What Differentiates Successful GVCs: Lessons for India

Reading Time: 4 minutesGlobal trade can be an important source of economic transformation for an emerging economy like India, through increased employment[1]. However, India has not been able to use this important tool to its potential, and, is facing challenges in sustaining the export journey that it started after its economic reforms in 1991. While India’s share in global exports increased at an impressive rate since 1991, the share has stagnated since 2011. Its share in global exports was 1.8 per cent in 2011, and has increased by merely 0.2 per cent, to reach a 2 per cent share in global exports, in 2022 (WITS, 2022).

Lack of Export Orientation

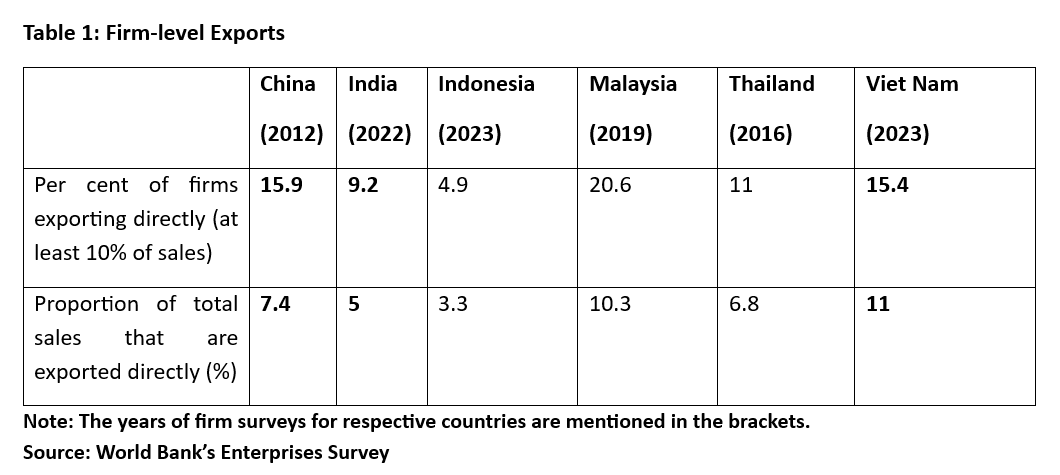

The export activities of the manufacturing firms in India can help to understand this national trend. In this regard, World Bank’s Enterprise survey[2] brings out the low weightage that Indian manufacturers give to the foreign market and demand, with only 9.2 per cent of Indian firms exporting (at least 10 per cent) of their sales directly, in comparison to 15.4 and 15.9 per cent for Vietnam and China (Table 1).

This survey-based information can be corroborated with the firms’ financial data derived from the CMIE Prowess database, according to which, out of the total manufacturing firms listed (47372), only 17 per cent of firms are exporting (8106), dominated by petroleum, gems and jewelry and automobile firms.

Only 9.2 per cent of Indian firms exporting (at least 10 per cent) of their sales directly.

