Decoding Copper Cathode – Navigating Through the Indian Copper Market

Reading Time: 9 minutesOverview

Copper, a non-ferrous base metal, is highly valued for its exceptional conductivity, ductility, efficiency, corrosion resistance, machinability, and recyclability. Its extensive usage encompasses power generation, transmission, electricity distribution, and a myriad of end-use applications and consumer products.

Copper is used as a fundamental raw material across various industries, making it ‘Doctor Copper’, an important determinant of the economic health of any nation.

Beyond traditional sectors, copper is integral to energy transition technologies such as wind and solar power, storage batteries, and electric vehicles (EVs). The copper intensity for power generation from solar and wind sources is approximately twice that required for conventional power generation (International Energy Agency, 2022). Additionally, an EV necessitates two to three times more copper than an internal combustion engine vehicle.

The Criticality of Copper

Copper is essential for economic development and the green transition, leading major mining jurisdictions like the USA, Canada, Australia, and the EU to classify it as a critical and strategic mineral. The Ministry of Mines highlights copper’s high economic importance (Ministry of Mines, 2023). CSEP’s study on ‘Assessing the Criticality of Minerals for India’ assesses the criticality of 43 minerals based on their economic importance and supply risks (Chadha et al, 2023). The study points out that copper’s economic importance outweighs its supply risks. Its diversified supply sources, mature markets, and recyclability make it less risky on the supply side.

Economic Significance of Copper

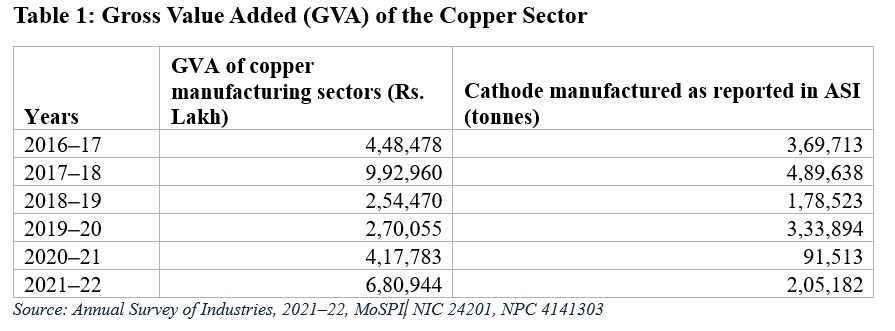

To emphasise the economic significance, the latest ASI data (2021–22) indicates that the GVA by this sector amounted to Rs 6,80,944 lakh, representing approximately 11% of the GVA for the entire basic and non-ferrous metals manufacturing sector (Table 1). Based on the sectoral cathode consumption, it is estimated that approximately 10% of the country’s manufacturing GVA would be affected in the absence of effective substitutes if the cathode supply gets stalled. Copper cathode is extensively used as a critical raw material in various industries (Figure 1). A bulk portion of cathodes is consumed by copper product manufacturers and steel fabricators. Consequently, due to the widespread and diverse applications of copper across various industries, any disruption in the copper supply chain would have a substantial impact on the basic metals and metallurgical sectors. Moreover, cathodes serve as intermediary products not only to produce finished copper goods but also for other manufacturing industries, highlighting their crucial role in the economy.

Source: Annual Survey of Industries, 2021-22, MoSPI

Source: Annual Survey of Industries, 2021-22, MoSPI

In this emerging era of energy transition and economic growth, the annual global demand for refined copper is expected to reach 50 million tonnes by 2050, up from 26.1 million tonnes in 2022 (International Copper Association, 2023).

The Refined Copper (Cathode) Conundrum

The highest value addition in terms of purity occurs at the smelting and refining stage when copper concentrates are smelted into blister (90.5% Cu) and then refined into copper cathodes (> 99.99% Cu) which become available to the fabricators and downstream industries for end-use product manufacturing. Copper cathode is typically traded either through contracts or on-spot trading on the Commodity Exchange (COMEX) and London Metal Exchange (LME) and the cathodes’ price determines the prices of other embedded finished products.

