The Role of Critical Minerals Stockpiles in India’s Energy and National Security

Reading Time: 7 minutesAs China weaponises its dominance across critical mineral supply chains, countries, including India, are looking for strategies to hedge against geopolitical and market disruptions. Therefore, globally and domestically, there has been a renewed focus on stockpiling of critical minerals in an increasingly uncertain world order.

Critical minerals have emerged as the strategic raw materials of the 21st century. Like coal in the 19th century and oil in the 20th century, critical minerals are emerging as a bedrock of economic, energy, and national security today. As China weaponises its dominance across critical mineral supply chains, countries, including India, are looking for strategies to hedge against geopolitical and market disruptions. Globally and domestically, there has been a renewed focus on stockpiling of critical minerals in an increasingly uncertain world order. Against this backdrop, this blog examines India’s critical mineral landscape, outlines the role of stockpiles as a policy instrument and identifies challenges to their deployment in the Indian context.

India’s import dependence on critical Minerals

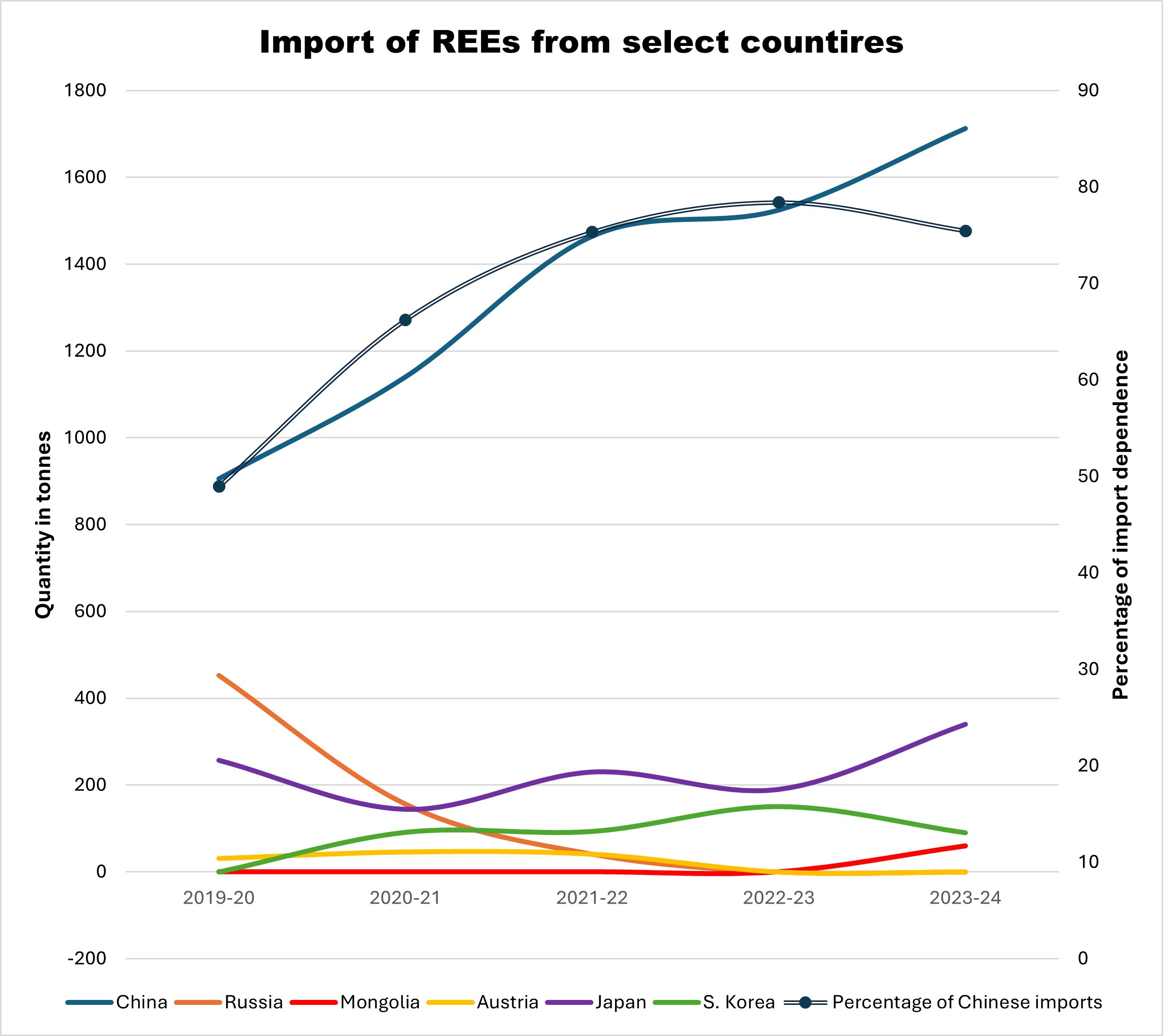

According to the Ministry of Mines India currently remains completely dependent on 10 critical minerals[1]. Particularly, India is making efforts to diversify and reduce dependence on China, which contributes to 80% of the country’s rare earth elements (REE)[2] needs (See Figure 1). There has been a small decline in the share of imports from China due to an increase of imports from Japan and Mongolia, but volumes imported from China have been steadily rising (Figure 1).

