Odisha Privatisation Round 2: Lessons, Challenges, and Opportunities

Reading Time: 10 minutes

Executive Summary

The state of Odisha has a predominantly rural and tribal population, with over three-quarters of its residents living in rural areas. Managing electricity distribution in Odisha has been challenging, characterised by high transmission and distribution (T&D) losses, underinvestment, and system inefficiencies. Odisha first ventured into privatising its power sector in the late 1990s. The effort failed to meet its objectives for several reasons, including poor scheme design, lack of investment by the private players, insufficient political support and regulatory oversight, and the failure to reduce technical and commercial losses. As a result of this failure, rural and household electrification also suffered. The first round of privatising electricity distribution ended with the Odisha Electricity Regulatory Commission (OERC) revoking the licences of all the privately owned distribution companies (discoms) and entrusting their operation and management to the administrators appointed by it.

In 2017, the OERC embarked on a second phase of privatisation by auctioning the utilities managed by the administrators. It aimed to bring private sector investment and expertise to improve the discoms’ performance. Tata Power Company (TPC) was eventually selected as the new private partner to operate all four discoms in the state—Northern, Western, Central, and Southern Odisha Distribution Limited (now Tata Power Northern Odisha Distribution Limited [TPNODL], Tata Power Western Odisha Distribution Limited [TPWODL], Tata Power Central Odisha Distribution Limited [TPCODL], and Tata Power Southern Odisha Distribution Limited [TPSODL]). GRIDCO, a state-owned company, continued to be responsible for all the power procurement and planning for the state. It is also a part-owner of the new discoms and holds 49% equity, while Tata Power holds 51%.

This paper reviews the second round of Odisha distribution privatisation in detail to draw broader lessons and insights to help the process of structural reforms at the state level. It is part of a project that evaluates various ownership options for the discoms, including public ownership, private ownership, and distribution franchisees.

Odisha’s Second Round of Privatisation

In 2016–2017, the OERC initiated the privatisation process by first inviting bids for the erstwhile Central Electricity Supply Utility (CESU). There was little interest. Eventually, bids for all four discoms were invited, but interest remained low. Noting the lack of enthusiasm from the private sector, the Commission conducted several meetings with potential buyers to understand how the bid design could be improved. Post these consultations, the revised bids offered several attractive incentives to make the proposal more appealing to the potential bidders. The entry barriers were lowered, allowing generating companies or consortia with 1 GW+ generating stations to qualify, and reducing the net worth requirement from Rs 1,200 crore to Rs 600 crore. Some of the more salient features of the revised bids are as follows:

- Setting a Low Reserve Price: In contrast to the first round of privatisation—in which the asset value was inflated supposedly to realise better returns—in the second round, the OERC deliberately set the asset prices at 15%–30% of the book value. This achieved two things: first, it made it easy for the bidders to participate, as the upfront investment required was substantially low; second, it protected consumers from a potential tariff shock on account of upward asset revaluation. The reserve price was also used as the base for computing return on equity for the new discoms. As the new discoms would undertake capital expenditure (capex), the equity base would increase proportionately. This also helped in keeping tariffs low while incentivising fresh investments.

- Continuing With the Single-Buyer Model: In round two, the state continued with GRIDCO as the single entity responsible for all power purchase planning and procurement. Being a coal-rich state, GRIDCO has the advantage of having access to low-cost power purchase agreements (PPAs) with various independent power producers (IPPs) under the state’s energy and industrial policy. Low-cost hydropower is also a part of the state energy mix. The low power purchase cost helps in keeping consumer tariffs low. The OERC approves GRIDCO’s power purchase expenses and determines the quantum and cost of power allocated to each discom. While the consumer tariff is uniform across the state, the Bulk Supply Price (BSP)—the price at which the discoms buy power from GRIDCO—differs for each discom. It is the lowest for Southern Electricity Supply Company (SOUTHCO) or TPSODL, which has a very high share of low-tension (LT) consumers, and is the highest for Western Electricity Supply Company of Odisha (WESCO) or TPWODL, which has a very high share of high-tension (HT) and extra-high-tension (EHT) consumers in its mix.