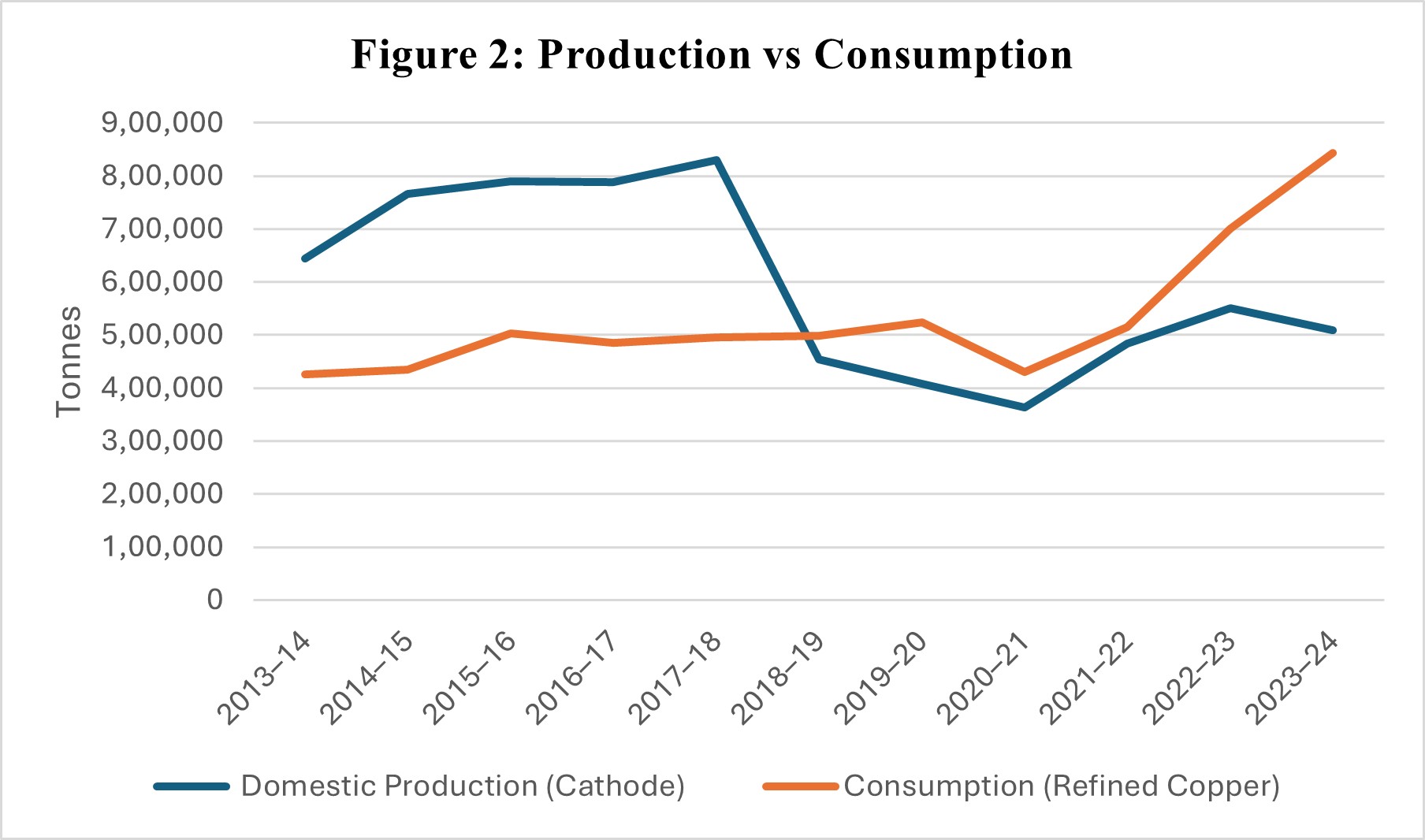

Refined Copper Status: Production vs Consumption

Source: Indian Minerals Yearbook, IBM

Source: Indian Minerals Yearbook, IBM

The domestic production of copper cathode in India showed significant growth until 2017–18, followed by a sharp decline. While production saw a slight increase since 2020–21, it has not returned to pre-2017–18 levels (Figure 2). Globally, the average annual growth rate of refined copper production was 2% from 2013 to 2022 (International Copper Study Group, 2023). The domestic production of cathode has seen an average annual growth rate of just 0.01% over the past decade. For FY 2023–24, production was approximately 5.09 lakh tonnes, reflecting an 8% decrease from the previous year. Domestic consumption is computed by excluding each year’s exports of refined copper from the total domestic production and adding imported refined copper. Yearly trends in domestic consumption also reflect the demand for refined copper. Although demand dipped slightly in 2020–21, perhaps on account of the COVID-19 pandemic, it has been rising since 2021–22.

