The escalating climate crisis necessitates large-scale mobilisation of financial resources for both mitigation and adaptation efforts. Several studies have assessed capital investment needs for climate action, especially for mitigation measures. However, various estimates of climate finance that are available globally as well as for EMEs are often non-comparable because they are based on different objectives, time horizons, baselines and the scope of sectors covered. Another challenge with most of these estimates is that they rely on top-down approaches, which make broad assumptions and do not account for local and sectoral variations.

Our study ‘An Assessment of Climate Finance – Nine G20 Emerging Economies’[1] examines the climate finance requirements of nine EMEs (Argentina, Brazil, China, India, Indonesia, Mexico, the Russian Federation, South Africa, and Türkiye) from 2022 to 2030[2]. All the EMEs selected are a part of the G20 and they together account for 30 per cent of global gross domestic product (GDP), 47 per cent of global population and 30 per cent of global carbon emissions. The study covers the four highest carbon emitting sectors – power, road transport, cement, and steel – which cumulatively constitute 40 per cent of carbon emissions in the nine EMEs selected for the study.

The study estimates climate finance or additional capital expenditure (capex) required for climate mitigation purely on account of transition to a low carbon economy, over and above the business-as-usual (BAU) needs of investment needed for expected economic growth. Climate finance for the power sector includes the capex for generation as well as pumped and battery storage. The road transport sector entails additional capex for transitioning from internal combustion engine vehicles (ICEVs) to electric vehicles (EVs) as well as for developing the charging infrastructure. In the cement and steel sectors, different investment pathways such as energy efficiency, renewable energy, alternative fuels, carbon capture and storage (CCS), and clinker substitution (in the case of cement sector) were considered for decarbonising existing and new capacities up to 2030.