- Equity-in-Kind Arrangement: Since 2013, the Government of Odisha (GoO) has invested over Rs 10,000 crore in improving the distribution infrastructure. These assets are on the books of the state government and are transferred to the new discoms as and when GRIDCO needs to make any equity contribution for new capital investments made by them. This arrangement, called equity-in-kind, has three key benefits: a) it allows the new discoms to use the entire asset base from day one without buying these assets; b) it helps the financially constrained GRIDCO fulfil its obligation to contribute equity in the new investments without any additional support from the state government; and c) it moderates the tariff impact for retail consumers by gradually increasing the book value of assets.

- Discoms as Franchisees: The second round of privatisation has primarily followed an input-based distribution franchisee-like model, where the new discoms act more as distribution network operators than fully independent distribution licensees. This is due to the continuing role of GRIDCO as the state’s bulk power supplier, which relieves the new discoms of power procurement responsibilities. Like the franchisees, the OERC uses a fixed trajectory for Aggregate Technical and Commercial (AT&C) losses for tariff determination. The discoms keep any losses or gains arising from the actual AT&C loss levels.

- Floor for Capital Expenditure: Learning from the mistakes of the first round, in which the private sector made few investments, in the second round, the bidders were required to provide a capital expenditure trajectory for the first five years and invest at least Rs 500 crore during this period. This was crucial to ensure that the new discoms made investments not just for loss reduction but also for network upgradation and augmentation.

- Incentive on Arrear Collection: The bids offered an incentive of 10% for past arrears collected from live consumers and 20% for those collected from the permanently disconnected ones. In the case of SOUTHCO, the incentive is higher at 20% on past arrears collected from live consumers and 30% on those collected from permanently disconnected consumers due to higher arrears. The bidders were required to quote an arrear recovery trajectory for the first five years. Failure to recover arrears as per the commitment given in the bid for any given year could lead to encashment of the Performance Guarantee, to the extent of 10% of such shortfall.

- Transfer of Employees and Employee Benefits: All existing utility employees, except those on deputation, were transferred to the newly formed discoms. These employees continue to be governed by the terms of their original appointment. The new discoms cannot change them or make their existing service conditions worse in any manner. The bidders were required to submit a staff deployment plan after considering the existing employees of the erstwhile utilities. Each utility had an Employee Pension Trust, an Employee Gratuity Trust, an Employee Provident Fund Trust, and a Rehabilitation Trust. After bidding and selecting new discoms, these arrangements were to continue as before. The new discoms are responsible for remitting designated amounts to these Trusts at scheduled intervals, and they cannot liquidate these investments without OERC’s prior approval.

Operational Performance of the New Discoms

Given below are some of the highlights of the new discoms’ operational and financial performance:

