India’s fiscal architecture: Lessons from the world and a way forward

Reading Time: 13 minutesEditor's Note

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development. All content reflects the personal views of the authors. CSEP does not hold an institutional view on any subject. Editor’s Note: An earlier version of this Discussion Note was published as a two-part series in Mint.

DOWNLOADS

Abstract

As the COVID-19 pandemic brings various challenges to public finance, the magnitude of fiscal costs that need to be absorbed has highlighted and exposed the weak fiscal architecture in many countries. These challenges highlight the need for clarity in the three pillars of fiscal architecture: fiscal rules, public financial management (PFM) processes, and fiscal institutions that widen accountability over the fiscal rules. In this discussion note, we look at how countries are strengthening their fiscal systems by putting in place new and innovative coordination mechanisms. We argue that India needs to benchmark its fiscal architecture to 21st century international standards and learn from global best practices. We discuss the fiscal rules, the PFM framework, and fiscal institutions in India and observe that India needs to improve the quality and efficiency of public spending and financial management across all levels of government. We also suggest the use of information technology to make PFM more transparent, reliable, and real-time.

The COVID-19 crisis has brought new risks to public finance given its extent, the inability of subnational governments to absorb the fiscal costs, and the asymmetric regional impact of the crisis. These risks exceed those experienced in the 2008 global financial crisis. The sheer magnitude of fiscal support has highlighted and exposed the weak fiscal architecture in many countries.

A key lesson from history is that an accountable and efficient PFM system becomes more critical during crises. Without improving the adaptability and responsiveness of fiscal management, the costs to the economy from misdirected resources and inefficient resource use will compound the effects of the COVID-19 crisis.

