Challenges for natural gas to become India’s bridge fuel: Economics, availability, and alternatives

Reading Time: 28 minutesDOWNLOADS

Abstract

This paper examines the possibilities for natural gas in India’s energy mix, both through the lens of competitive economic viability as well as the impact its use might have, notably, on carbon emissions. We examine the electricity sector in detail because it not only represents a high share of gas usage but also dominates India’s energy portfolio. Coal, which has the highest environmental impact, accounts for most of India’s carbon emissions. Almost three-quarters of coal goes towards producing electricity. While many countries have made the shift from coal power to natural gas, they relied on inexpensive natural gas supply, which India doesn’t have. From the cleanliness perspective, renewable energy (RE) appears to limit the value-proposition of natural gas. Opportunistic or variable RE, which does not require storage, has already become the lowest cost option for new electricity capacity. It may be a matter of only a few years before storage technologies mature and allow RE to displace both gas and coal, even as ‘firm power’. In addition to energy cost competitiveness, we examine the role of gas for other benefits such as flexibility and find a disproportionate value proposition. However, such uses add up to only a modest total volume. Natural gas does have a role in niches or select segments, including industry, which can drive some growth in India. However, it appears unlikely that the use of natural gas will grow either to the planned 15 percent of portfolio mix announced by the government or to a level where it accounts for a meaningful downward shift in India’s carbon emissions. On the bright side, carbon emissions are already decreasing because of RE, in addition to other shifts in the economy and increased efficiency.

A few years ago, the Indian government announced its ambition to almost triple the share of natural gas in its energy mix to 15 percent by 2030 (Press Trust of India, 2016).[1] There could be multiple possible objectives for this target, but it also has some contradictions. If resilience is the intent, then is sufficient domestic natural gas available? India currently imports half of its gas. If sustainability is the objective, from carbon and other perspectives, is natural gas the best fuel to achieve it? Can the value propositions of cleanliness or flexibility be achieved more cost-effectively elsewhere, such as from RE in the short run and, potentially, from hydrogen in the long run?[2] Both these points reflect the reality that natural gas remains a fossil fuel, even though it is much cleaner than coal.

Because natural gas has lower carbon (with more hydrogen) than coal and also because of the higher efficiencies in combined cycle gas power plants, gas-based power produces half the carbon emissions of coal-based power. This gets to the heart of the question analysed in this paper: is natural gas a bridge fuel for India as it moves away from coal to a low-carbon and, eventually, a zero-carbon economy? Does natural gas add, other than environmental benefits, values such as operational flexibility for the electricity grid, which would be more compatible with a high-RE future?

This paper focuses on the prospects for natural gas, especially its competitiveness based on more than just simplified economics. We begin by examining the sectors that can consume gas and illustrate how the power sector is a key area for consideration. We then compare natural gas with alternatives, both on economic grounds as well as non-economic factors such as its cleanliness and flexibility. We also examine scenarios for the growth of gas and estimate the impact of such increased use on our carbon emissions trajectory.

India’s experience and ambitions

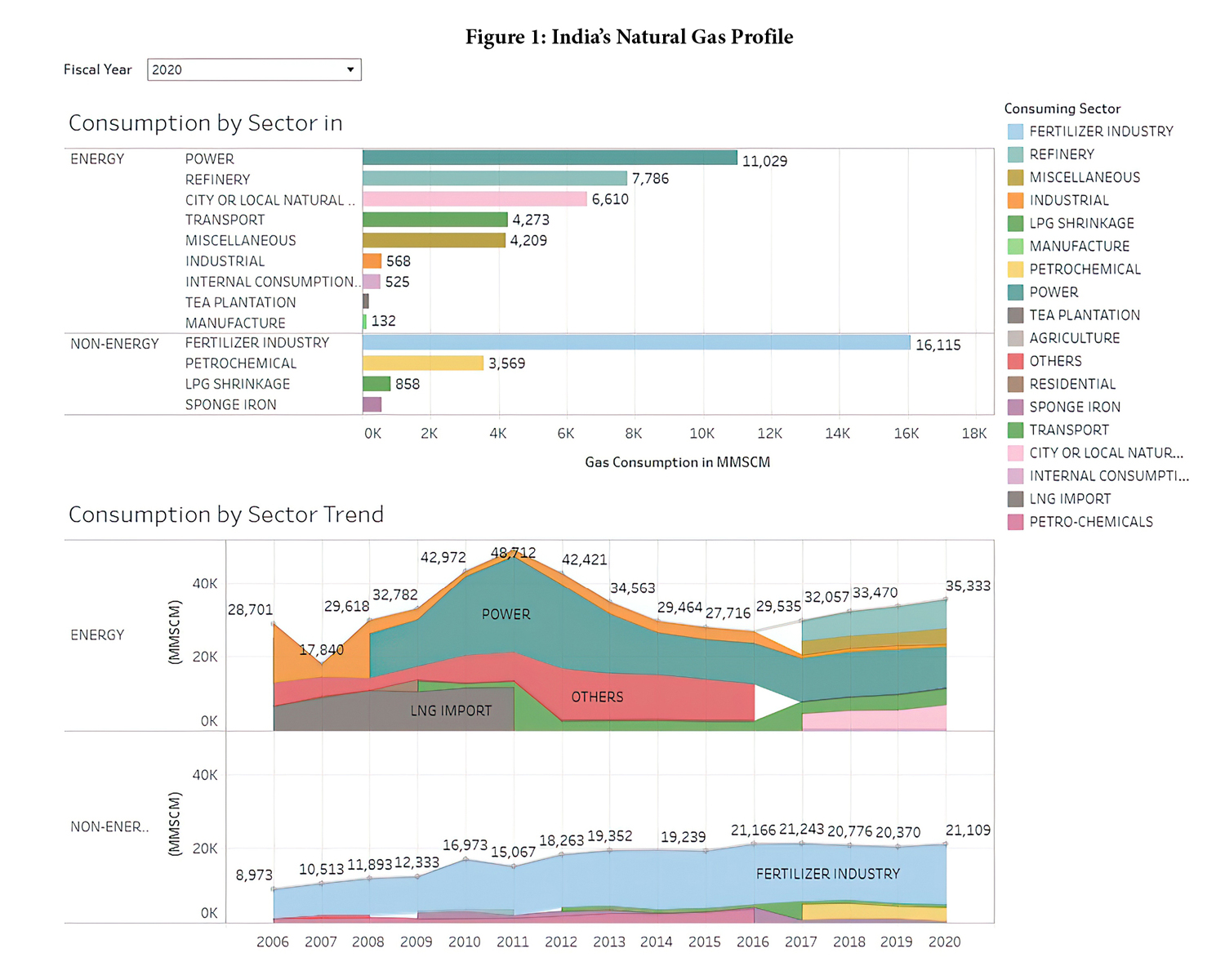

Figure 1 shows a current snapshot as well as a time series of natural gas usage in India. We see that the fertiliser industry dominates the use of natural gas (as input or feedstock). However, its growth has slowed down. The power sector is the second-largest consumer of natural gas. It has also declined from its peak a decade ago, and recent usage is relatively flat, at about a fifth of the total.

Source: NITI Aayog (n.d.)[3]

Note: There have been a few re-categorisations. ‘Other’ gives way to City Gas Distribution networks (which feed into household cooking and CNG stations, among other uses) and the segregation of petrochemical. LNG imports didn’t cease after FY2011, but official reporting changed to not factor this into the consumption side (breaking it down, for example, into other sectors).