Until 2017–18, India was self-sufficient in meeting its domestic copper demand and exported a substantial amount of refined copper overseas.

However, Sterlite’s copper plant, with a production capacity of four lakh tonnes per year, has been shut down since 2018 due to environmental non-compliance and pollution concerns, drastically reducing domestic production afterwards (Yadav, 2024). As a result, the additional supply of refined copper is being met through imports, leading to a gradual increase in import volumes. The trade scenario is discussed in the following section.

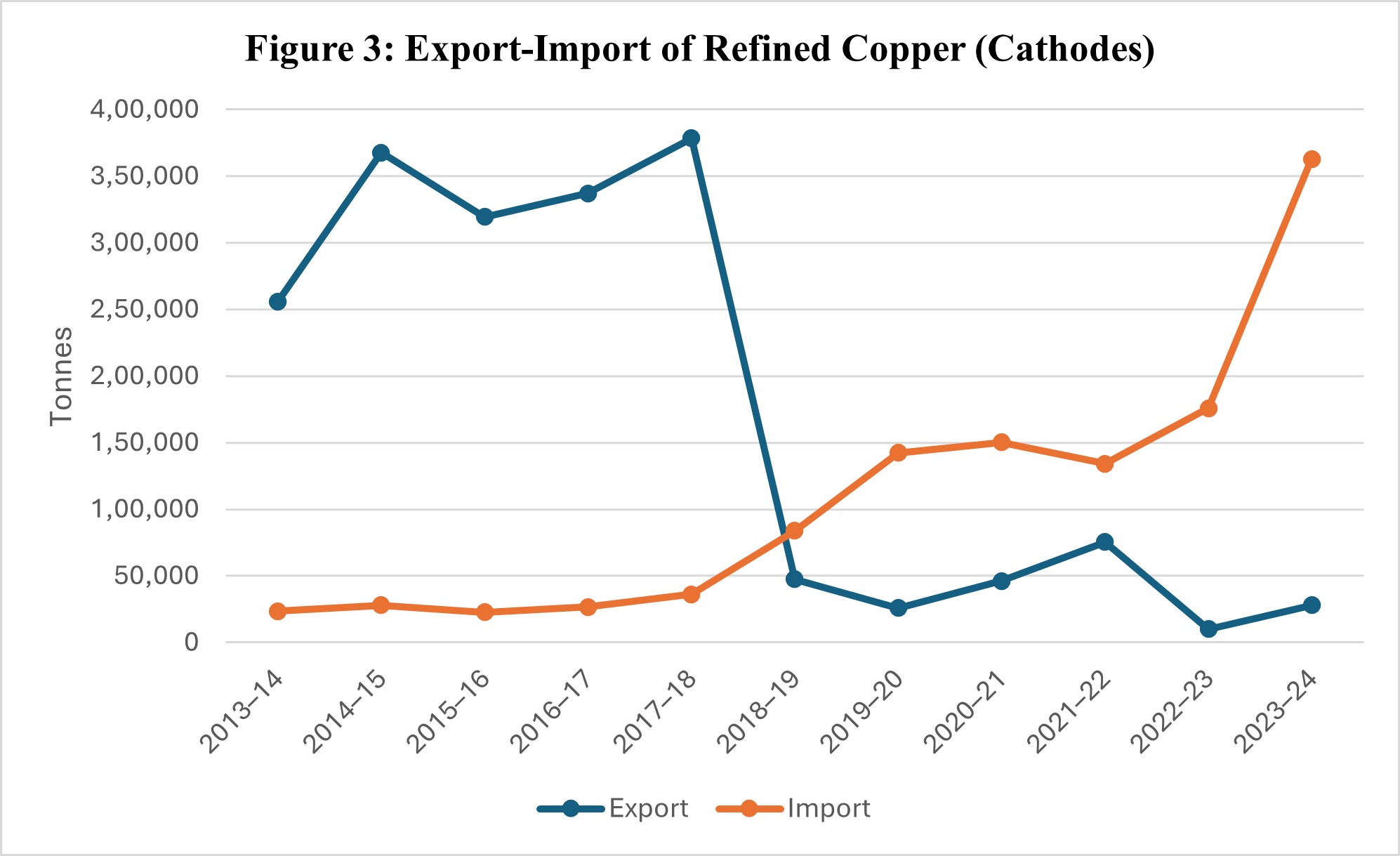

Trade Scenario

Source: Ministry of Commerce https://tradestat.commerce.gov.in/eidb/default.asp

Source: Ministry of Commerce https://tradestat.commerce.gov.in/eidb/default.asp

Since 2018–19, India has transitioned from being a net exporter to a net importer of copper. The inability of other domestic industries to pace up, combined with accelerating domestic demand, has exacerbated India’s reliance on copper imports, including refined copper (Figure 3).

Post-2018–19, the trade deficit has widened, with imports in FY 2023–24 increasing by 107% compared to the previous year.

Another factor contributing to rising imports, as reported by industries, is the reduction of duty rates to near-zero under Free Trade Agreements with Japan and ASEAN nations (Dhoot, 2015).

Closer Look at the Indian Copper Sector

Indian refined copper market faces a significant demand-supply gap. To address this critical challenge, we need to understand the loopholes and challenges faced by Indian copper processing and mid-stream processing industries, including smelters, refiners, and fabricators, as well as potential geopolitical challenges.

In the Indian copper scenario, three key players: Hindustan Copper Limited (HCL) from the public sector predominately engages in the mining and beneficiation of copper ore. In contrast, Sterlite Copper (a unit of Vedanta) and Hindalco from the private sector are mostly engaged in the processing, with a total installed smelting and refining capacity of nearly 10.28 lakh tonnes (Ministry of Mines, 2024).