Importing for Higher Exports

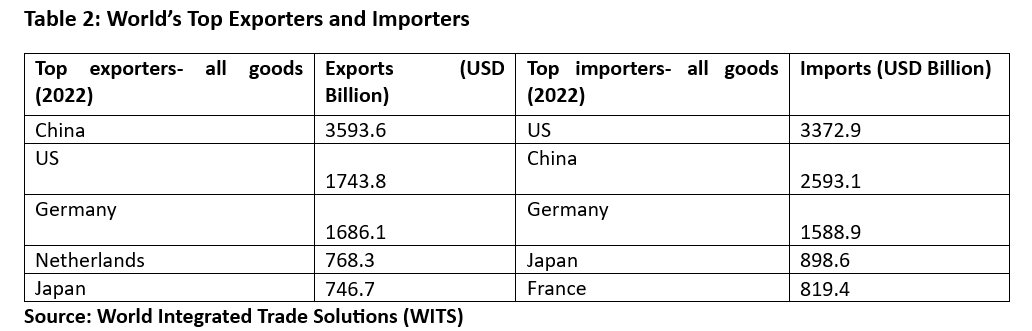

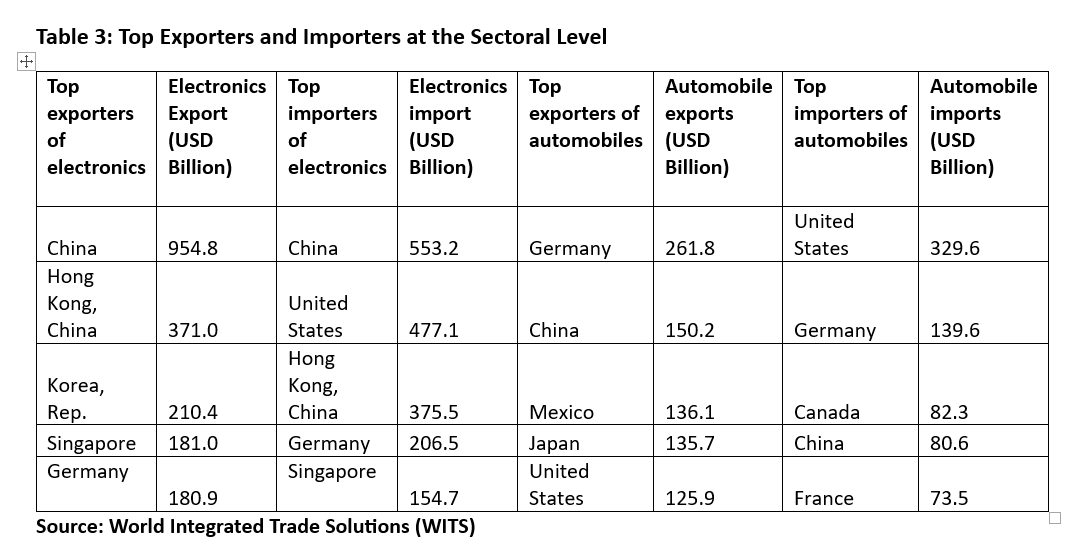

Given this trend of low export-oriented manufacturing in India, it is important to understand the wider picture of the export dynamics. An important driver of a country’s exports is the import of key inputs like raw materials, capital goods, and intermediate goods, which is determined by the import tariffs a country places on these imports. This explains why countries like the US, China, and Germany, the global export leaders, are also top importing nations (Table 2). This relationship can also be observed at the product level, indicated by the commonality between top exporting and importing countries for the electronics and automobile sectors (Table 3). Even Vietnam, an emerging electronics hub, appears to be among the top exporters and importers of electronics items. These trends indicate the integration of these countries in the Global Value Chains (GVC) of respective products, wherein the countries import requisite intermediate goods, to add value and export the finished goods.

An important driver of a country’s exports is the import of key inputs like raw materials, capital goods, and intermediate goods.

In the case of India, GVC integration evidence is missing for important GVC items like automobiles and electronics, as India tries to be more self-reliant in sourcing production inputs, and hence has to bear the competitiveness cost, reflected in its low exports.

World Bank’s enterprises’ survey findings also substantiate India’s low GVC integration as only 6 per cent of firms reported using inputs of foreign origin for their production, which is the lowest among other competing countries, like China and Vietnam with 15 and 38 per cent respectively.

Firm-level Data Substantiates India’s Low GVC Integration

To understand the nuances of GVC integration, we resort to CMIE prowess database for details on the imported and domestic raw materials. Out of the 8106 exporting firms, there are around 3175 firms that report to be using raw materials, either imported or domestic. Out of these, 2608 firms use a combination of both, imported and domestic raw materials, and 14 firms rely only on imported raw materials and belong to sectors like autocomponents, household appliances, gems, sugar, and X-ray films. Of the 2608 firms that use domestic and imported raw materials, only 585 firms have a relatively greater dependence on imported raw materials, indicating weaker GVC integration from the input sourcing end.

Most of the imported or domestic raw materials go into production for domestic consumption.

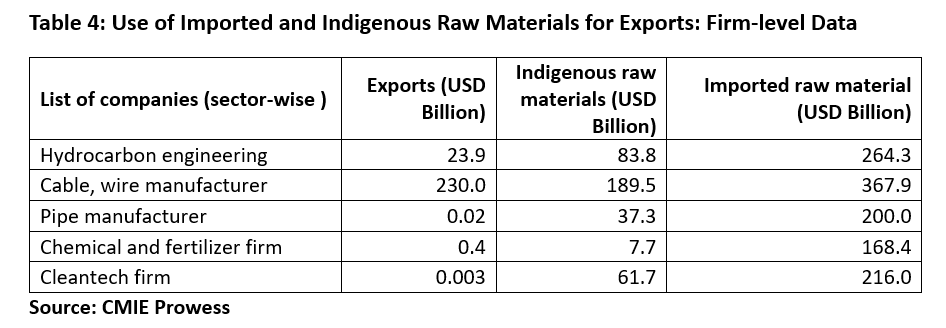

An interesting insight from the analysis is that most of the exporting firms (except a few oil companies), that rely on the combination of domestic and imported raw materials, export only a proportion of the value of raw materials (Table 4 provides firm-specific trade data). [3] This implies that most of the imported or domestic raw materials go into production for domestic consumption.

The analysis revealed India’s low GVC integration, driven by both import and export ends. The key implication that can be derived is that if India wants to use GVCs to strengthen its export flows, it will have to liberalise the entry of imported goods, specifically inputs/intermediate goods, by lowering the import tariffs. Free Trade Agreements can be an important policy tool in this regard, wherein India can bilaterally engage with important economies to achieve mutually beneficial outcomes for respective economies.

References

The World Bank. (2022). World Integrated Trade Solution. Retrieved from https://wits.worldbank.org/

FOOTNOTES

[1] Jobs gap rate, which is defined as the number of persons without employment who are interested in finding a job, was 8.2 per cent for the high-income countries in 2023, as compared to higher values of 20.5 and 11 per cent for the lower income countries and lower middle-income countries, respectively (ILO, 2024). According to the World Bank, every 1 per cent increase in employment leads to a 0.6 per cent increase in GDP growth.

[2] The World Bank Enterprise Survey (WBES) is a firm-level survey of a representative sample of an economy's private sector. The surveys cover a broad range of topics related to the business environment including access to finance, corruption, infrastructure, competition, and performance.

[3] The company name is not mentioned in the table, only the broad sector to which the company belongs is provided.

Prerna Prabhakar

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.