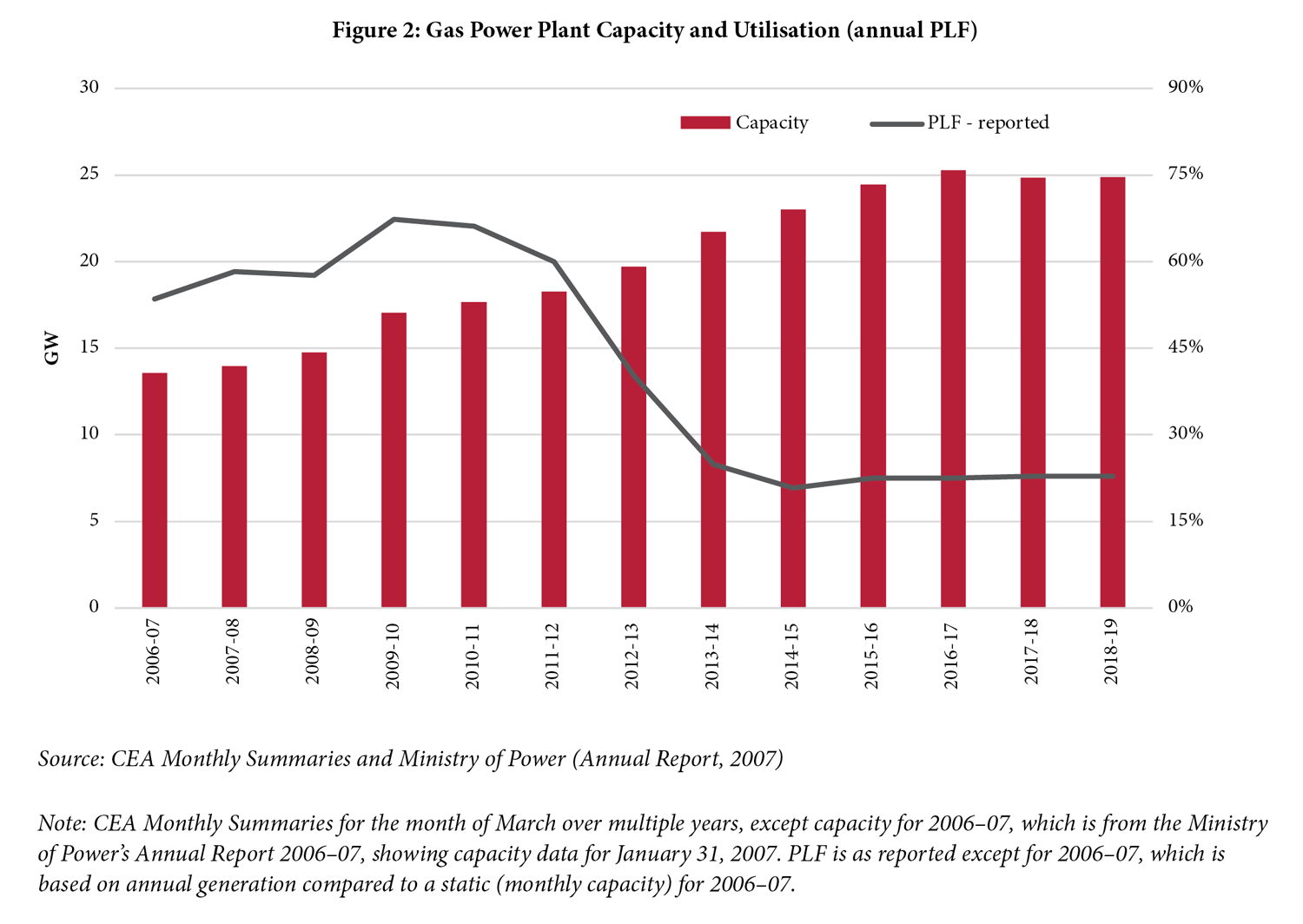

In the power sector, natural gas usage grew not because of a rise in power capacity but because viable (controlled price) gas was available to power plants. Power plant capacity grew faster than utilisation, leading to a dramatic fall in capacity utilisation (plant load factor, PLF), as Figure 2 shows. Gas-based power generation peaked in FY2010-11 in absolute terms. Its share in electricity has been falling since FY2009-10, stabilising around or below 4 percent of the total since 2013-14.

On the supply side, about half of India’s natural gas is imported as Liquefied Natural Gas (LNG), overwhelmingly from Qatar. Imports provide a near-limitless supply, albeit at a price higher than that set through the Administered Pricing Mechanism (APM) for selected domestic gas. APM gas has historically been prioritised for the fertiliser sector. Within the power sector, only a handful of gas-based power plants get cheap gas.[4] Most remaining power users have to rely on more expensive imported LNG, which ends up expensive as delivered, despite often low global spot prices. This is one reason the utilisation (Plant Load Factor) of many gas power plants was very low in 2019. It was even zero for over a dozen plants. These plants are not able to compete on the merit order despatch, where grid operators select (despatch) the incremental supply based on marginal price signals, which, for fossil fuel plants, are largely the fuel costs.

While prices are a factor, the growth of natural gas would likely be far more constrained by demand than by supply.

Lessons from other countries on role of gas

The world is awash in natural gas. Because of technology improvements, including extraction of tight gas (shale gas), the reserves-to-production ratio has grown to just under 50 years as of 2019 (BP, 2020). Unofficial estimates suggest extractable gas reserves are multiple times higher.

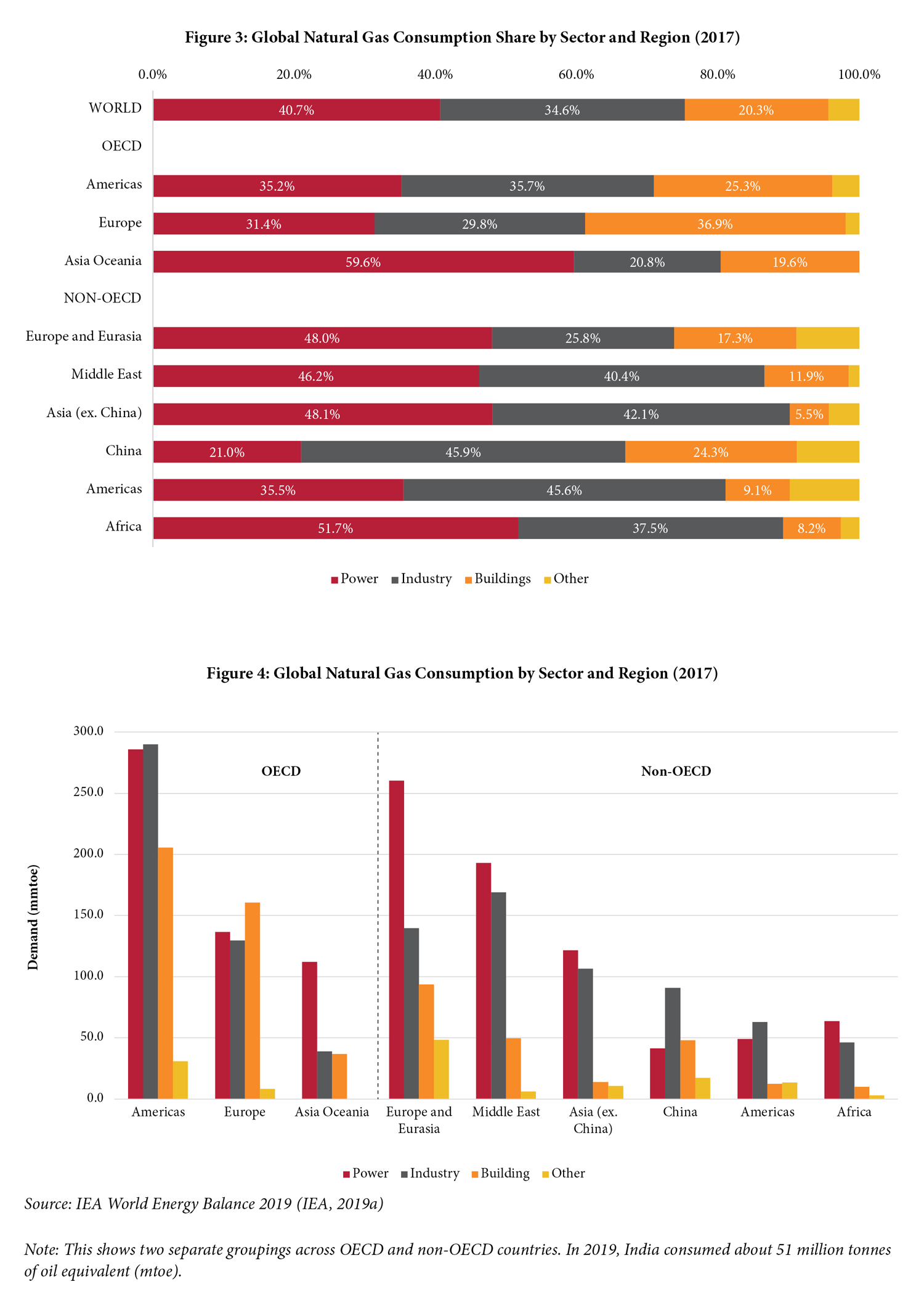

Globally, power-generation, industry, and heating (used in buildings) are the three major sectors that consume natural gas (Figure 3). But the mix varies heavily by country (shown in an absolute scale in Figure 4). In power, natural gas use has thrived either when cheap domestic gas is available or when there is no easy alternative such as coal or hydro. The US and UK did have coal reserves but natural gas displaced coal because of a price advantage. The rise in their use of RE has been relatively recent.

The physical nature of natural gas poses a challenge, making its transportation more expensive than that of oil. Internationally, the original gas flows used pipelines but LNG has gained ground. LNG involves up-front capital investment towards facilities for liquefaction, tankers, and regasification. This makes LNG cheaper than pipelines over long distances. Historically, many LNG facilities were designed as an alternatives to pipelines. They had a specific buyer as the anchor, if not the sole beneficiary. Despite rising flexibility for LNG sales, in 2018, spot sales for LNG were about 100 Billion Cubic Meters (BCM), (IEA, 2019b) a tiny fraction of the global gas consumption of 3,852 BCM (BP, 2020). However, when we consider only international transactions, spot sales have grown to a third of LNG sales in 2019. LNG accounts for a third of total sales of international gas; the remainder is delivered via pipelines.

Global shifts in natural gas use are a complex intersection of market changes, new technologies and new entrants, among other factors. Energy security has not been as big a consideration as one would imagine in much of the world. For instance, even during the Cold War, Western Europe expanded its use of Russian natural gas. While India has grave concerns over any pipeline coming through Pakistan, it has not operationalised pipeline links to the east (Myanmar or Bangladesh) either. LNG is relatively secure and provides some inherent storage capabilities. While it is not as inexpensive as short-distance pipelines, the price differential isn’t the main challenge for natural gas imports in India.