The HCL produces copper ore and concentrates at their five operating copper mines. Moreover, HCL has two primary smelting and refining plants and a secondary copper smelter with a combined installed capacity of 0.68 lakh tonnes. However, since 2020, HCL has phased out its cathode production due to economic non-viability and entered a public-private partnership with Hindalco. Under this partnership, HCL will sell 60% of its concentrates to Hindalco for refined copper production, whereas the rest will be sold through open tender at LME-linked prices (Hindalco Industries Limited, 2020).

With HCL ceasing its copper cathode production, Hindalco and Vedanta remain the only dominant players in the refined copper market.

Hindalco operates a port-based custom copper smelter at Dahej, Gujarat, housing three smelters and three refineries with a combined installed capacity of 500 thousand tonnes, making it the second-largest smelter and sixth-largest refiner in the world. In FY 2022–23, it produced 407 thousand tonnes of cathode, exhibiting a growth rate of 13% over the preceding year (Hindalco Industries Limited, 2023). Hindalco meets more than 50% of domestic refined copper requirements, catering to diverse sectors such as railways, electrical equipment, consumer durables, automotive and transport.

Vedanta Ltd.’s Sterlite Copper used to contribute more than 36% of India’s demand for refined copper with an installed capacity of 460 thousand tonnes in their two operating units at Thoothukudi, Tamil Nadu and Silvassa, Daman and Diu (Ministry of Mines, 2024). However, in 2022–23, Vedanta recorded 148 thousand tonnes of cathode production from its only operational Silvassa plant, which has an installed capacity of 216 thousand tonnes per annum (Vedanta Limited, 2022–23). A study estimated the consolidated loss due to the closure of the Thoothukudi plant is approximately Rs 14,749 Cr which is about 0.72% of the state GDP of Tamil Nadu (Batra, 2022). Both companies rely on importing copper concentrates from their mines abroad or other overseas reserves (Ministry of Mines, 2024).

As an emerging player, Adani Enterprises’ subsidiary, Kutch Copper, has recently launched the first unit of its greenfield copper refinery at Mundra, Gujarat. With an initial investment of USD 1.2 billion, the first phase will establish a smelter with a capacity of 500 thousand tonnes, eventually expanding to one million tonnes per annum in the second phase, making it one of the largest port-based single-location custom smelters in the world (Adani Enterprises Limited, 2024).