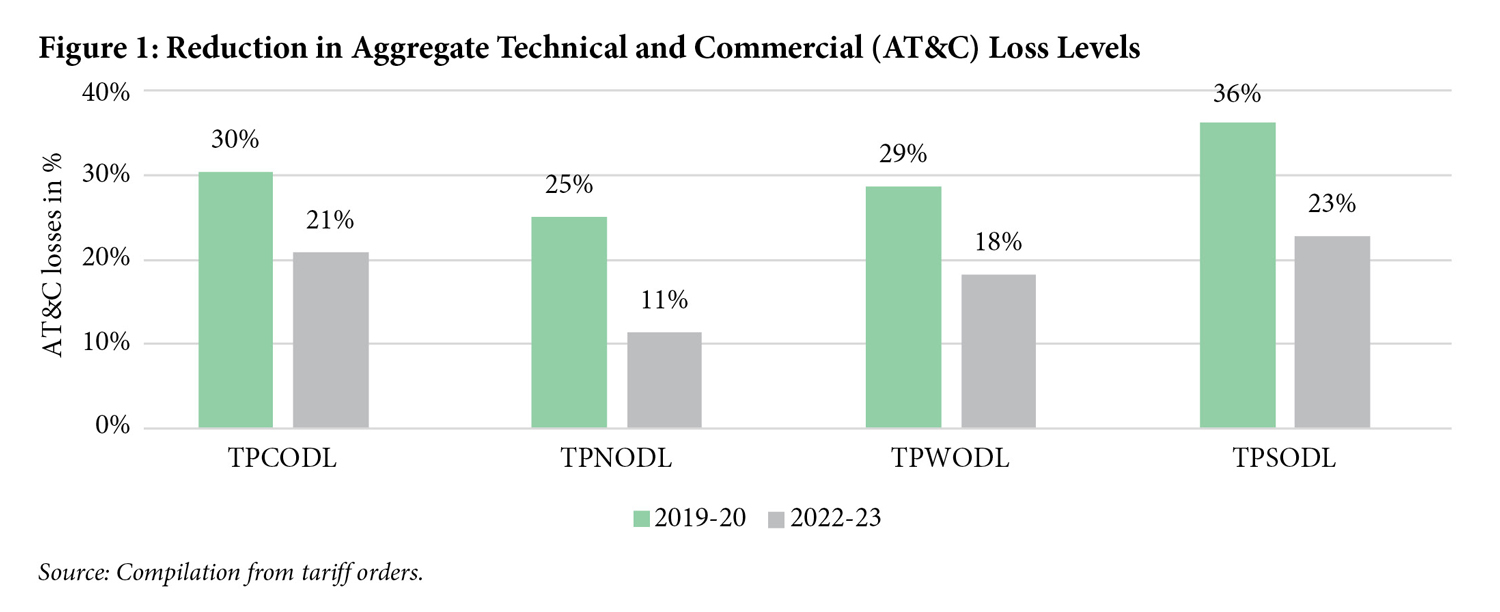

- As can be seen from Figure 1, the AT&C losses for all four discoms have reduced significantly over three years. Furthermore, in FY 2023, all discoms achieved lower AT&C loss levels than the trajectory set by the OERC for tariff determination for that year.