The real challenge is the overall price-competitiveness of natural gas. While spot prices for gas were until recently low, they have risen after August 2020, and many analysts say future prices won’t be as low as much of 2020, which had a perfect storm of demand falls, favourable weather that muted demand spikes, COVID-19, etc. More importantly, India’s delivered price is much higher due to a combination of infrastructure costs (for regasification and domestic pipelines) and a steep taxation regime. States currently set their own tax rates that are over and above import or federal taxes. The state’s taxes can vary from, for example, 15 percent in Gujarat to 25 percent in Chhattisgarh (as of 2019). Admittedly, oil products may have higher taxes than natural gas has. However, both fall outside the Goods and Services Tax (GST) regime. This results in a much higher effective tax rate for many end-users as they cannot avail input tax credit.

The section on competitiveness of gas in power highlights the price issue in more detail.

The 15 percent target share of natural gas in the energy mix would entail a growth of about five times in absolute terms. This projection is based on inherent economy-linked growth in overall energy demand, which would roughly double by 2030. A five-fold growth in about a dozen years is challenging for any mainstream fuel. In this scenario, over and above the organic growth concurrent with a growing economy, gas would need to displace alternatives.

Space-heating requirements in India are trivial. Water-heating is overwhelmingly electric. Industrial demand for natural gas is thus far modest because of two reasons. On one hand, overall industrial demand is muted and on the other, industry that wants natural gas faces the challenge of access because of limited infrastructure. This sector has some growth potential, but it is nowhere near sufficient to help achieve the 15 percent target.

While fertilisers have historically been the priority use of natural gas, there is evidence that the use of nitrogenous fertilisers is too high when compared to those with other nutrients (based on the N:P:K ratio). Part of this is due to subsidies on fertilisers dominated by the ammonia variety (created using natural gas). Even if fertiliser use continues (see Figure 1), and there is mild growth commensurate with food production growth, it would be nowhere near enough to drive a tripling in the national use of natural gas.

Considering the limits of natural gas demand for above uses, electricity emerges as a key sector for analysis. It accounts for half of primary energy use. On paper, there is scope for electricity to drive the maximum increase in demand for gas. But this needs to be examined with a critical lens on its competitiveness.

Role of gas in electricity

We begin with an examination of the price competitiveness of gas-based electricity. There are two dominant components of electricity costs: capital costs and variable (operating) costs. For fossil fuel electricity, variable costs are overwhelmingly fuel costs. In contrast, RE is almost entirely capital expenditure.

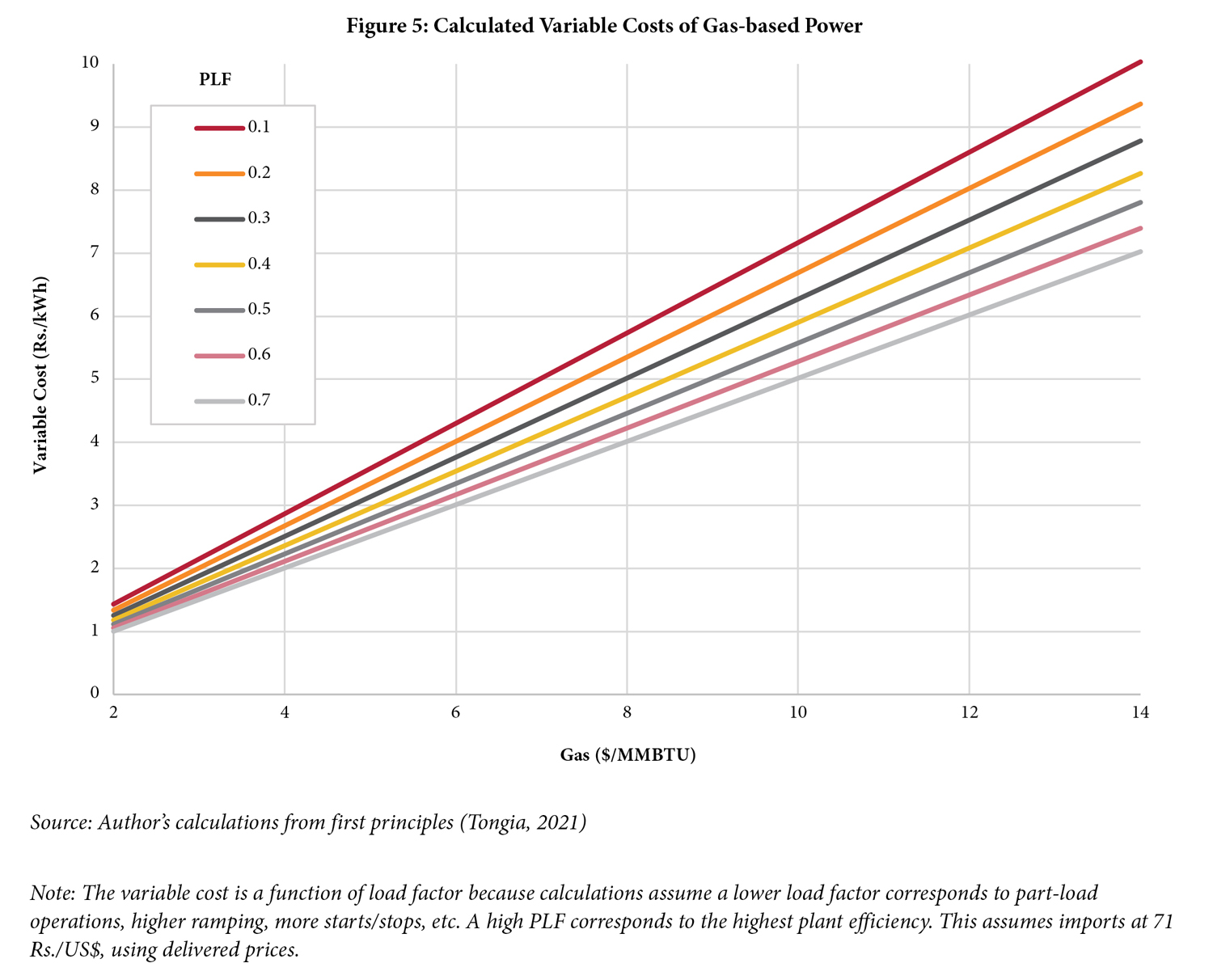

Variable costs for power are a function of the cost of incoming gas as well as plant efficiency. Efficiency is dictated by technology and design, but also depends on the duty cycle (full-load versus part-load operation). Modern combined cycle gas power plants are amongst the most efficient, far more so than coal power plants. Figure 5 shows the calculated variable cost of gas-based power. This analysis assumes a degradation of efficiency with falling PLF, thus raising variable costs.

Discussions with experts and details in Mehta (2021) indicate that imported LNG typically costs at least 8 US$/MMBTU delivered, corresponding to a variable cost above 4Rs./kWh.

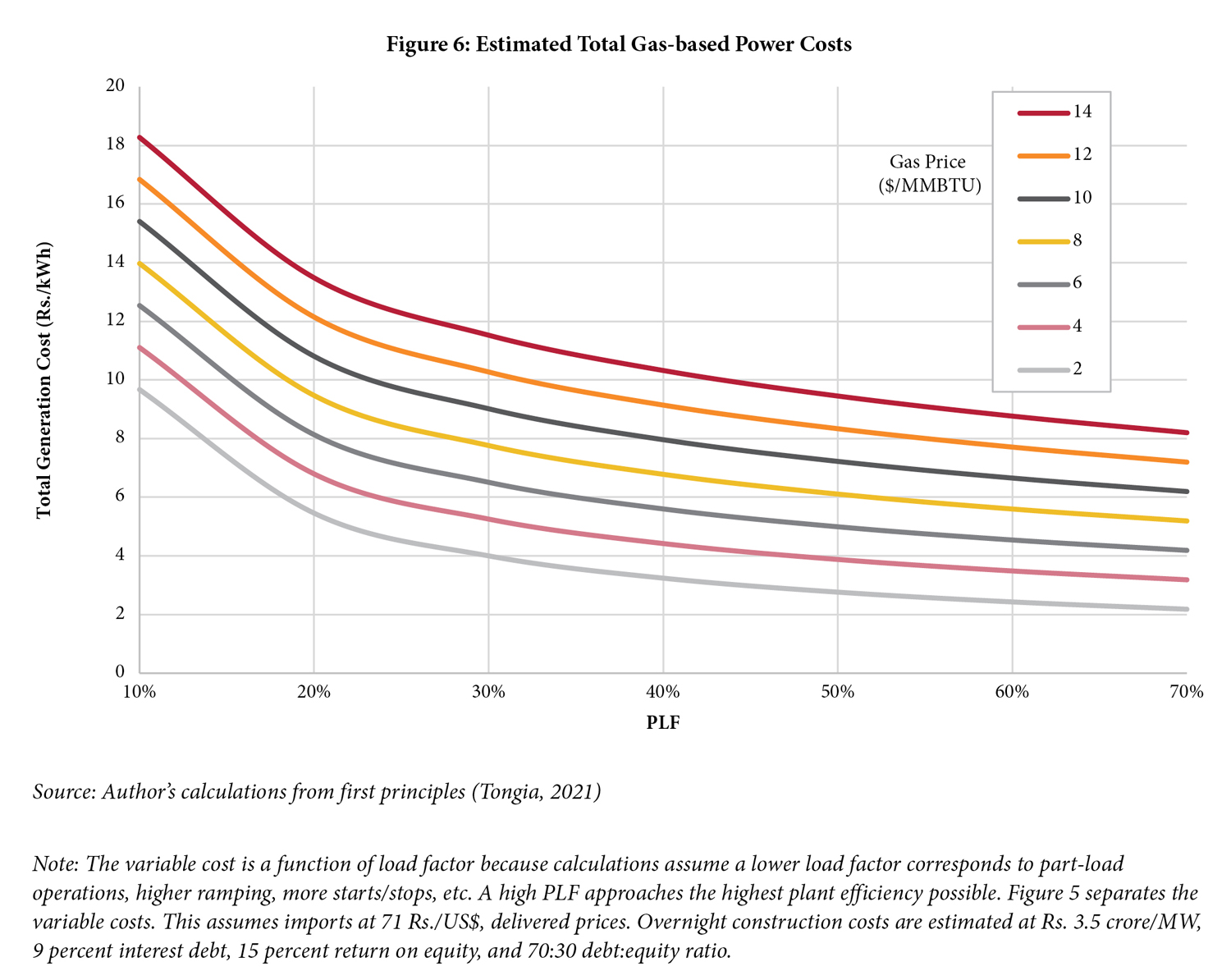

In addition to variable costs, there are fixed costs for the plant, the amortisation of which depends heavily on utilisation (plant load factor or PLF). Figure 6 shows the calculated total cost for a gas plant based on the two key factors – gas price and PLF.