Global Concerns of Processing

Copper processing is apparently more concentrated than copper mining, where China dominates approximately 44% of global refined copper production. In contrast, the top three countries in copper mine production are Chile (23%), Peru (12%) and the Democratic Republic of Congo (DRC) (11%) (Mineral Commodity Summary, 2024). Despite, being the largest extractor of copper, Chile produced only 8% of the world’s refined copper in 2023, down from 12% in 2015. A substantial portion of Chile’s copper concentrate is exported for refining, primarily to China (IEA, 2024).

In a usual copper business model, commissioning new projects involves long-term agreements between miners, semi-fabricators and refiners, as smelters require a guaranteed supply of copper concentrates as feedstock. However, there is a tightened supply of concentrates due to resource exhaustion in existing mines, diminishing grades, geotechnical and operational issues, limited discoveries, and delays in commissioning new mining operations. This constrained supply, combined with the expansion of smelting and refining capacity, will affect treatment and refining charges (TC/RCs)[1], leading to an increase in capital and operating costs. Most miners and smelters negotiate long-term contracts based on an annually agreed benchmark framework, where the first settlement between a major miner and a smelter typically sets the benchmark TC for the year ahead (Charlesworth, 2024). In November 2023, Chilean miner Antofagasta and Chinese smelter Jinchuan established the benchmark at USD 80 per tonne. The same rate was adopted by Freeport-McMoRan and Jiangxi Copper. This TC is 9% lower than the previous year’s USD 88 per tonne, marking the first drop in TCs in three years (Mining.Com, 2023).

[1] TC/RCs are the fees which the mining companies pay to the smelters to convert their semi-processed ore or concentrate into cathodes or finished metal.

This global plummeting of TCs/RCs adversely impacts Indian processors’ revenue as well as the entire copper supply chain, market, and investment. To offset this, domestic smelters must prioritise increasing value-added output over enhancing tonnage.

While Kutch Copper’s entry might boost production and ease the trade deficit, currently, only 50% of India’s mid-stream processing capacity gets utilised. Huge working capital requirements, complex raw material procurement, scarce availability of domestic ore and concentrates, and bulk imports of cathodes and other finished products have adversely impacted India’s primary and downstream copper industry.

The Way Forward

Copper industries face several challenges in terms of global supply-chain vulnerabilities, import reliance, limited geopolitical presence, shutting down of major production units, scarce domestic ores, and insufficient exploration to convert resources into reserves and reserves into production.

Addressing these challenges requires strategic investments, adherence to environmental standards, and leveraging public-private partnerships to enhance production capacities. Building domestic processing capabilities, focusing on research and development, and technological innovation are essential to secure the copper supply chain. Given the capital intensity of the industry, incorporating copper mid-stream processors into India’s production-linked incentive scheme would incentivise domestic processors to attract further investments (Raizada & Moerenhout, 2024). However, providing such incentives is a short-term solution to an overall push to make the industry internationally competitive.

The strategic acquisition of mines abroad in copper-rich countries such as Chile, Peru, DRC, Australia, and South Africa, along with bilateral cooperation in copper processing ventures and knowledge-sharing through diplomatic and trade agreements, should be augmented. Alongside Khanij Bidesh India Limited’s (KABIL’s) government-to-government (G-to-G) negotiations, efforts should also be directed towards business-to-business (B-to-B) collaborations.

The exemption of customs duties on 25 critical minerals, as declared in the Union Budget 2024-25, will boost the domestic processing and refining sector, thereby enhancing competitiveness in the manufacturing sector (Press Information Bureau, 2024).