Power Sector

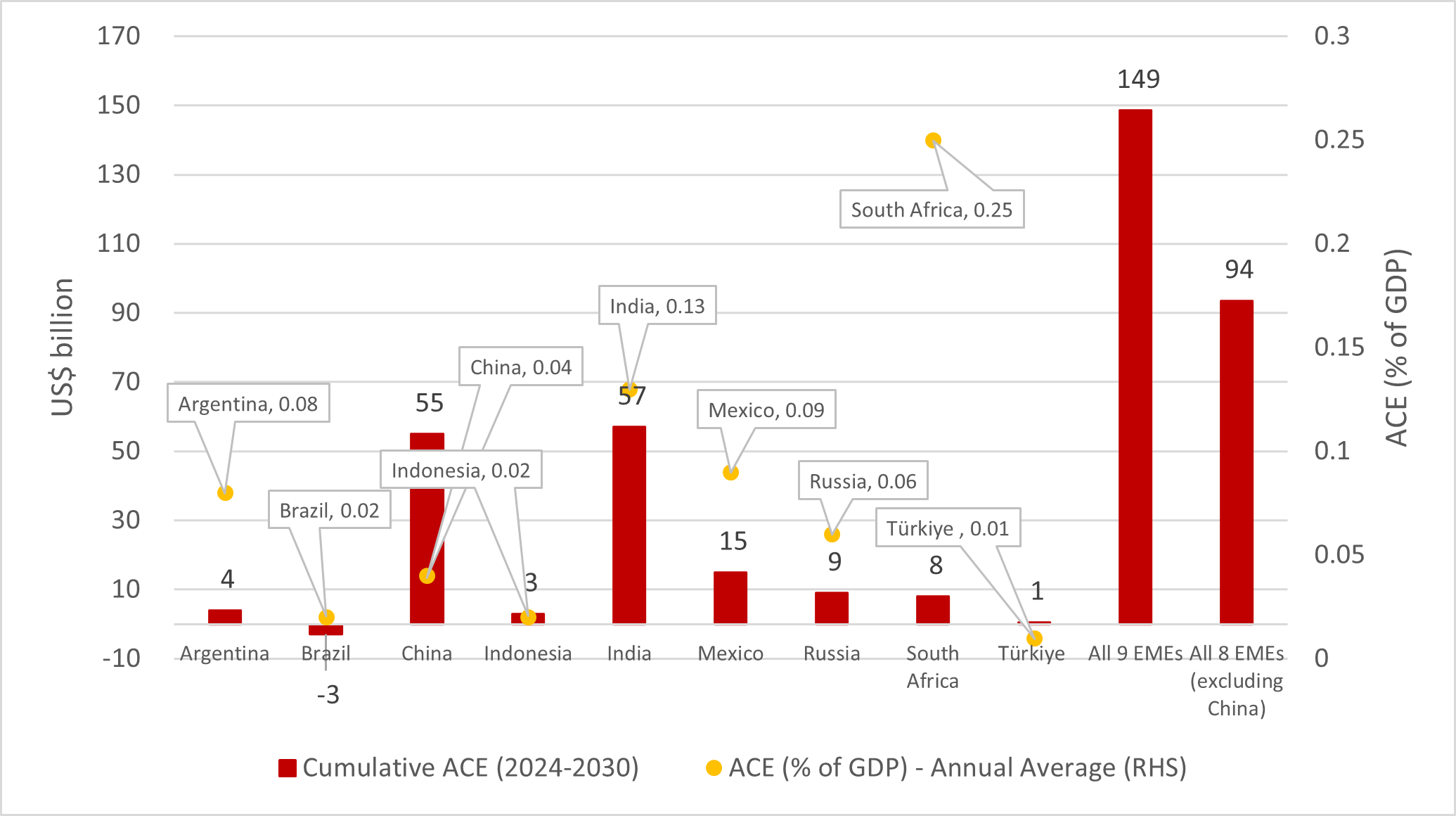

Climate finance for the nine economies for power generation for 2024-2030 is estimated at $121 billion. While capital expenditure for fossil-based plants is estimated to reduce by $156

billion, that for non-fossil-fuel based power sources is expected to increase by $277 billion. The unit capital cost of producing solar and wind energy has declined to the extent where it is now lower than that of producing unit cost of fossil-fuel based energy in many economies. The cost of solar panels (for solar energy) and wind turbines (for wind energy) declined by 83 per cent and 42 per cent, respectively, over the last 12 years.

Pumped and battery storage costs for renewables are estimated to involve an additional capital expenditure of $28 billion. The overall climate finance for the power sector for the nine economies is estimated at $149 billion for 2024-30, which translates to $21 billion annually (Figure 1).

Excluding China, it is estimated that the other eight other economies would require capex of $71 billion for power generation for 2024-2030. However, with the addition of storage costs, cumulative climate finance for the eight economies is estimated at $94 billion which works out to $13 billion annually (Figure 1).

Figure 1: Country-wise ACE Requirement – Power Sector (2024-30)

ACE – Additional Capital Expenditure.

Source: Authors’ calculations.