The aggregate PLF for India’s gas power plant fleet is very low. It was below 24 percent in FY19, based on capacity and generation data from the Central Electricity Authority (CEA). PLFs at individual plants vary significantly, often based on ownership, which is a proxy to contracts for access to cheap gas. Nonetheless, even at high PLFs, the total cost of gas-based power is at least 5Rs./kWh, likely much higher in practice.

What are the alternatives and how do they compare? RE power just reached record lows at 2 Rs./kWh in November 2020. It is true that these were for specialised bids with a few unique characteristics, including focused offtake, waiver on surcharges for inter-state sales, etc. However, even otherwise, conservative RE price projections for quality bids (good location and counterparty) after including import duties and protective border tariffs, are below 2.75Rs./kWh, and falling.[5]

RE prices are so low they compete with the marginal (fuel) cost of coal across much of India. Coal generation costs vary significantly by location. At the pithead, the marginal cost can be as low as 1.3Rs./kWh, inclusive of taxes, levies, and the coal cess of 400 Rs./ton. For distant locations, which rely on expensive railways transport or imports, the variable cost can be over 3Rs./kWh. As a benchmark, NTPC’s average fuel (coal) cost has been close to 2 Rs./kWh for several years.[6]

While one cannot wish away capital costs, marginal costs are useful because they signal how the state load despatchers (grid operators) utilise available plants. The capital costs are often locked in under take-or-pay clauses through Power Purchase Agreements (PPAs), the use of which is predominant. Under PPAs, the incremental cost for a state buying coal power is roughly the fuel cost. In the absence of a PPA, bilateral sales are usually priced at total costs. Alternatively, for purchases from the power exchange, prices vary based on the level of competition. Some time periods see prices falling to near marginal costs, while other periods find higher prices, covering fixed costs for most bidders.

There is another reason why marginal costs are an important short-term pricing signal. India has ‘surplus’ capacity both of coal plants and gas plants (underutilised capacity). Thus, there is no incremental investment or CapEx involved in the short run. Of course, the marginal costs of RE are zero. But to a state buying power, RE costs are signalled as total costs. The surplus, even if it lasts only a few years, undercuts the value proposition of natural gas, which has low capital costs but higher fuel costs, more so in India. A new, supercritical-technology, efficient, load-flexible, and environmentally state-of-the-art coal power plant can have a total cost below 4Rs./kWh, assuming it has access to cheap coal – invariably at the pithead or minemouth – and operates at a reasonably high PLF.

Can gas be price competitive for non-RE hours?

Currently, gas in India does not compete well on price with coal or RE. RE as currently used is Variable RE (VRE) without any storage, and is thus only generated at selected times of the day. Isn’t there value in natural gas meeting the electricity demand during non-RE hours?

On the flip side, what happens when storage technologies, especially batteries, mature? With batteries, RE will turn into despatchable or ‘firm’ power. This solution easily beats natural gas on the environmental front. It meets not just time-of-day needs (e.g., by shifting solar output to the evening) but can also meet peaking and ramping requirements, where capacity is required only occasionally, including seasonally. This is discussed in more detail subsequently.

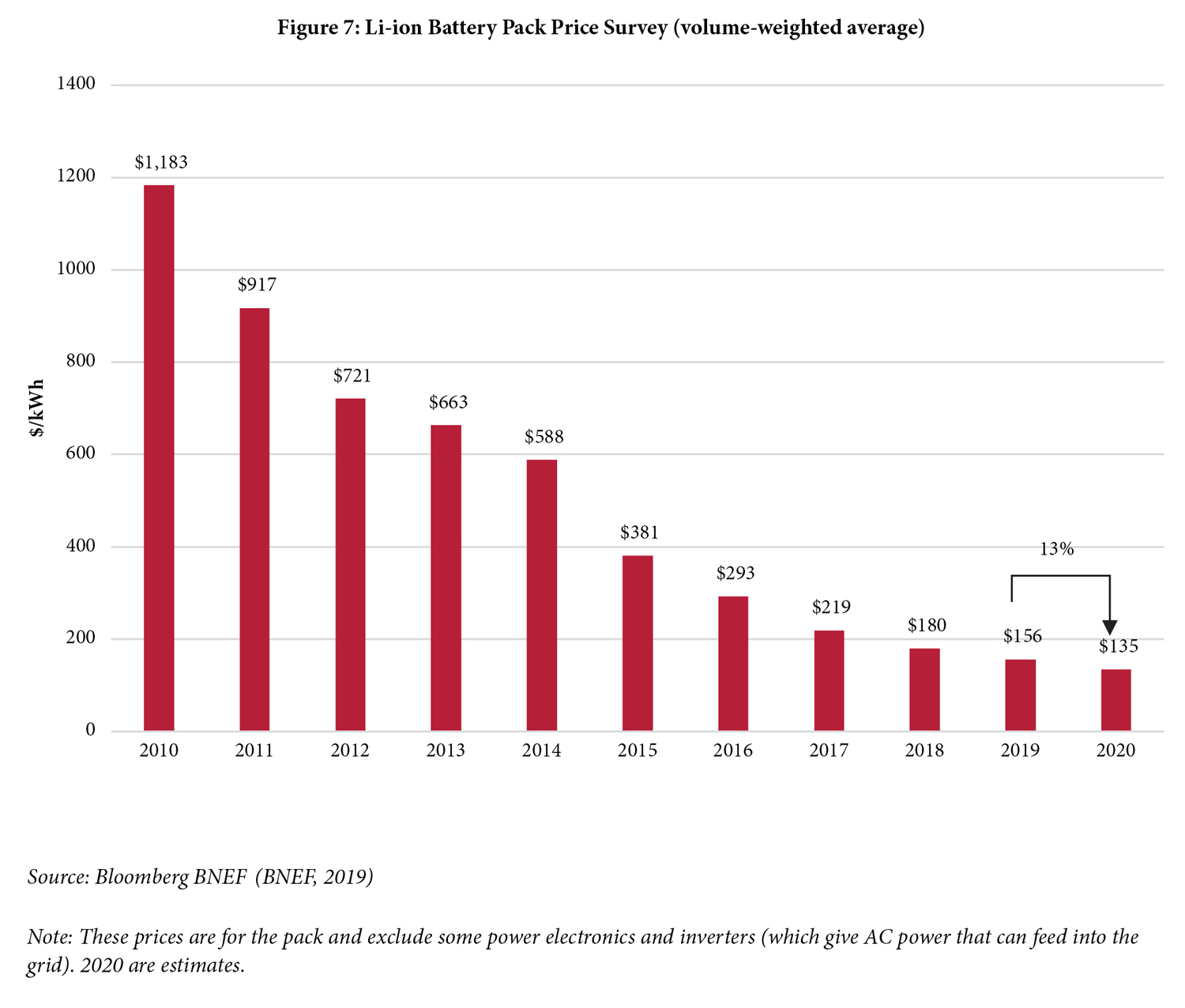

In the short run, batteries are expensive. In India, pumped hydro, the globally dominant storage technology, has limited deployment due to multiple reasons, most of which relate to competing uses of and duty cycle pressures on water. However, the price trends for batteries are falling aggressively, as seen in Figure 7.