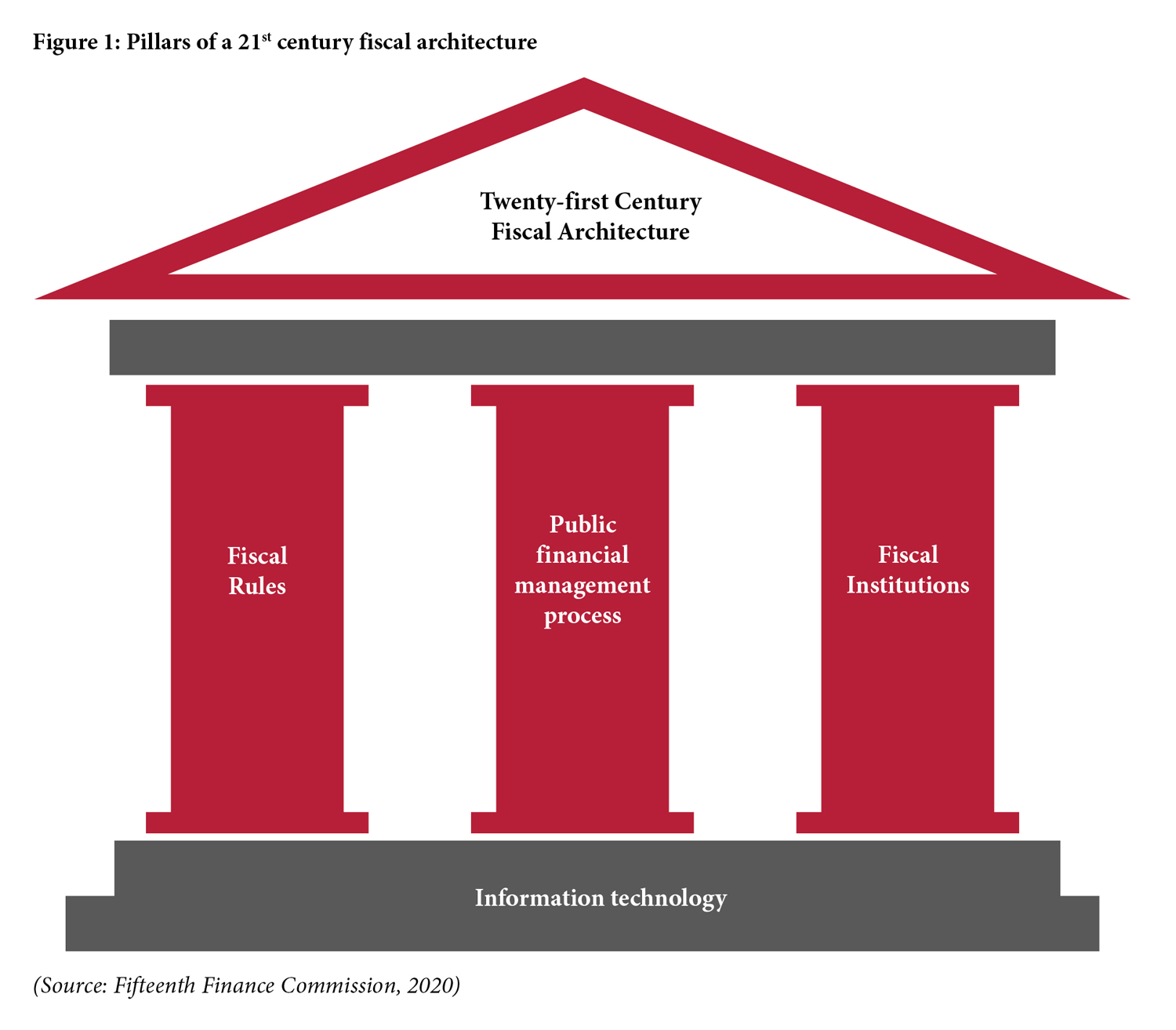

The challenges currently being faced highlight the need for greater clarity in the three pillars of the fiscal architecture, viz. fiscal rules, PFM processes, and fiscal institutions. While many countries do not have this fiscal architecture in its entirety, a growing number are quickly putting in place new and innovative coordination mechanisms, involving governance and fiscal tools, to strengthen these pillars. Over the past decade, since the global financial crisis, international experience in fiscal rules, PFM processes, and institutional reforms has been building (International Monetary Fund, 2014). The evidence from these experiences confirms the effectiveness of stronger budgetary institutions at key stages of the fiscal adjustment process in achieving better fiscal outcomes. The fiscal reforms broadly fall under the following three heads:

Understanding the fiscal challenge: Extending the coverage of fiscal reporting, forecasting and risk assessment to the general government and, eventually, to the public sector, with independent fiscal agencies reviewing fiscal forecasts.

Developing a credible fiscal adjustment plan: Establishing fiscal rules and performance budgeting systems that review spending allocations and a medium-term budget framework that includes the fiscal impact of policies.

Implementing the fiscal adjustment plan by ensuring all major fiscal decisions are part of the ‘unity’ of the budget process by eliminating extra-budgetary funds, reducing earmarked expenditures and tightening rules around supplementary budgets.

Many countries have established overarching legal frameworks to cover these fiscal objectives and institutional reforms, including defining the roles and responsibilities of key stakeholders, especially the states and local governments. These legal frameworks have covered the critical interplay between the design of fiscal rules, PFM systems, and the establishment of fiscal councils. The central lesson from international experience is that clear and consistent PFM systems are a pre-requisite for the effective implementation of fiscal rules and fiscal councils.

India’s twenty-first-century fiscal architecture should accordingly be built on the three aforesaid mutually reinforcing pillars (Figure 1):

- fiscal rules across all levels of government which set the institutional and budgetary framework for fiscal sustainability.

- a PFM system that provides complete, consistent, reliable, and timely reporting of the fiscal indicators that are part of the first pillar; and

- an independent assessment mechanism so as to provide assurance and advice on the working of the other two pillars.

The use of information technology and computing capacities that India has developed in last few decades already provide a strong backbone to support such a fiscal architecture.

With respect to strengthening budget institutions and management practices and their accountability, many advanced and emerging market countries have set fiscal rules (including at subnational levels) to retain the confidence and trust of financial markets. The fiscal rules have evolved over time into a broader ‘second-generation fiscal-framework’, trying to balance credibility with flexibility. However, they are now being tested during the pandemic, prompting a raft of reforms, including the introduction of new rules, revamping of escape clauses, enhancement of monitoring and enforcement mechanisms, and reconsideration of procedures and practices to ensure fiscal sustainability. Many economies have now also adopted “emergency bills” to suspend their fiscal rules and enhance flexibility in sub-national regulatory frameworks as they address the fiscal challenges from the pandemic (Fifteenth Finance Commission, 2020).