Road Transport Sector

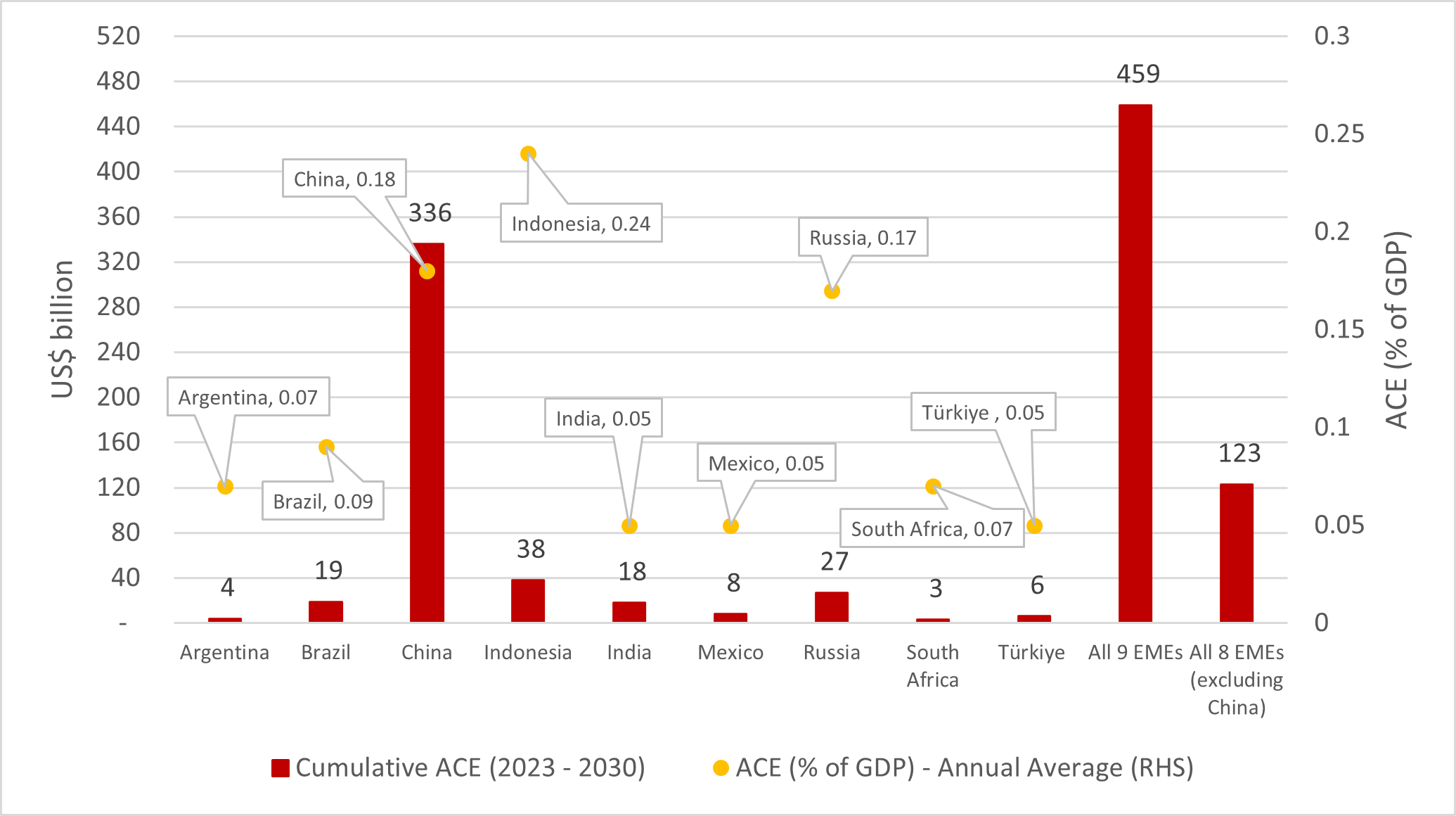

Climate finance for all the nine economies for electrification of the road transport vehicle fleet is estimated at $(-)5 billion for 2023-2030. This is because vehicle sales in China are projected to decline to 72.3 million units in 2030 from 84.7 million units in 2022. Therefore, China is expected to save capex on road transport. However, including additional capex for building the charging infrastructure, aggregate capex for the road transport sector for the nine economies is estimated at $459 billion (annual average of $58 billion) from 2023 to 2030. This is driven largely by China as it is developing high-speed charging infrastructure for its EVs, the cost of which is seven times higher than that of slow-speed chargers. Excluding China, capex for the other eight economies from 2023 to 2030 is estimated at $105 billion for switching over from ICEVs to EVs, and an additional $19 billion for building the charging infrastructure. The total capex for the eight other economies works out to $123 billion or $4 billion, annually (Figure 2).

Figure 2: Country-wise ACE Requirement – Road Transport Sector (2023-30)

ACE – Additional Capital Expenditure.