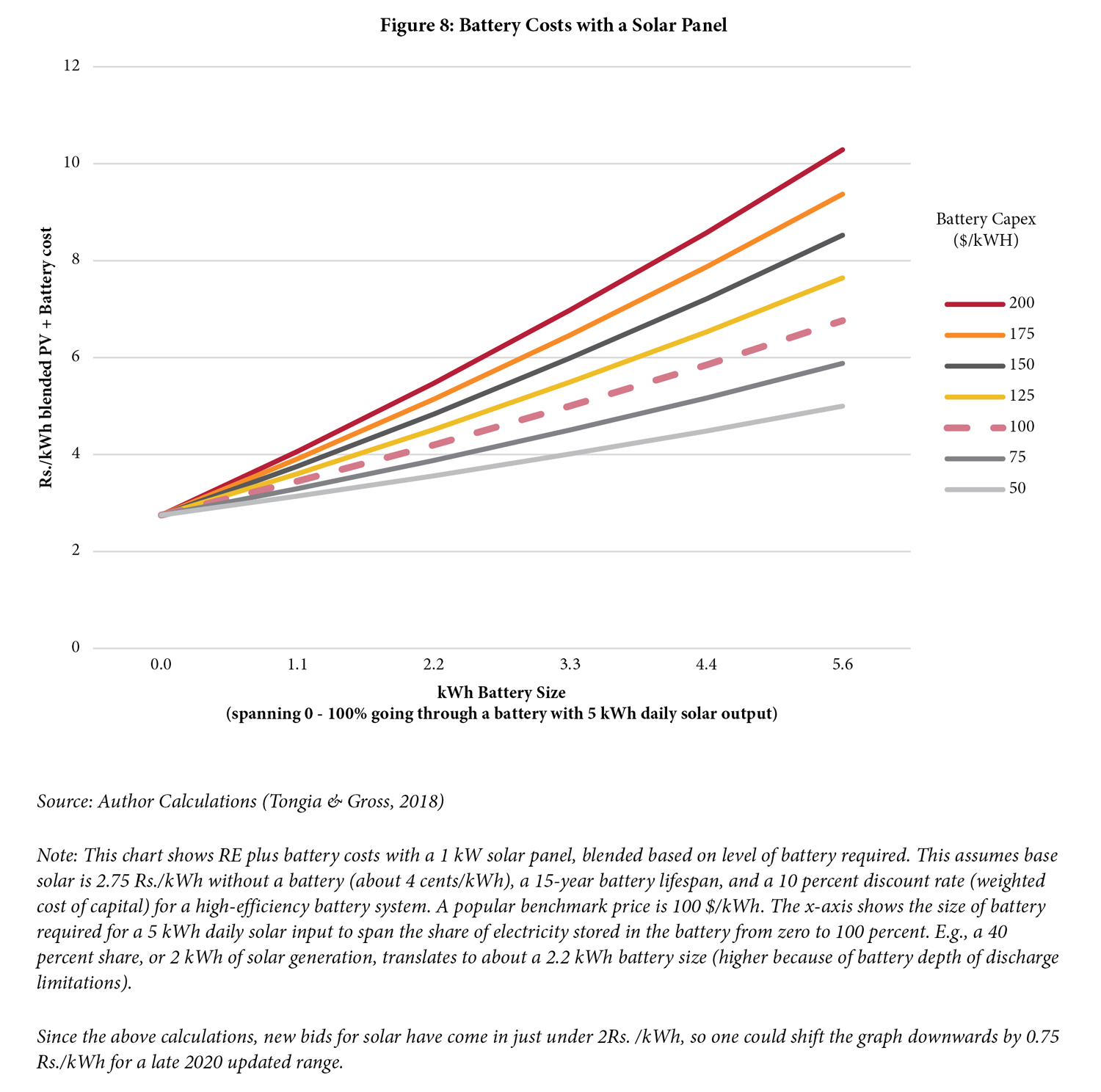

What does this mean for RE in electricity? Discussions with RE companies indicate that 2019-20 delivered, all-inclusive storage costs for grid-quality batteries (which can handle more cycles than automotive batteries, shown above) were well over 200 $/kWh and closer to 300 $/kWh, a price that includes the costs of power electronics and inverter, plus applicable taxes or duties. While these are capex-heavy technologies, there are also some operating costs, notably for cooling, which is important in India’s climate based on battery chemistry and operating specifications. Figure 8 shows the converted Rs./kWh implications of a range of all-inclusive capital costs for a battery, excluding O&M costs, combined with solar power. This figure also shows the blended costs based on how much battery you need—from no battery (pure solar) to 100 percent of the energy going through a battery.

To give a simplified calculation, in the long run, perhaps 35 percent of India’s power demand may be RE output-coincident. That would translate to an average of some 65 percent of it going through the battery.[7] In the short run, one doesn’t need a battery at all as most of the VRE can be absorbed as-is. The exact timeline for the switch depends on how demand, RE supply, and coal (fuel) prices evolve in the next few years.

This suggests that batteries will displace natural gas for firm, clean power in a few years unless very cheap gas is available. Global capital is relatively cheaper while Indian interest rates are typically high. In addition, in the absence of a carbon price, coal can remain competitive for a few more years, more so at locations near the pithead. In either of these cases, gas is not an economically competitive option for electricity in India. We revisit this issue again shortly.

Competitiveness of gas in non-power sectors

The 2021 India Energy Outlook by IEA indicates that industry will be a key sector for rising carbon emissions, growing in some years to surpass the power sector, which is relatively easy to decarbonise.

Given India’s development plans, industry has potential for growing the use of gas. Figure 1 shows that only a very small fraction of gas goes to industry today. A granular analysis of price-sensitivity and demand for gas by industry-type is beyond the scope of this paper. However, discussions with experts indicate, at best, a modest potential for natural gas, given competing pressures from two sides. For small-scale industries, any cheap fuel works well, including diesel, coal, etc. Small-scale industries can also use electricity, assuming the industrial process doesn’t require very high temperatures. This is despite the low cost of gas on a Rs./MMBTU basis compared to retail electricity of perhaps 8 Rs./kWh (which can be about triple the fuel costs of gas). This is because electricity is easy to utilise, does not require combustion or emissions control equipment, and, for many industries, energy costs are modest on an operating basis. On the other end of the scale, industries with a high share of energy cost often have dedicated coal conversion technologies, with pollution control equipment as required.

There is also a significant bottleneck due to the limited availability of natural gas at the user’s doorstep. As an example, over one lakh brick kilns use a few percent of India’s coal. They have no emissions control equipment and are very polluting. However, the government is focusing either on raising their efficiency or on making them switch from fired clay bricks to ‘cement bricks’, which use waste fly ash from coal power plants. Most of these kilns are nowhere near natural gas supplies. Even if gas is priced right, its physical availability for these kilns is a serious challenge. Moreover, coal, burned crudely, is very inexpensive on an energy basis.

City gas distribution (CGD) is one of the high-growth and high-potential segments for gas identified by the government. Other than industry, cooking and vehicles are two key uses for gas in cities.

Compressed Natural Gas (CNG) gained popularity for vehicles in Delhi, where a court mandate pushed its use for public transportation, displacing diesel. Pricing advantages also drove the use of CNG. Delhi enjoyed cheaper input gas under the administered pricing mechanism (APM), which kept per kilometre costs for gas measurably lower than for diesel. This called only for a modest retrofit cost for a petrol vehicle (few tens of thousands of rupees). Such vehicles also had a back-up option for using regular petrol. This helped users overcome concerns about not finding CNG re-fuelling stations. Unfortunately, it’s not clear how much more cheap gas is available for growth in the rest of the country.

Gas for transportation also faces competition in two directions. For smaller users, electric vehicles are becoming cost-competitive. For large users, especially over long distances, CNG hasn’t proven attractive. For bulk inter-city usage, this leaves LNG trucking or, in the longer run, hydrogen, as a possibility. However, scaling these is a challenge that calls for enormous infrastructure requirements.

Like CNG, electric vehicles (EVs) also enjoy attractiveness over liquid fuels because of per kilometre operating cost. In fact, EVs fare even better than CNG. Some states have issued specialised electricity rates for EVs. Depending on the price of this electricity, the operating cost of an EV can be several times lower than that of a CNG vehicle. In contrast, there remains a high upfront cost of the battery for an EV. However, even CNG has an upfront cost for the gas infrastructure. The earlier section exemplified the importance of batteries to India’s energy transition. Vehicles are, in fact, likely to drive battery technologies globally because, in mobility, their netback value is typically compared against more expensive liquid fuels instead of the power sector’s coal or even natural gas (which is cheap in the US and parts of the world).

When we consider cooking, the volume of gas that could be used is modest. Indian buildings have little heating demand. Importantly, instead of displacing coal, gas would displace LPG, more so only in urban areas (this ignores the displacement of biomass cooking, typically replaced by LPG as households move up the energy ladder). Thus, such a shift brings about a negligible change in pollution or carbon emissions. Use of natural gas, marketed as Pressurized Natural Gas (PNG), is driven mainly by consumer preference for convenience and cost-saving. But the latter is again an artefact of pricing regimes rather than of inherent technological advantages.[8]

The analysis so far has been through a simplified lens of cost competitiveness of natural gas compared to alternatives. It is also a static analysis. Are there specific shifts, ranging from changes in the market to technology or policy, which can dramatically move the needle?

Valuing externalities – Carbon

India’s commitments towards the Paris Accord (COP21) span a number of targets. The most important is the target of reducing greenhouse gas (GHG) emissions intensity by 33-35 percent in terms of Gross Domestic Product (GDP) by 2030 relative to a 2005 baseline. Given the expected growth of GDP, this still represents a net increase of emissions, albeit from a low base compared to global per capita emissions. There are additional pledges that could be viewed as mechanisms rather than outcomes. The commitment to have 40 percent of capacity based on non-fossil fuel is one such. India has also pledged to increase forest cover.

One limitation of this target of 40 percent non-fossil capacity is that it ignores utilisation of installed capacity. Generation from fossil fuels, not merely having installed capacity, is the problem. Secondly, all fossil fuels have been lumped in the same basket, which diminishes the carbon benefits of natural gas over coal. Unless India clarifies these in future notifications, this becomes a disincentive for natural gas.