International experience indicates that well-designed and well-implemented fiscal rules have helped contain the ‘deficit bias’, strengthen market credibility of the commitment to fiscal sustainability, and in enabling countercyclical fiscal management. By increasing the predictability of fiscal policy, they have helped lower output volatility and raised sustainable growth.

However, the challenge to achieve these outcomes is at least three-fold: to ensure that they are well-designed, that the PFM systems and institutions allow them to be well-monitored and implemented, and deviations from the fiscal rules allow the return to the rules in a time-bound manner. Unless these challenges can be met, fiscal rules can quickly lose their relevance and credibility. A crucial element is subjecting the process to external scrutiny and parliamentary approval, which will balance flexibility with credibility. Independent fiscal councils help in overcoming these challenges.

The aforesaid second generation fiscal-framework that has developed across countries in the past decade can be characterised by three broad features:

- Countries are now increasingly adopting more than one fiscal rule to better balance credibility (the need to create a fiscal anchor) with flexibility (the need to respond to economic shocks). One challenge with multiple rules, however, is that they can sometimes be internally inconsistent and complex to monitor, verify, and communicate.

- They typically rely on ‘escape clauses’ to create flexibility. To ensure that fiscal rules have the flexibility to respond to economic shocks, advanced economies rely on cyclically-adjusted or structural deficits. Computing the state of the business cycle and the quantum of output gaps, however, is challenging in emerging markets. Emerging markets, therefore, rely on escape clauses that allow deviations from fiscal rules in the event of exogenous shocks that are outside the policymaker’s control.

- Countries often adopt ‘automatic correction mechanisms’ which are encoded in the legislation and specify in advance how deviations from the rule will be handled. This is now a requirement for European Union countries that have signed the ‘Fiscal Compact’. An ex-ante auto correction mechanism is a visible signal of policymakers’ commitment to return to fiscal rules in a time-bound manner.

It should also be noted that countries with successful fiscal rules had also implemented overarching PFM laws to ensure that these systems were sufficiently developed to support the fiscal rules. International evidence is clear that countries with weak PFM systems were unable to monitor and effectively control fiscal targets and rules.

India was one of the early adopters of fiscal rules among emerging market countries. Through a number of amendments, the Union has updated the Fiscal Responsibility and Budget Management (FRBM) Act, adopted multiple fiscal indicators as target indicators, and has tried to bring India into the second generation of fiscal rules. As such, the Union as well as all States have their fiscal rules and numerical targets in place.

However, there are gaps and inconsistencies in these rules. For instance, the fiscal deficit defined in the FRBM Act (as the balance of operations incurring into the Consolidated Fund of India) falls short of the newly legislated debt ceiling that covers a broader definition of accounts and implementing agencies that deliver public services on behalf of the government. In practice, this has led to the fiscal rules being effectively circumvented, in particular by the use of off-budget fiscal operations, inconsistent budget classification and accounting standards, and improper use of the public accounts for budgetary purposes. Effectively, this is because the underlying PFM system meets only a fraction of best practice standards.

In short, having a fiscal rule raises the bar on the needed strength of the underlying PFM processes and fiscal institutions.