Source: Authors’ calculations.

Steel and Cement Sectors

Cement and steel are hard-to-abate sectors as their production processes are highly energy and emission-intensive. Therefore, decarbonising them requires a diverse mix of low-carbon solutions. Various decarbonisation options for the steel and cement sectors can be classified into five broad categories: (i) energy efficiency; (ii) use of renewable energy; (iii) use of alternative fuels; (iv) carbon management; (v) and clinker substitution in the case of cement industry. Transitioning to alternative energy sources and energy-efficient systems alone is insufficient to mitigate climate change impacts caused by the steel and cement sectors. Actively removing and storing CO2 through carbon management – CCS technology – is essential to achieve large reductions in carbon emissions, complementing the other clean energy solutions.

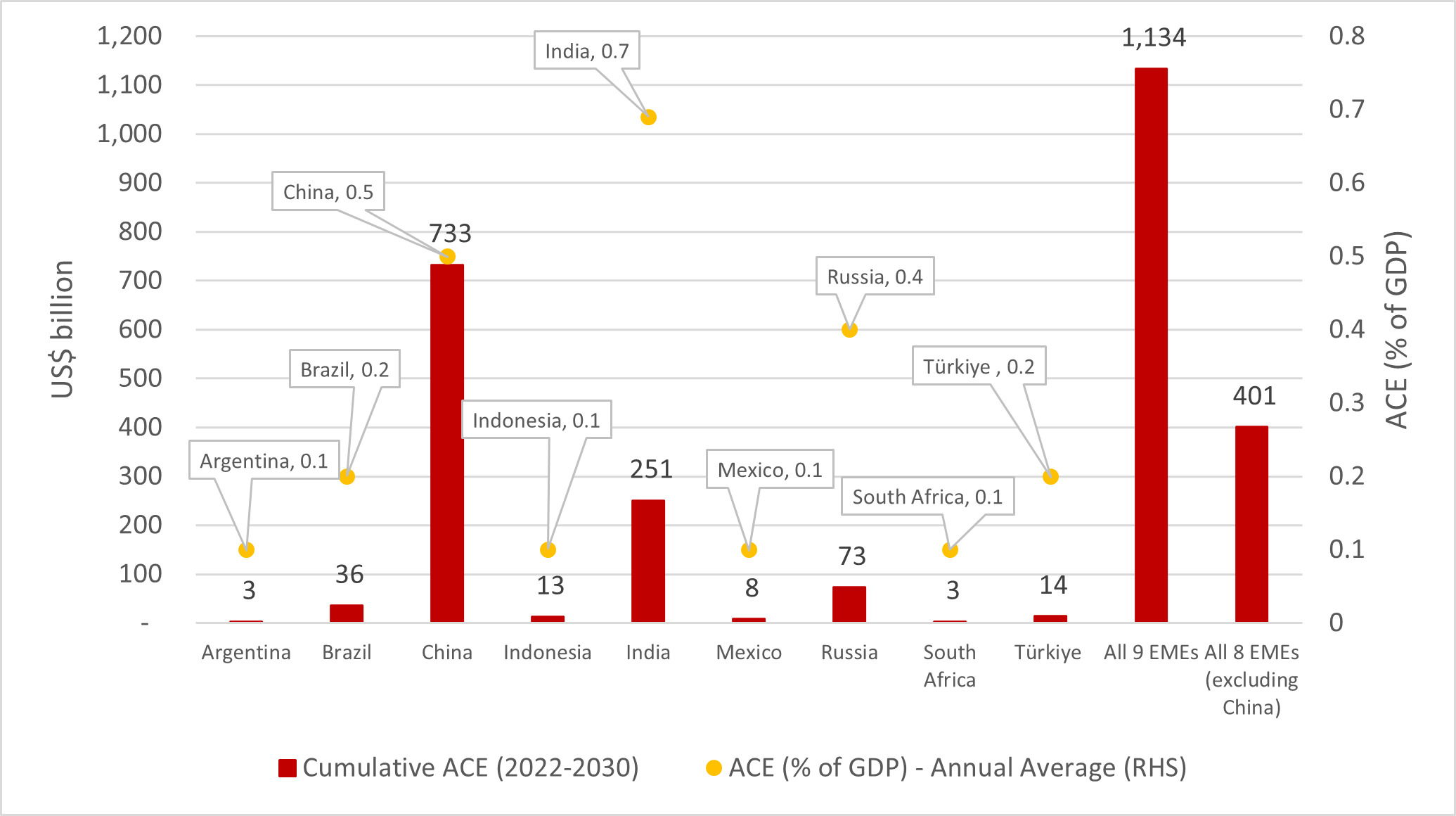

For 2022-30, climate finance required to mitigate CO2 emissions from the steel sector across the nine economies is estimated at $1.2 trillion or $126 billion annually. However, China alone needs 65 per cent of this estimated capex to decarbonise its steel sector. Excluding China, the eight other economies would need $401 billion or $45 billion annually, on an average (Figure 3).

Figure 3: Country-wise ACE Requirement – Steel Sector (2022-30)

ACE – Additional Capital Expenditure.

Source: Authors’ calculations.