Figure 1: Imports of Rare earth elements, scandium, and yttrium (HS code 28053000) and Compounds, inorganic or organic or rare earth metals (HS code 2846) from major import sources between 2019 and 2024. Here, China includes Hong Kong. Source: Lok Sabha unstarred question No. 5253

Weaponisation of critical mineral supply chains

This is not the case only for India. Globally, China dominates the entire critical minerals supply chain of the upstream extraction of raw ores, the midstream processing into refined materials, and the downstream manufacturing of finished products – notably batteries (lithium, cobalt, nickel), wind turbines (neodymium, dysprosium), and solar panels (arsenic, gallium). This implies that the global green energy transition remains reliant on China’s critical minerals and allied industries. Of the 20 energy-related minerals studied by the International Energy Agency (IEA), China was the dominant refiner for 19. China produces 70% of all batteries manufactured globally, which are 20% and 30% cheaper than those produced in North America and Europe, respectively. China also produces 90% of all magnets essential for wind turbines and Electric Vehicle (EV) motors. For the defence sector too, critical minerals are essential components of specialised and generic components used in military aircrafts, surface vessels, submarines, radars, and batteries.

In India most green components are still cost more to manufacture compared to in China. For example, components of the solar PV supply chain are 10% more expensive and wind turbines are 60% costlier to produce in India than China. An exception is the manufacturing of Lithium batteries which is stated to be 5.5% cheaper in India.

Besides their geopolitical volatility, critical minerals also have high price volatility. On average, of the twenty critical minerals deemed as strategic by the IEA, most have a higher price volatility than oil and natural gas