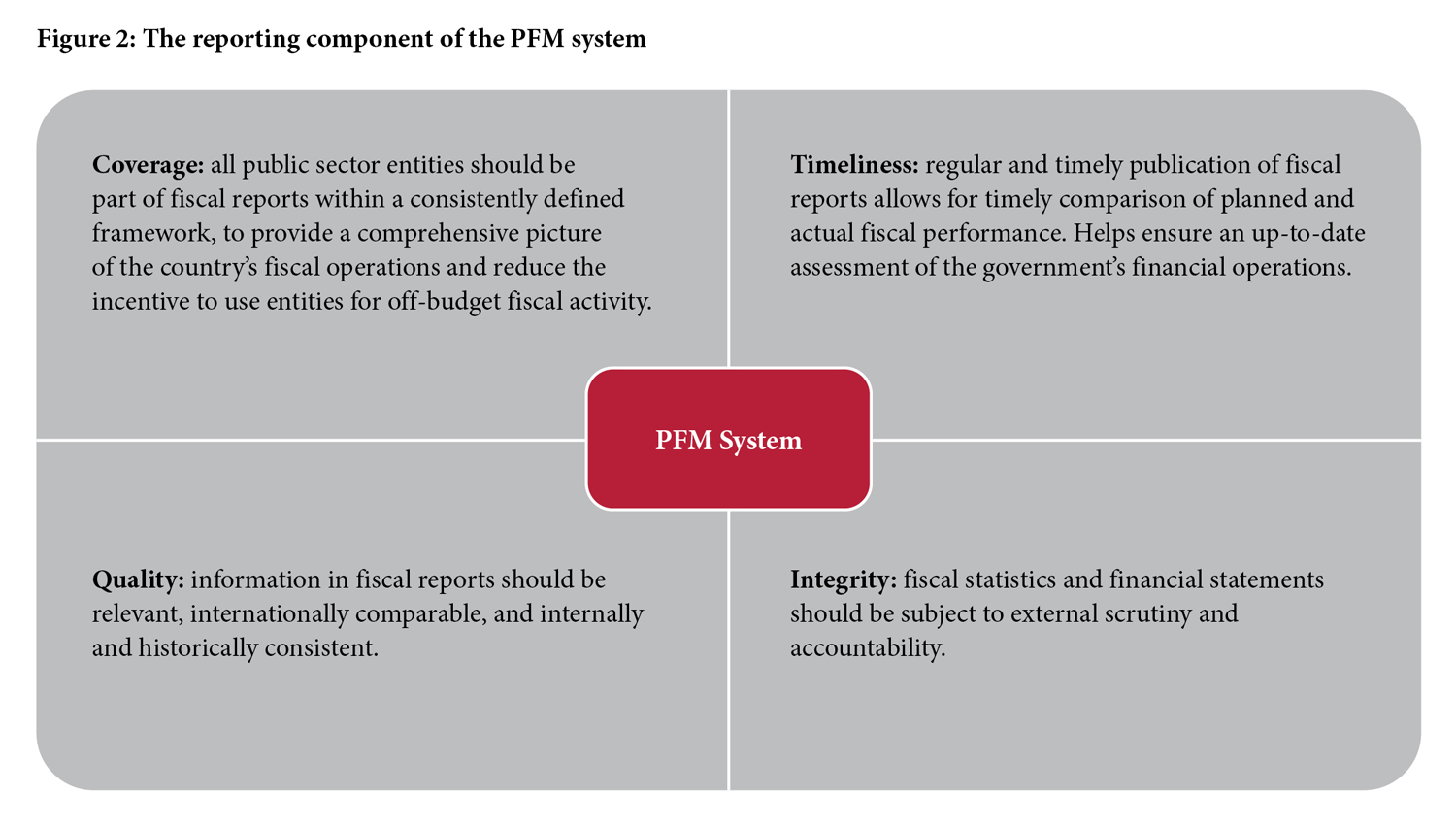

PFM refers to the set of laws, rules, systems, and processes used to mobilise revenue and allocate and account for the use of public funds. It is well-recognised that a strong PFM system is an essential part of the institutional framework for effective public service delivery—both are closely associated with poverty reduction and economic growth. The first step towards better fiscal management is improving the coverage, timeliness, quality and integrity of fiscal reporting (Figure 2).