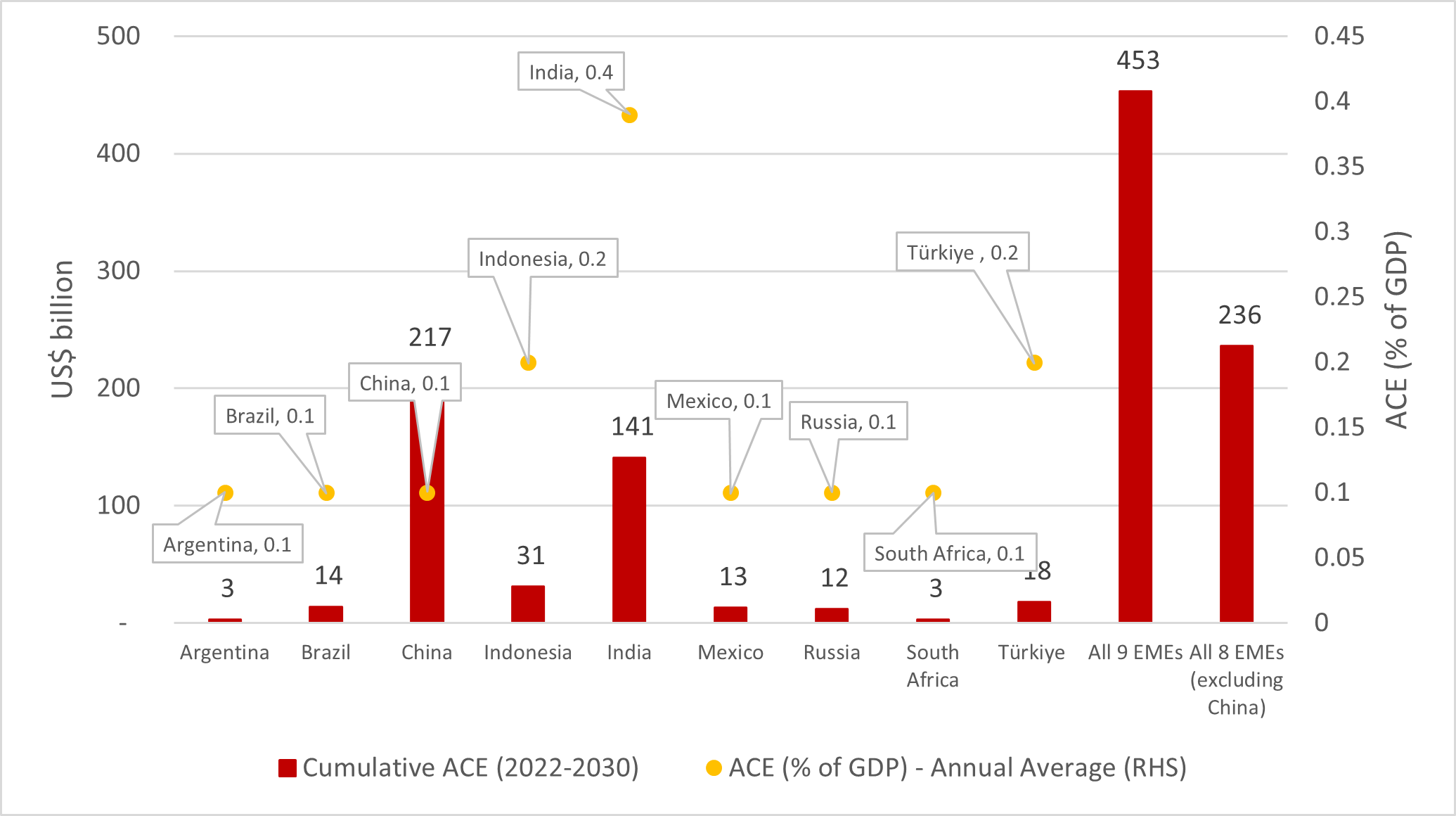

Additional capital expenditure required to mitigate CO2 from the cement sector across the nine EMEs from 2022 to 2030 is estimated at $453 billion or $50 billion on an annual average basis.

Excluding China, additional capex for the cement sector works out to $236 billion between 2022-2030 or $26 billion annually, on an average (Figure 4).

Figure 4 – Country-wise ACE Requirement – Cement Sector (2022-30)

ACE – Additional Capital Expenditure.

Source: Authors’ calculations.

Overall Assessment

Climate finance requirement for all the four sectors for the nine economies has been assessed at $2.2 trillion ($255 billion or 0.6 per cent of GDP annually) up to 2030. The sectoral break-up reveals that the climate finance requirement is driven largely by the steel sector ($1.2 trillion or 52 per cent of total), followed by road transport ($459 billion or 21 per cent), cement ($453 trillion or 20 per cent), and power ($149 billion or 7 per cent) – Table 1.

At a country level, 61 per cent of the climate finance requirement is estimated for China. Excluding China, the climate finance requirement drops sharply to $854 billion ($100 billion or 0.5 per cent of GDP, annually) – Table 1.