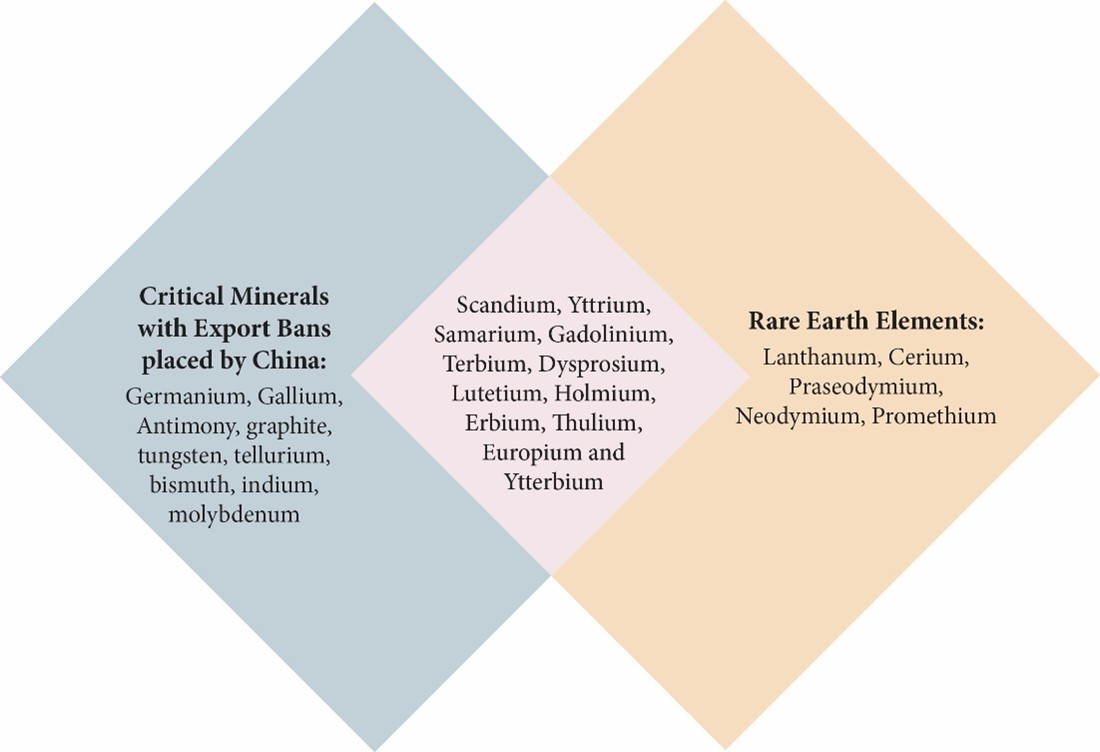

Beginning with restrictions on exports to Japan in 2010, China has used its hegemony of critical minerals to weaponise trade. In retaliation for tariffs imposed by the United States between July 2023 and October 2025, China placed restrictions on several critical minerals and seven REEs (see Figure 2). In 2024, the U.S. Geological Survey estimates the reduction in US Gross Domestic Product (GDP) from simultaneous and complete export bans on Gallium and Germanium up to US$9 billion (0.03% of GDP).

Figure 2: List of critical minerals on which China has or had placed export bans between July 2023 and November 2025 (Blue), and List of REEs (Pink). Note the overlap between REEs and critical minerals with export bans placed on them.

Besides their geopolitical volatility, critical minerals also have high price volatility. On average of the twenty critical minerals deemed as strategic by the IEA, most have a higher price volatility than oil and natural gas (See Figure 2).

It is in this context that critical mineral stockpiles may serve as a tool to buffer against supply disruptions, economic risks, and national security risks. It allows governments to develop long-term supply diversification polices, reduce price volatility, investment risk, and project costs, and may even allow them to negotiate better prices.

What are critical mineral stockpiles?

Simply put, a stockpile is a strategic reserve maintained to ensure an uninterrupted supply of critical minerals. For a stockpile to be viable, certain conditions should ideally be satisfied:

- A downstream industry that can offtake minerals for processing such as smelters and refiners, chemical processing plants, and raw commodity traders.

- A favourable market to purchase minerals at a reasonable cost such as commodity exchanges, long-term offtake agreements, and strategic purchase agreements between governments.

- A market for materials from upstream processing such as EV manufacturers, solar panels and wind turbine manufacturers, the defence sector, and medical equipment manufacturers.

- The nature of the substance to be stockpiled also determines the feasibility of stockpiling (see Table 1).

|

Considerations for critical mineral stockpiling |

||||

| Storage Logistics | Trade and Demand | Compatibility with domestic assets | Processing | Geopolitical considerations |

| Vulnerability to chemical degradation | Frequency with which material is currently traded, shipped, or stockpiled | Availability and composition of geologic resources in the stockpiling country | Degree of additional processing required to synthesise final products | Allied strategic convergence on the use of stockpiles |

| Risk of contamination during storage | Import dependency and supply chain overconcentration | Domestic extraction, processing, and refining capacity of the stockpiling country | Versatility for serving multiple end-use markets and applications.

|

General and sector-specific location of stockpile |

| Vulnerability to physical attacks and cyber-attacks | Price discovery of the commodity

|

– | – | Protection of critical mineral trade routes during conflict |

| Probability and severity of chemical incidents | Potential to support byproduct recovery of other critical minerals | – | – | Requirements for defence stockpiles |

| Form of storage, including volume and density of substance | Relevance for technologies with salient economic and/or national security value | – | – | – |

| Type of ownership of stockpile (Public or private) | – | – | – | |

Table 1: Author’s analysis based on three reports: Taking Inventory of Critical Mineral Stockpiling: A Supply Chain Analysis; A Multilateral Commercial Stockpile for Critical Minerals; and Critical Stocks, Critical Stakes: The Effectiveness of Critical Mineral Stockpiles in Mitigating Supply Risks to Energy, Security and Information.

Historically, stockpiling has been resorted to prior and during periods of high geopolitical tensions. The establishment of modern non-fuel mineral stockpiles can be traced back to the Second World War. In preparation for war, Japan established stockpiles of tin by 1936, Germany established stockpiles of copper by 1939, and the United States (US) established a national mineral stockpile under the Strategic and Critical Materials Stockpiling Act of 1939. The renewed global interest in stockpiling follows a similar pattern.