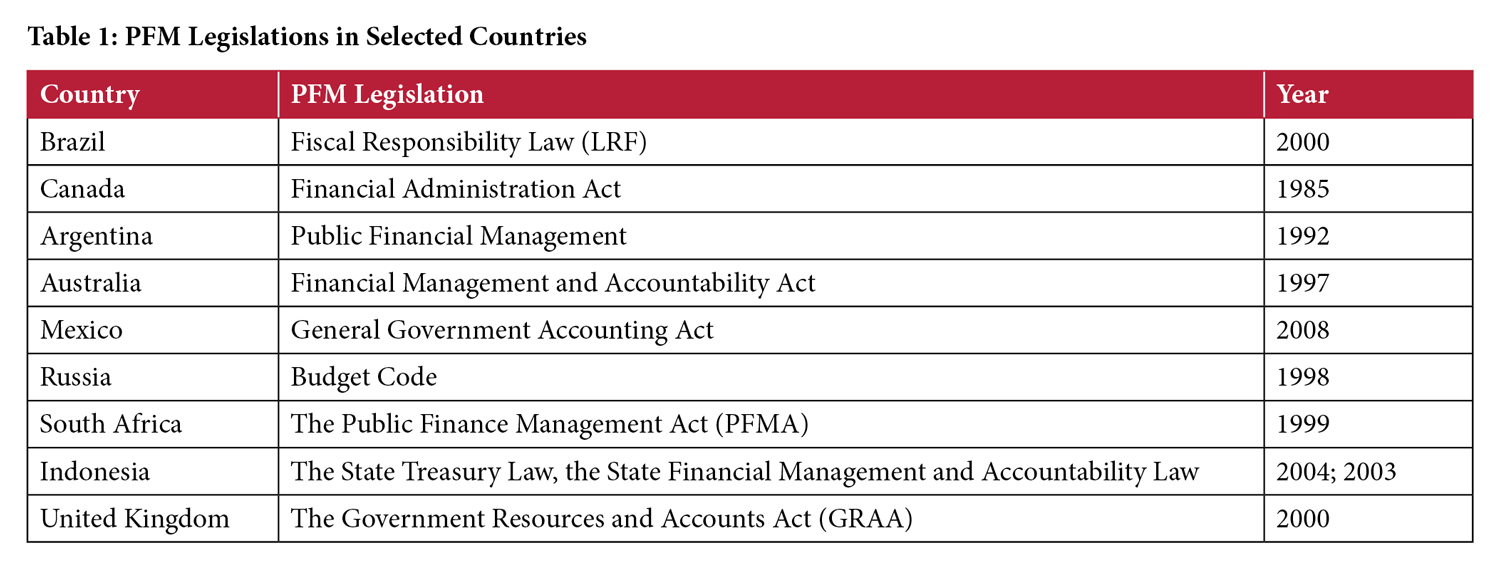

Towards this end, most advanced and large emerging market countries have, in the past decade, established legal frameworks for PFM that set out the budget, reporting, accounting, and audit processes, and define the roles and responsibilities of key stakeholders (Table 1). These laws have aimed at aligning fiscal policy to resource allocations and have paved the way for implementing the standards in the fiscal rules in a credible manner. For instance, New Zealand sets a high standard for transparency and the lucidity of its budget documents. Among middle-income countries, South Africa’s budget documentation is highly transparent and accessible, with extensive debt reporting and clear and concise fiscal risks reports.

India’s fiscal architecture, therefore, needs to address these reforms and bring its PFM processes up to international standards and ensure that public and private resources are efficiently deployed for sustainable growth. Equally importantly, international experience conveys that PFM best practices are critical for the effective implementation of fiscal rules.

India’s current PFM processes are defined at the highest level, i.e. in the Constitution itself. However, many policies and operational details have evolved over time through a plethora of practices. Compliance with best practices envisaged in the fiscal rules remains challenging as a majority of the practices affecting budget formulation, execution, and reporting are still without legislative strength—being governed instead by a multiplicity of constitutional provisions, executive rules, orders, and manuals. There is also lack of consistency in practices across the levels of government, resulting in marked differences in the way PFM systems at the Union and States have emerged.

India needs to clearly define its PFM framework, strengthen budgetary institutions at key stages of the fiscal process, prescribe the accounting framework and precise definitions for target fiscal indicators, and ensure consistency of fiscal rules across all levels of government. The lack of progress in these areas continues to distort the alignment of the budget and expenditures with government policy priorities, hinders effective expenditure control, raises the public costs of inefficiency on fiscal management, and creates opportunities for creative accounting and biased forecasts; in this regard, it helps that progress is being made in bringing the food subsidy more fully on-budget in the recent budget for 2021-22.