References

Adani Enterprises Limited. (2024). Adani’s copper unit in Mundra begins operations. Retrieved from https://www.adanienterprises.com/en/newsroom/media-releases/adanis-copper-unit-in-mundra-begins-operations

Chadha, R. Sivamani, G. and Bansal, K. (2023). Assessing the Criticality of Minerals for India: 2023 (CSEP Working Paper 49). New Delhi: Centre for Social and Economic Progress. Retrieved from https://csep.org/wp-content/uploads/2023/04/Critical-Minerals-for-India-2.pdf

Charlesworth, L. (2024, June). Copper concentrate benchmark structure at risk in current market – Fastmarkets. Fastmarkets. Retrieved from https://www.fastmarkets.com/insights/copper-concentrate-benchmark-structure-at-risk/

Dhoot, V. (2015, October). As cheaper imports increases copper industry sends SOS to government. The Economic Times. Retrieved from https://economictimes.indiatimes.com/industry/indl-goods/svs/metals-mining/as-cheaper-imports-increases-copper-industry-sends-sos-to-government/articleshow/49344924.cms?from=mdr

Hindalco Industries Limited. (2020, September). Hindalco and Hindustan Copper sign MoU for supply of copper concentrate. Retrieved from https://www.hindalco.com/media/press-releases/hindalco-and-hindustan-copper-sign-mou-for-supply-of-copper-concentrate

Hindalco Industries Limited. (2023). Integrated annual report 2022–23. Retrieved from https://www.hindalco.com/upload/pdf/hindalco-annual-report-2022-23.pdf

IEA. (2024). Global Critical Minerals Outlook 2024, IEA, Paris. Retrieved from https://iea.blob.core.windows.net/assets/ee01701d-1d5c-4ba8-9df6-abeeac9de99a/GlobalCriticalMineralsOutlook2024.pdf

International Copper Association. (2023). COPPER—THE PATHWAY TO NET ZERO. In Copper—The Pathway to Net Zero: Summary. Retrieved from https://internationalcopper.org/wp-content/uploads/2023/03/ICA-GlobalDecarb-Summary-A4-202302-R3.pdf

International Copper Study Group. (2023). The World Copper Factbook 2023. Retrieved from https://icsg.org/copper-factbook/

International Energy Agency. (2022). The role of critical minerals in clean energy transitions. https://iea.blob.core.windows.net/assets/ffd2a83b-8c30-4e9d-980a-52b6d9a86fdc/TheRoleofCriticalMineralsinCleanEnergyTransitions.pdf

Mineral Commodity Summary. (2024). U.S. Geological Survey, 64–65. Retrieved from https://pubs.usgs.gov/periodicals/mcs2024/mcs2024.pdf

Mining.Com. (2023, December). Copper miners, Chinese smelters agree on first drop in fees in 3 years – MINING.COM. Retrieved from https://www.mining.com/web/copper-miners-chinese-smelters-agree-first-drop-in-fees-in-3-years/

Ministry of Mines, Indian Bureau of Mines. (2024, April). Indian Minerals Yearbook 2022 (Part II: Metals and Alloys). Retrieved from https://ibm.gov.in/writereaddata/files/1715685346664347e2b0816Copper_2022.pdf

Ministry of Mines. (2023). Critical Minerals for India. Retrieved from https://mines.gov.in/admin/storage/app/uploads/649d4212cceb01688027666.pdf

Press Information Bureau. (2024, July). Reforms In Customs Duties Will Support Domestic Manufacturing and Promote Export Competitiveness. Ministry of Finance. Retrieved from https://pib.gov.in/PressReleasePage.aspx?PRID=2035601

Raizada, S., & Moerenhout, T. (2024). Securing India’s Copper Supply Challenges and the way forward. International Institute for Sustainable Development. Retrieved from https://www.iisd.org/system/files/2024-07/securing-india-copper-supply.pdf

Vedanta Limited. (2022-23). Integrated Report and Annual Accounts 2022-23. Retrieved from https://www.vedantalimited.com/uploads/investor-overview/annual-report/Vedanta-Limited-Integrated-Annual-Report-202022-23-VF.pdf

Yadav, K. (2024). SC junks Vedanta’s plea to reopen Sterlite Copper’s Thoothukudi plant. Mint. Retrieved from https://www.livemint.com/companies/news/setback-for-vedanta-as-sc-dismisses-plea-to-reopen-sterlite-copper-plant-in-tamil-nadus-thoothukudi-11709205833536.html

FOOTNOTES

[1] TC/RCs are the fees which the mining companies pay to the smelters to convert their semi-processed ore or concentrate into cathodes or finished metal.

Rajesh Chadha

Tanima Pal

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.