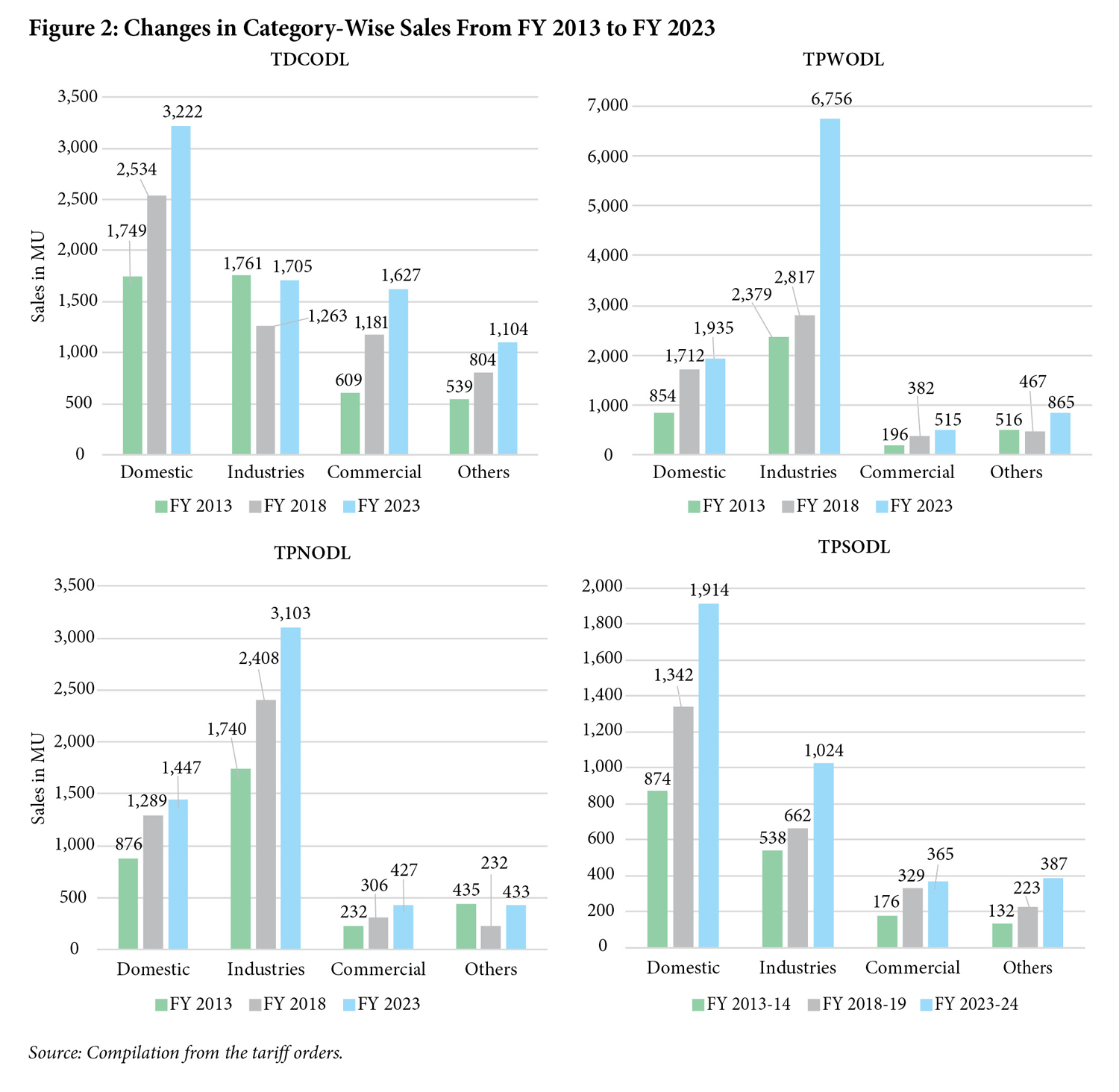

- Total sales across all four discoms have also increased substantially (refer to Figure 2). In addition, except for TPCODL, the new discoms have increased sales to industrial and commercial consumers, including those who had earlier migrated to open access and/or captive consumption.

- In its bids, TPC committed to undertaking total capital expenditure of Rs 5,640 crore in the first five years across all four discoms. As per the FY 2024-25, the capex approved until FY 2023 seems largely on track to meet this commitment. However, the level of capitalisation is different for each discom, ranging from 60% to 80%, and overall spending is around 70% of the planned amount.

- Most significant, as per the annual reports (FY 2023), all discoms have reported profits after tax.

These performance indicators are certainly encouraging. However, it needs to be noted that a good part of this success can be attributed to the favourable terms of the deal, which included a clean slate free from past liabilities (mandatory as per Section 21 of the Electricity Act, 2003), substantial state support, below-cost bulk supply tariffs, lucrative incentives for loss reduction and arrear recovery, and so on. Further, the new discoms seem to be shielded from current and ongoing losses due to tariffs not reflecting costs, as the government has explicitly suggested to the OERC to park such losses in GRIDCO’s accounts. The success of TPC’s involvement suggests that government support and favourable regulatory and financial conditions are critical for attracting private investment in electricity distribution, particularly in regions with rural and low-income consumers.

Observations and Lessons from Odisha’s Second Round of Privatisation

Based on a detailed review of the second round of privatisation in Odisha, we draw the following lessons, observations, and insights.

- Need to Balance the Interests of Private Entities and Consumers: One of the critical lessons from the second round of privatisation is the limited interest from private entities in operating discoms with a large number of rural and low-income consumers. The reluctance stems from the perception of high financial risk and the challenge of achieving full-cost recovery in such areas. Odisha addressed this by shielding the new discoms from revenue losses due to the non-revision of tariffs, at least so far in the initial period, and providing subsidised bulk supply rates. It also offered substantial incentives for loss reduction and arrear recovery while giving significant discounts on asset prices. All this was instrumental in attracting a big and serious player like Tata Power to bid for and take over the discoms, but there was hardly any competition.

- Cross- and Direct-Subsidisation Done Through GRIDCO: Odisha’s state-owned bulk power supplier, GRIDCO, is central to managing the second round of privatisation. Its access to relatively low-cost power is vital to keeping the new discoms financially viable without significantly increasing retail tariffs. This enabled the discoms to operate without immediate financial distress. Although there is not much cross-subsidy built into the retail tariff structure, it is provided by adjusting the BSP that the discoms pay to GRIDCO. The BSP is lowest for TPSODL, which has a predominantly LT small and residential consumer base, while it is the highest for TPWODL, which has a majorly HT industrial and commercial consumer base. BSP is set prospectively for the year, and there are no mechanisms to compensate GRIDCO for short-term borrowings arising on account of changes in power purchase cost or quantum, or deviations from scheduled generation or demand.