While India doesn’t have an explicit carbon pricing mechanism, it has high taxes and levies on many fossil fuels. For petrol, these can entail half the retail cost or more. Coal has a 400Rs./tonne ‘coal cess’ that covers about 70 percent of India’s carbon emissions. But this cess translates to only a little over 3 $/ton of carbon dioxide (CO2). Estimates for the social cost of carbon are multiple times higher. India has a low GDP per capita and thus low damage functions. For strong mitigation, the High-Level Commission on Carbon Prices (2017) suggests a minimum 40 $/ton CO2 price to be meaningful, going up over time.

The coal cess, which began as a clean energy cess, currently ends up paying into the GST Compensation Fund. It translates to about 0.25Rs./kWh for electricity.[9] Thus, a 40 $/tonne CO2price entails an enormous increase. It would lead to a burden of close to 3 Rs./kWh of electricity. However, natural gas is not fossil-free, and would itself have an attendant carbon tax cost of about 1.4-1.6Rs./kWh depending on efficiency assumptions, leaving a spread of only about 1.5Rs./kWh versus coal (Ali & Tongia, 2020). As the section on gas-based electricity costs showed, even 40 $/ton CO2 is unlikely to be sufficient to make gas cost-effective with coal, more so when we consider only marginal costs, except in niche locations.

Importantly, higher carbon taxes would favour RE more than they would favour gas. RE is considered virtually zero-emissions during operations (there is a mild penalty on fossil fuel generators that lose efficiency if they operate a lower-than-rated output). Zero-emissions for RE exclude the carbon needed for manufacturing and installation. But even on a lifecycle emissions basis, RE still has a dramatic advantage over not just coal but also natural gas. Thus, any policy away from coal implicitly becomes an argument towards RE, not natural gas.

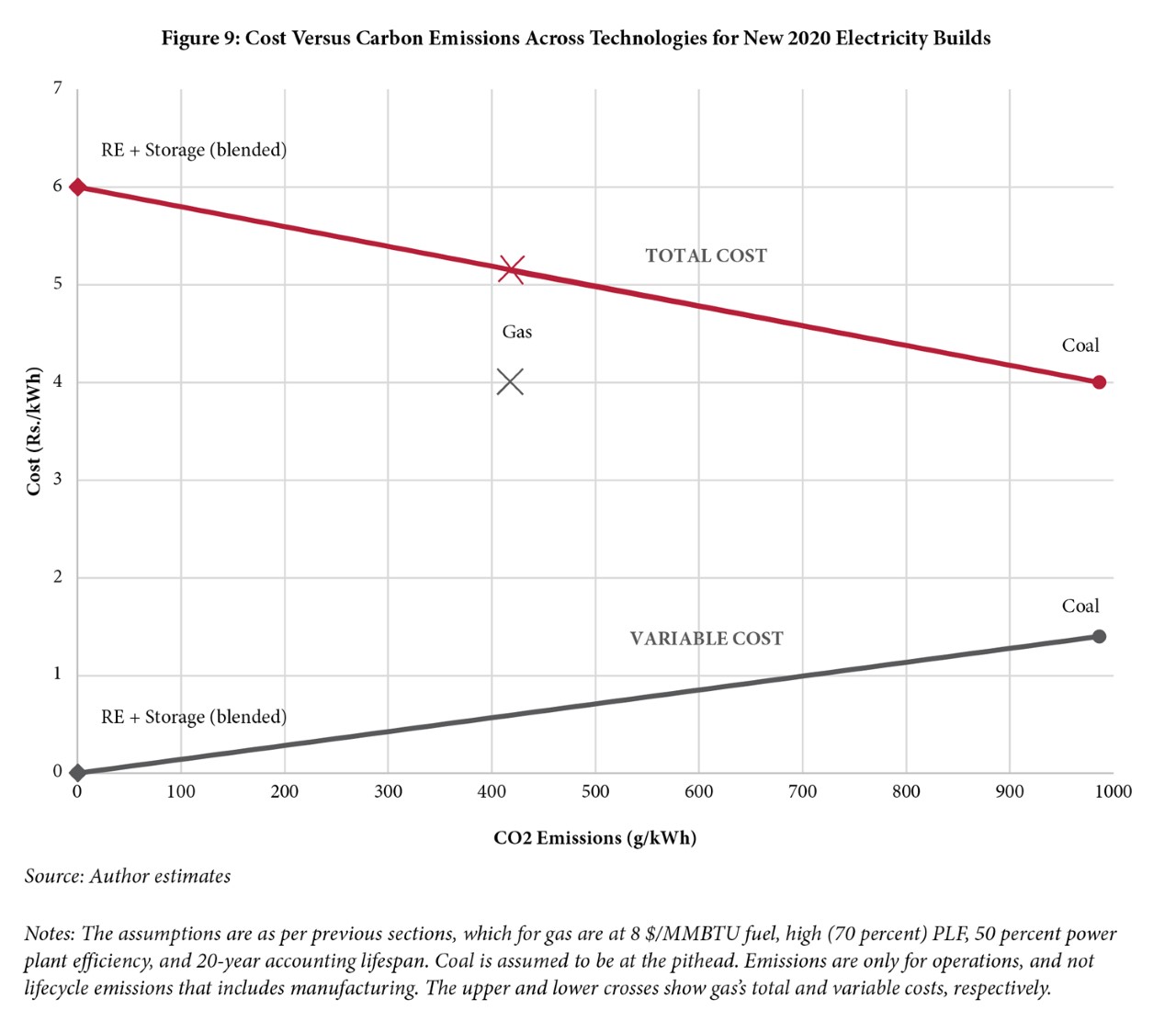

Figure 9 compares carbon emissions with costs for firm RE, coal, and gas; variable RE is far cheaper. When total costs (fuel plus capital) are considered, gas fits in the middle and appears to be virtually a linear blend of coal and RE. However, this is based on a number of assumptions that both may be unattainable in the short term and would shift in the long term. Calculations assume gas delivered at 8 $/MMBTU to the power plant, which is cheap for LNG-based supply as delivered today. It also assumes a specific blend of battery costs and size with RE, translating to 6Rs./kWh electricity costs.[10] With raw solar at 2 Rs./kWh, the 4 Rs./kWh for storage would be, for example, either a fall of battery capex to 100 $/kWh with 100 percent storage, or a 50 percent blending at 200 $/kWh battery capex. In the short run, even 50 percent storage would not be needed as VRE is sufficient. As the need for storage begins and then grows, the prices of batteries would fall. Coal could also improve in costs (for pithead plants) and may become more efficient with new technologies; this assumes 986 g CO2/kWh emissions from coal at the busbar, i.e., post auxiliary consumption. Thus, while there is a possibility for gas fitting in between (with the blue upper line), it may not last long as technologies evolve.

The upper line shows the total costs and not marginal costs. If we consider only marginal costs once constructed, shown in the orange line, gas drops out of competitiveness entirely.

A carbon tax wouldn’t make gas a winner. At a higher price of over 27 $/ton-CO2, coal power’s price rises to 6 Rs./kWh. But then gas’s price rises too. The only scenario for new gas capacity would entail inexpensive fuel supply, which remains challenging. Figure 9also assumes a high PLF for gas (and thus high efficiency), which wouldn’t materialise with high gas prices. And all of this is relevant only until battery costs fall further.

Valuing non-carbon environmental benefits of natural gas

Limiting carbon emissions is an important goal for the Government of India. But it is not necessarily the only concern, especially for states or consumers that worry about the price of power or more pressing immediate challenges such as local air pollution.

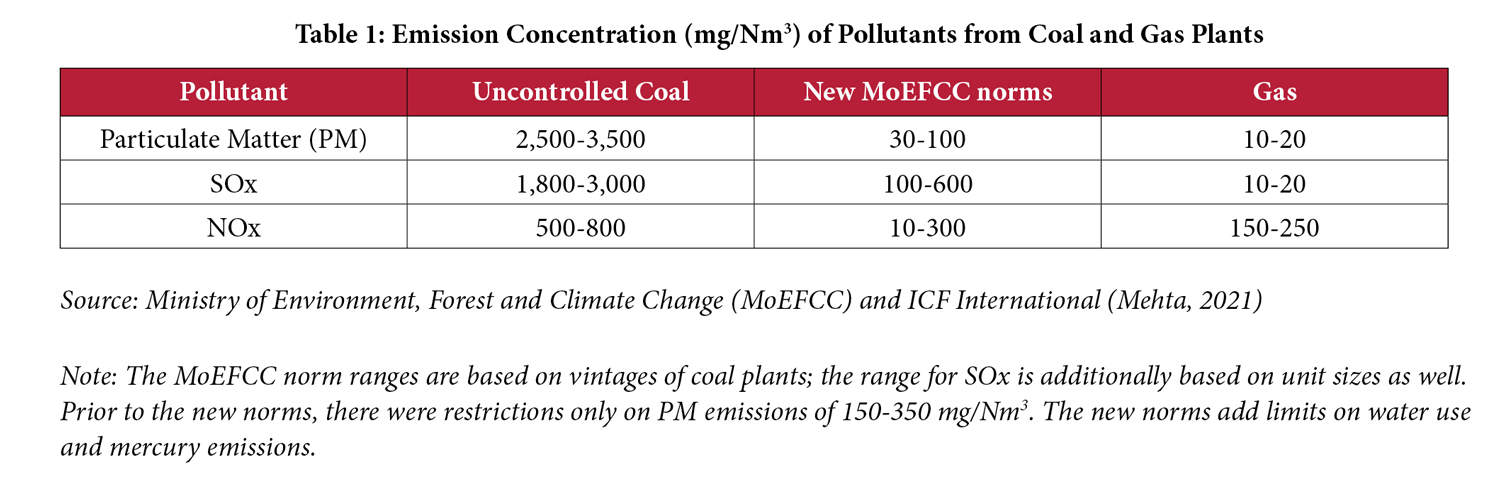

Table 1compares emissions between coal and natural gas, adding specifically the behaviour expected of coal plants as they comply with the newest environmental norms. The new norms for coal vary by plant vintage and size. Newer large plants are expected to be the cleanest, but, even then, natural gas is superior on most parameters, except NOx emissions. Even for the same plant, NOx emissions vary heavily based on combustion parameters, including ramping output up and down, a duty cycle we could reasonably ask of gas. Gas is also superior in terms of lower water requirements and dramatically lower emissions of mercury.