Table 1 – Climate Finance Requirement – Four Sectors and Nine Economies#

|

Country |

Power

|

Transport

|

Steel

|

Cement

|

Total Capex | Total Capex

(2022-30)# |

Total Capex as % of GDP (2022-30) |

| 2024-30 | 2023-30 | 2022-30 | 2022-30 | 2022-30 | Annual Average# | ||

|

(1) |

(2) | (3) | (4) | (5) | (6) | (7) |

(8) |

|

1. China |

55 | 336 | 733 | 217 | 1,341 | 155 |

0.7 |

|

2. India* |

57 | 18 | 251 | 141 | 467 | 54 |

1.3 |

|

3. The Russian Federation |

9 | 27 | 73 | 12 | 121 | 14 |

0.7 |

|

4. Brazil |

-3 | 19 | 36 | 14 | 67 | 8 |

0.3 |

| 5. Indonesia | 3 | 38 | 13 | 31 | 85 | 10 |

0.6 |

|

6. Türkiye |

0.6 | 6 | 14 | 18 | 39 | 4 |

0.3 |

| 7. Mexico | 15 | 8 | 8 | 13 | 44 | 5 |

0.3 |

| 8. Argentina | 4 | 4 | 3 | 3 | 14 | 2 |

0.3 |

|

9. South Africa |

8 | 3 | 3 | 3 | 17 | 2 |

0.5 |

| Total (1 to 9) | 149

(6.8) |

459

(20.9) |

1,134

(51.7) |

453

(20.6) |

2,195 | 255 |

0.6 |

| Total (excluding China) | 94

(11) |

123

(14.4) |

401

(47) |

236

(27.6) |

854 | 100 |

0.5 |

ACE – Additional Capital Expenditure.