- Continued Need for State Support: Like most states, achieving full-cost recovery through tariff increases is a politically sensitive issue in Odisha, particularly given the state’s rural and low-income demographics. Going forward, OERC’s reluctance to adopt measures such as a fuel adjustment surcharge, intra-state Deviation and Settlement Mechanism (DSM) or setting cost-reflective retail supply tariffs can make it challenging for GRIDCO to fully cover operational costs. Without such corrective measures, losses could continue, as would the need for state support. Even if all the desirable regulatory measures are implemented to enable GRIDCO and discoms to recover costs through tariffs, small and vulnerable consumers will need protection and support from the state to withstand such cost increases. This suggests that while privatisation can drive efficiency improvements, it may not be sufficient to resolve the financial challenges that the sector faces. Addressing these challenges will necessitate not just tariff and regulatory reform, but also sustained and consistent political and financial support from the state government.

Conclusions

The second round of electricity distribution privatisation in Odisha offers valuable lessons for the broader power sector. Tata Power’s success suggests that favourable regulatory and financial conditions are critical for attracting private investment, particularly in regions with rural and low-income consumers. The experiment so far has led to notable improvements in operational efficiency, loss reduction, and the overall financial situation of the discoms. However, full-cost recovery over a sustained period remains challenging due to constraints on tariff reforms and the difficulties inherent in serving a predominantly rural consumer base. The issue of ensuring full-cost recovery over the long term with gradual reduction and ultimately elimination of financial support from the state government is important. However, given the complexity of the issue, it would be best covered in a separate paper. Nevertheless, the experience in Odisha 2.0 described in this paper highlights the possibility of turning around a loss-making distribution business through carefully designed reforms supported by the state with adequate subsidies and financial support.

As the whole power sector in Odisha moves towards full-cost recovery, power procurement practices will need improvement. This will be best accomplished if effective resource planning is implemented to manage the resource portfolio.

The sustainability of Odisha’s newly (re)privatised discoms will depend on continued regulatory and state support and their ability to adapt to future challenges, particularly the integration of renewable energy. To ensure long-term success, regulatory innovations and a collaborative approach between the private sector and the government will be necessary to maintain financial stability while meeting consumers’ evolving needs. The Odisha experiment serves as an important case study for other states such as Uttar Pradesh that are considering structural reform to improve efficiency in power distribution, demonstrating both the potential benefits, costs, and the ongoing challenges in managing the complexities that arise in the wake of such changes.

Q&A with authors

What is the core message of your paper?

Odisha’s “Privatisation Round 2” experiment shows that loss-making discoms can be turned around, and structural reforms are feasible even in challenging regions characterised by rural and low-income consumers, provided they are supported by carefully designed regulatory innovations and sustained through political and financial backing from the state. However, ensuring full-cost recovery through consumer tariffs is still some distance away. Achieving this will require not just a sensitive and careful approach to tariff reforms but also a long-term and gradual plan for the reduction in the financial support given by the state government.

What presents the biggest opportunity?

The paper serves as an important case study for other states, such as Uttar Pradesh, that are considering structural reform to improve efficiency in power distribution, demonstrating both the potential benefits, costs, and the ongoing challenges in managing the complexities that arise in the wake of such changes.

The recently introduced Electricity Act Amendment Bill, 2025, is another huge opportunity to introduce structural reforms in the sector. The Act amendment process can benefit immensely from this paper to understand the core issues that affect the design and implementation of such reforms at the state level.

What presents the biggest challenge?

Making the electricity distribution business self-sustaining and profitable has been the holy grail of the Indian power sector. Carefully designed structural reforms can help, but they should not be seen as a silver bullet that, by itself, will solve this challenging problem with socio-political and historical roots. To ensure the long-term success of such reforms, continuous regulatory innovations and a well-calibrated long-term support plan from the government are essential.

Ashwini Chitnis

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.