While gas and coal clearly emit differently, there is no emissions-trading market or other mechanism that sets a price for this pollution. The best estimate of the cost of emissions entails the cost of adding emissions control equipment to existing coal plants as a retrofit. Estimates vary based on required technology and utilisation (PLF). On average, they are in the order of half a rupee per kWh at modest PLFs (Srinivasan et al, 2018), but with a spread based on a range of assumptions. Experts believe the costs could fall slightly once suppliers begin to compete in earnest and there is design learning. This projection also excludes a handful of outlier power plants that are old and, thus, not only hard to upgrade but also have limited life ahead.

Thus, the clean advantage of gas over coal is real but modest. Again, the same argument favours RE over coal as emissions are virtually zero with the former.

Valuing non-environmental benefits of natural gas

How high is the non-environmental value of natural gas? On one hand, gas appears to afford low energy security as the growth of supply is disproportionately from imports. On the other hand, once gas pipeline infrastructure is established, gas supply is usually steady, barring rare mishaps, and avoids the hassle of coordinating periodic shipments of LPG, coal, or other batch-delivery fuels.

What natural gas doesn’t provide is high domestic employment, especially if it is imported. However, RE doesn’t provide large-scale jobs domestically either.[11] Most solar cells and even modules are also imported. China dominates the supply of both cells and modules (the latter are sometimes assembled in India) (Press Trust of India, 2018). Only coal disproportionately provides domestic jobs, albeit with high environmental costs of mining added to the externalities of coal combustion.

When we consider the addition of new gas capacity, the relevant question that arises is whether there is value in gas plants within a regime of high uncertainty of utilisation? Of course, such an addition is, at the minimum, several years away given the current surplus capacity of gas and coal power.

Between FY2011 and FY2016, there was a dramatic growth of coal-based electricity capacity, at more than double the growth of electricity demand. This drove India’s current surplus capacity and is also the reason for surplus or underutilisation of gas-based capacity. India also has extremely aggressive and ambitious plans for renewable energy, including achieving 175 GW of RE by 2022, and 450 GW by 2030.[12] It currently has about 90 GW of RE. It is unlikely to achieve the 175 GW target by 2022, but the trend remains in favour of RE.

If we ignore the dip in demand due to COVID-19, in a few years, by the mid-2020s, the surplus will disappear due to rising demand. This exhaustion could be exacerbated by the pending implementation of stringent environmental norms at coal power plants. This may result in the shutting down of some capacity that is unable to comply either on technical grounds (not enough space for the retrofits) or on economic grounds (old plants with modest life and/or low expected utilisation).

It is more difficult to predict what will happen if India’s ambitious RE targets don’t materialise on time and demand continues to grow, especially ‘net demand’, which is the measure of demand after accounting for variable RE. Adding new coal-based capacity may be difficult. Not only is there a purposeful shift away from coal but also simply because such additional capacity may not be utilised much because of the primacy of RE for parts of the day. This is compounded by the question of who will build, rather, finance, such new coal power plants. Gas plants are also an option to revisit in a few years, after existing surplus capacity is exhausted and demand rises. They can be built faster than coal plants.

After surplus gas power capacity is used up, would the economics align for adding new gas power capacity at a modest scale? The answer to this question would require many assumptions on the future prices of gas and nuances of location (both coal and RE are location-sensitive for logistical reasons). Even if the economics aligned for niches, their impact on carbon emissions would be limited (as shown previously on a per unit basis and in aggregate in the next section).

There is a value-proposition for natural gas to act as a peaker rather than as new capacity. India’s electricity grid regularly has peak electricity demand in the evening, when solar output falls to zero. Even with demand shifted to match solar output, for example, shifting irrigation loads, the ‘net demand’ (removing RE supply) peaks in the evening. It isn’t viable to add a new coal power plant to operate only for a few hours a day. Also, batteries are still expensive, which limits the use of RE for such peak power.

Tongia (2021) shows a bounding exercise for peaking operations. Gas turns out to be quite useful as a value proposition but is low in volumes required. Even if all existing but underutilised gas capacity were to be turned on for a few hours every day (adding some 15 GW of net additional output), this would translate only to about 3 percent of current total natural gas consumption. While, on paper, this translates to several years’ worth of plausible incremental peak evening demand, in the short run, such a peak can even be met by existing but underutilised coal plants, not to mention hydro, which is an optimal peaker.

What about the value of natural gas for grid stability and ramping operations? While it is true that natural gas power plants have faster ramping capability than coal, there are three wrinkles to this argument. First, the really fast capabilities of natural gas are for open or simple cycle designs, which are rare in India. Combined-cycle power plants were favoured for their higher efficiency, which makes their output less expensive on a per kWh basis, assuming a reasonable utilisation. Unfortunately, PLFs have fallen. Secondly, even if the per minute ramp for combined cycle natural gas plants is attractive in percentage terms, say, over 5 percent per minute, the typical operating fleet of gas at any given minute is quite low–in 2019, it was about 6 GW. In comparison, even ‘slow’ coal could ramp at least at 0.5 percent per minute, if not 1 percent as per specs. The aggregate ramping from the typical 120-140 GW of coal in operation at any given time overwhelms the higher percentage ramp rate that gas offers. Lastly, like Australia’s recent grid-scale deployment showed, batteries can offer even greater value for grid stability through frequency support, ramping, and other ancillary-services (services that keep the grid stable, instead of merely providing energy).

Even the upper bound of gas’s impact on India’s carbon emissions is not much

As the above sections show, natural gas is squeezed between cheap coal and clean RE; the latter is already less expensive if considered without storage. How much gas ultimately gets used depends on what the alternatives are.

We can set aside price and corresponding demand issues and, as a bounding exercise, extrapolate the environmental impact of a very high natural gas scenario. If we assume a 15 percent share for gas by 2030, which would be on a growing base, what does this achieve for carbon emissions? The answer to that depends on what gas displaces as it grows in share. The upper bound for the carbon value of natural gas would be achieved only if it displaces coal.

India’s total emissions are currently at half the world per capita average. They total about 7 percent of global emissions. Let us hypothesise an aggressively high (but unlikely) 10 percent share of global emissions for India by 2030, with no rise in global emissions. Let us also assume all this gas avoids coal. The 10 percent absolute rise of gas’s future share of energy, at coal’s expense, isn’t all a carbon saving. Even gas has, say, half the CO2 emissions of coal. Thus, we’re talking of half of 10 percent (coal mix displacement) of 10 percent (global share), or a crude estimation of a 0.5 percent shift in global emissions, at most.

In reality, India is unlikely to reach 10 percent of global emissions by 2030. Also, some natural gas use may displace other sources of energy, including LPG (cooking) and petrol/diesel (transportation). Combined with the sheer implausibility of a 15 percent share for natural gas in India’s future energy mix, this suggests that even growing natural gas use may, realistically, have an impact of only 0.1-0.2 percent on the global scale, for a country that is a perhaps a sixth of the global population. Such a shift is not to be ignored, but it is not the game-changer many hope for.

What should India be doing in the larger Future Energy space?

For a variety of reasons, India is unlikely to need natural gas to comply with its climate commitments, made at COP21 in Paris. This doesn’t mean natural gas has no role or future, but simply that carbon alone won’t be its driver.

The calculations thus far make assumptions about both the availability of cheap-enough gas and a plausible evolution of technologies and regulations. The US discovered cheap shale gas through fracking. India is attempting new gas fields, but the supply track record has been poor so far, notably for the KGD basin. Aggressive sourcing of cheap gas will obviously help increase gas uptake but finding it is easier said than done.

If India becomes more aggressive in tackling local air pollution, then the use of gas may grow. In pockets of industrial use, local pollution may be addressed by natural gas (given small industries usually can’t afford the same emissions control solutions as large power plants and may not be able to use coal). However, even here, the aggregate impact on national carbon emissions would remain modest, primarily because industrial use of relevant fossil fuels is itself modest. This doesn’t mean India should be ignoring gas, especially if it displaces dirtier alternatives that include not just coal but also Petcoke or wastes burned haphazardly.

One of the biggest challenges arises from the enormous uncertainty in this space, not merely in terms of prices but also with respect to technology changes. While natural gas prices are expected to remain low, even that doesn’t necessarily translate into lower delivered prices of gas to consumers without a number of policy shifts, such as on taxation. As of now, natural gas is outside the GST regime. Adding it to GST would increase its attractiveness to many end-users, especially industrial ones (electricity also remains outside the GST ambit for now).