*Refer to Raj and Mohan (2025).

# Based on the years 2022-30 for the cement and steel sectors, 2023 to 2030 for the road transport sector and 2024-2030 for the power sector.

Note: Figures in parentheses represent the percentage shares in total climate finance requirement.

Source: Authors’ calculations.

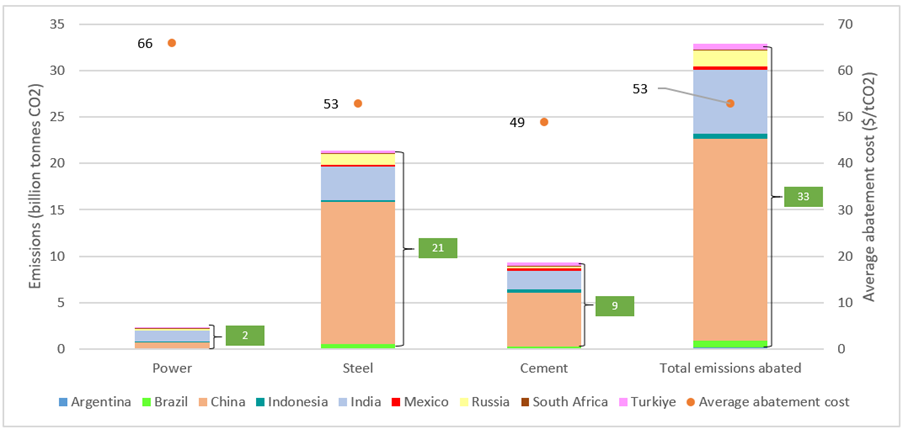

The climate finance estimated for the nine EMEs for the three sectors (power, steel and cement)[3] has the potential to mitigate 33 billion tonnes of CO2. Most of the emission mitigation potential is estimated in the steel sector (65 per cent), followed by cement (29 per cent) and power (6 per cent) – Figure 5.

The average cost to mitigate one tonne of CO2 is estimated at $53 across the three sectors. On a per unit basis, the power sector is estimated to be the most expensive to decarbonise, the average cost of which works out to $66 per tCO2, followed by steel at $53 per tCO2 and cement at $49 per tCO2 (Figure 5).

Figure 5 – Expected Carbon Emissions Mitigation Potential

Note: 1. Average cost is for the nine EMEs.

- Total emissions mitigated do not include emissions mitigated from the road transport sector due to lack of data.

- Carbon emissions mitigation potential in the power sector of Brazil, Mexico and Turkiye could not be worked out due to lack of readily available reliable data.

Source: Authors’ representation.

Conclusion

Climate finance requirements for the nine G20 economies are assessed to be large. China and India alone account for 82 per cent of the climate finance requirement (61 per cent for China and 21 per cent for India). The steel sector requires the largest share of 52 per cent in the estimated climate finance, followed by the road transport cement sectors, requiring almost 21 per cent each. In the road transport sector, it is not the transitioning of ICEVs to EVs, but the development of charging infrastructure which requires large capital expenditure. The power sector requires the least amount of climate finance in most EMEs relative to other sectors included in the study, which is contrary to the common narrative that the transition of the power sector from fossil-based sources of energy to renewable sources requires large capital investments.

FOOTNOTES

[1] Raj, J., and Mohan, R. (2025). “Climate Finance Needs of Nine G20 EMEs: Well Within Reach” (CSEP Working Paper 106). New Delhi: Centre for Social and Economic Progress.

[2] The period covered is 2022-2030 for the steel and cement sectors, 2024-30 for the power sector and 2023-30 for road transport.

[3] CO2 emissions mitigation potential for the road transport sector could not be carried out due to lack of readily available reliable data.

Rakesh Mohan

Janak Raj

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.