Historically, stockpiling has been resorted to prior and during periods of high geopolitical tension. The establishment of modern non-fuel mineral stockpiles can be traced back to the Second World War. In preparation for war, Japan established stockpiles of tin by 1936, Germany established stockpiles of copper by 1939, and the United States (US) established a national mineral stockpile under the Strategic and Critical Materials Stockpiling Act of 1939. The renewed global interest in stockpiling follows a similar pattern. Currently, the US, Japan, South Korea, and China maintain known stockpiles of critical minerals. The European Union (EU), the United Kingdom (UK), Italy, France, and India are among the countries that have publicly expressed intent to establish them. The next blog in this series will explore the stockpiling policies of other countries in depth, while drawing out lessons for India’s own strategy.

In the context of energy security, similar to critical minerals, oil has also been the subject of stockpiling. In 1973, following the Organization of the Petroleum Exporting Countries (OPEC) oil export embargo, the US established the Strategic Petroleum Reserve. The IEA, since its creation in 1974, also requires member states to maintain stockpiles of crude oil and/or product reserves equivalent to 90 days of the previous year’s net imports.

In India, strategic oil reserves are maintained through a special purpose vehicle – the Indian Strategic Petroleum Reserve Limited (ISPRL). The ISPRL is a wholly owned subsidiary of the Oil Industry Development Board (OIDB), which is established under section 3 of the Oil Industry (Development) Act, 1974. The Indian government currently maintains 9.5 days’ worth of strategic oil reserves amounting to 5.53 Million Metric Tonnes (MMT) through the ISPRL, with an additional 6.5 MMT approved for construction. Separately, Oil Marketing Companies (OMC) in India maintain crude oil and petroleum products that will last for around two months.

India’s critical mineral stockpiling ambitions

India has sought to secure critical minerals through the National Critical Mineral Mission (NCMM). To this extent, it has allocated US$3.94 billion in support of the NCMM over seven years between 2024 and 2031 with the twin objectives of securing India’s critical mineral supplies and strengthening value chains. The mission places importance on the role to be played by Public Sector Undertakings (PSUs), namely through Khanij Bidesh India Ltd. (KABIL). The National Mineral Development Corporation, National Thermal Power Corporation Mining Ltd., Indian Rare Earth Limited, and Oil and National Gas Corporation Videsh are among others who are also expected to invest in critical minerals. It is anticipated that US$2.07 billion will be invested by PSUs.

The government has allocated US$57.5 million to establish critical mineral stockpiles. Under the NCMM, essential critical minerals will be identified for stockpiling, along with mechanisms to ensure their timely release through coordination between government and industry. The policy also proposes a partnership between central PSUs and private companies to institutionalise a National Critical Mineral Stockpile Programme. The programme aims to secure key strategic minerals, protect against supply disruptions, and support domestic industry needs. Stockpiles will be created for at least five critical minerals, with an initial focus on REE stockpiles that would last for two months.

Depending on how stockpiling is planned, it has the potential to either increase or decrease the prices of critical minerals. When stockpiles are released, an increased supply brings prices down by meeting demand. However, when minerals are procured to fill stockpiles, that surge in demand can raise prices – which may even delay the clean energy transition.

What factors should India consider while creating mineral stockpiles?

Stockpiles are generally considered a cost-effective way to mitigate geopolitical risks and supply shortages by ensuring the availability of critical minerals to match their demand. However, the effectiveness of critical mineral stockpiles varies depending on the purpose, the implementation, investments in midstream and downstream supply chains, and the existence of non-transparent stockpiles [3]. States also need to periodically weigh the risk of financial losses from geopolitical supply disruptions against the cost of storage.

Depending on how stockpiling is planned, it has the potential to either increase or decrease the prices of critical minerals. When stockpiles are released, an increased supply brings prices down by meeting demand. However, when minerals are procured to fill stockpiles, that surge in demand can raise prices – which may even delay the clean energy transition.

The creation of a stockpile and the development of a stockpiling policy must be approached with caution. For India, stockpiling can be one pillar of a broader strategy to build a stable and secure critical minerals ecosystem. Globally, if stockpiling is done right, it can lay the foundations of a world order resilient against economic and political coercion. Without a clear strategy however, stockpiles risk becoming costly symbols of security rather than instruments of it.

FOOTNOTES

[1] These are lithium, cobalt, nickel, vanadium, niobium, germanium, rhenium, beryllium, tantalum, and strontium

[2] Rare Earth Elements are a group of 17 metallic elements that are abundant, found in low concentrations and difficult to process (Figure 2). They may be classified as light rare earth elements (LREEs) or heavy rare earth elements (HREEs) based on their atomic number. These elements have unique properties that make them are essential materials in a broad range of technologies including energy security, defense, medicine, and manufacturing among others.

[3] Stockpiles whose size, composition, location, or release strategy remain undisclosed—such as those maintained by China

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.