Infrastructure is a more challenging question. To what extent should India commit to building natural gas infrastructure, which is highly capital-intensive? Many other countries are attempting to move away from natural gas as part of their vision towards becoming carbon neutral (‘net-zero’) within a few decades. Electrification of transportation, cooking, and heating are the pushes, but these require significant investments. Some of these go hand-in-hand with other changes, e.g., for space heating, use of heat pumps combined with envelope (insulation) improvements (Tsafos, 2020).

Gas infrastructure is often designed for a much longer life than end-usage equipment, even power plants. India may want to think hard about this aspect of the transition. For India, a better framing would include examining to what extent natural gas enables a plateau of its carbon emissions before it jumps to zero emissions. Is aggressive building of gas infrastructure a driver to lower emissions, especially by displacing coal, or a lock-in that risks delaying even greener solutions such as RE? Could it become a stranded asset? On the flip side, would not having accessible gas for consumers end up extending the life of coal? India should evolve a consistent framework for the option value gas provides, especially for a world with price, volume, demand, and technology uncertainty.

Budget 2021 announced a National Hydrogen Mission, but the role of gas in coordination with it hasn’t been part of planning yet. Given the immense gas infrastructure buildouts underway, an important question becomes how much of this infrastructure can be re-used for hydrogen delivery? Current technologies limit a blend to perhaps 20% hydrogen, at best. Can India innovate to give the infrastructure dual use potential, with minimal extra cost? This wouldn’t make sense for homes and cooking, but perhaps for bulk consumers.

Ultimately, policies for natural gas in India should not be determined in isolation but rather within a broader, holistic framework for energy. Under such a wider lens, a few of the high-level needs for India’s energy policy are:

- Better signalling of prices and incentives

- Overcoming structural distortions

- Innovation and enabling changes, even if disruptive, both in technologies and business models

All of these would help the rise of gas but would also enable other shifts, some of which may compete with gas.

Better signalling starts with the accurate signalling of marginal and average costs of energy, as well as demand at a granular level, for example, differentiated by location and time of day. This also extends to proper signalling of externalities such as pollution such that cost-effective solutions can be found.[13] Such a framework would also enable more serious thought towards co-benefits of technologies or solutions.

Structural distortions create winners and losers based not on performance but on factors such as ownership, location, legacy contracts, etc., of the competing entities. In case of natural gas, state, central, and private sector power plants are often treated differently by electricity distribution companies (DisComs). Select public sector power plants even enjoy priority access to cheaper natural gas.

Lastly, technology shifts should be enabled and not resisted even if they displace the incumbents. As smart grids and storage technologies rise, these should enable new entrants as well as edge-based energy solutions. For example, these could enable a greater role of natural gas and clean-tech for tri-gen solutions (heating, cooling, and electricity). Tri-gen is much more feasible if one is allowed to sell energy to others, allowing optimal economies of scale. Current policies disallow third-party electricity sales (beyond a recent exception created for electric vehicle charging stations). This exemplifies the area of greatest challenge: the rethinking of DisComs.

Natural gas is unlikely to be the bridge fuel for India. But it may play a wedge (portfolio) role within India’s clean energy trajectory. Any growth of gas should be a possible outcome, and not an objective function. Natural gas has a role with a higher value proposition than just its volume would indicate. Gas may be non-zero carbon but can coexist in a high-RE future, especially until India achieves net-zero emissions, which is likely multiple decades away. However, its value proposition or viability won’t last forever. It will only decrease over time as other solutions, including storage or hydrogen, mature. India needs to push for all solutions that accelerate a clean transition, while also being mindful of ensuring this is a Just Transition.

Ali, M. S. & Tongia, R. (2020). Pricing Carbon Externality: Context, Theory, Evidence and Lessons for India. In R. Tongia and A. Sehgal (Eds.) Future of Coal in India: Smooth Transition or Bumpy Road Ahead?. Notion Press and Brookings India: New Delhi.

Bloomberg NEF. (2019). Lithium-Ion Price Survey.

BP (2020). BP Statistical Review of World Energy 2020.

CEA. (n.d.). Monthly Executive Summary Reports. Retrieved from URL https://cea.nic.in/executive-summary-report/?lang=en

Gulati, A. & Banerjee, P. (2021). Fertilisers: A regulatory dilemma?. In V. S. Mehta (Ed.). The Next Stop: Natural Gas and India’s Journey to a Clean Energy Future. New Delhi: HarperCollins Publishers.

High-Level Commission on Carbon Prices (2017). Report of the High-Level Commission on Carbon Prices. Washington, DC: World Bank. Retrieved from URL https://static1.squarespace.com/static/54ff9c5ce4b0a53decccfb4c/t/59b7f2409f8dce5316811916/1505227332748/CarbonPricing_FullReport.pdf

IEA (2019a). World Energy Balances. IEA, Paris.

IEA (2019b). Global Gas Security Review 2019. Retrieved from URL https://www.iea.org/reports/global-gas-security-review-2019

IEA (2021). India Energy Outlook 2021, IEA, Paris. Retrieved from URL https://www.iea.org/reports/india-energy-outlook-2021

Mehta, V. S. (ed.) (2021). The Next Stop: Natural Gas and India’s Journey to a Clean Energy Future. HarperCollins: New Delhi.

Ministry of Power. (2007). Annual Report 2006-07. Retrieved from URL https://powermin.gov.in/sites/default/files/uploads/ar06_07.pdf

Niti Aayog (n.d.). India Energy Dashboards. Accessed on 16th January. https://niti.gov.in/edm/

Press Trust of India (2016). India to increase share of gas in energy mix to 15 per cent: Union Petroleum Minister Dharmendra Pradhan. Indian Express. Retrieved from URL https://indianexpress.com/article/india/india-news-india/india-to-increase-share-of-gas-in-energy-mix-to-15-per-cent-union-petroleum minister-dharmendra-pradhan-3017136/

Press Trust of India (2018). China accounts for 89% of India’s total solar cells imports in 2017-18, Business Standard: New Delhi. Retrieved from URL https://www.business-standard.com/article/economy-policy/chinaaccounts-for-89-of-india-s-total-solar-cells-imports in-2017-18-118080100849_1.html

Srinivasan S., Roshna N., Guttikunda S., Kanudia A., Saif S., & Asundi J. (2018). Benefit Cost Analysis of Emission Standards for Coal-based Thermal Power Plants in India. (CSTEP-Report-2018-06).

Tongia, R. & Gross, S. (2018, September). Working to turn ambition into reality: The politics and economics of India’s turn to renewable power. Paper #4 in the Cross-Brookings Initiative on Energy and Climate Paper Series.

Tongia, R. (2021). Power: Niche Potential?. In V. S. Mehta (Ed.). The Next Stop: Natural Gas and India’s Journey to a Clean Energy Future. New Delhi: HarperCollins Publishers.

Tsafos, N. (2020). How Will Natural Gas Fare in the Energy Transition?, CSIS Report (January 14, 2020).

FOOTNOTES

[1] The initial pronouncement for growing gas from 6.5 percent to 15 percent by the Petroleum Minister Dharmendra Pradhan lacked a timeline. Most official calculations are only for commercial fuels and, thus, exclude measurable use of informal biomass. If we add such biomass, for which data are scarce and heavily assumption-laden, the 2015 share of gas in the primary energy mix would be lower than 6.5 percent, likely closer to 5 percent.

[2] This assumes so-termed green hydrogen, produced in a manner that doesn’t increase carbon emissions, instead of more traditional large-scale hydrogen today, which is produced from methane (natural gas) and thus is not considered green. There is the possibility to use natural gas to produce hydrogen but remove and sequester the carbon, so-termed “blue hydrogen”, but this is not widespread.

[3] See NITI Aayog Energy Dashboard for November 15, 2020.

[4] It is beyond the scope of this paper to examine gas pricing regimes.

[5] These are developer bid prices as Levelized Cost of Energy (LCOE), without factoring in system level costs such as transmission or balancing requirements.

[6] Compiled from NTPC Annual Investor Meet presentations (multiple years).

[7] India’s demand shape curve (load profile) is relatively flat on a daily basis. While some amount of load-shifting from the night to the day (especially for agricultural pumps) is feasible, this doesn’t impact the peak evening demand measurably, especially since pump-sets are ostensibly not supplied power during the evening peak. Given the PLF of solar is 25 percent, if demand were a flat line, we’d find a ratio of 75:25 for battery vs. non-battery. Ongoing analysis suggests some improvement in this ratio. The portal carbontracker.in shows real-time shape curves by type of fuel (RE, coal, gas, etc.).

[8] Historically, city gas networks were given cheaper incoming gas supply because they were declared a ‘priority sector’, like fertilisers.

[9] The exact figure depends on a number of assumptions, including inherent coal quality as well as the efficiency of conversion. Another set of official figures leads to a price closer to 4 $/ton carbon.

[10] Recent ‘Round The Clock’ (RTC) bids in India for blended RE and storage came in much cheaper than shown, but those bids had very little storage volumes.

[11] After installation, the remaining jobs for RE are overwhelmingly for cleaning, a low-value-add component of ‘maintenance’.

[12] Because of the lower capacity factors for RE, 1 GW of RE capacity isn’t the same as 1 GW of coal. Depending on the usage of coal (and current load factors for coal are low), RE is between 2-3 times lower in terms of annual generation per GW of capacity.

[13] Proper signalling will expand the portfolio of options beyond the supply side (like solar), to give impetus to energy efficiency, storage, demand response, etc.

Rahul Tongia

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.