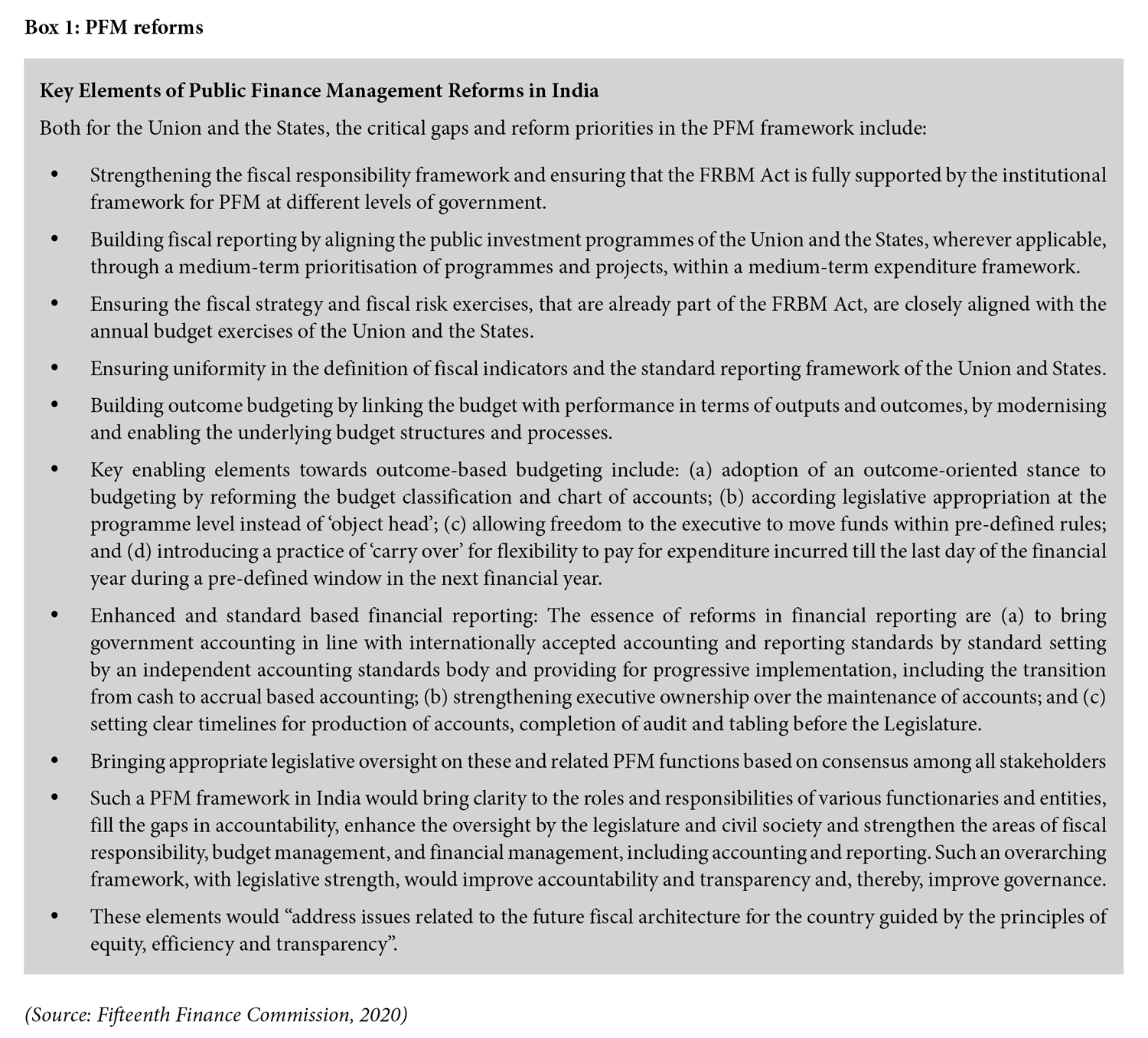

Looking ahead, PFM reforms at the sub-national level should be consistent with reforms at the Union Government level, especially in terms of a clear PFM framework, ensuring consistent and well-defined targets and accounting standards, timely and reliable reporting of subnational fiscal operations, and strengthening automatic correction mechanisms and sanctions for non-compliance. States should seek to define subnational debt targets that are consistent with general government debt reduction targets. Box 1 elaborates on this:

India has tried, over time, to make individual and incremental reforms to successive parts of the PFM system. These have generally been stand-alone in nature, focusing on particular (and dispersed) dimensions of PFM, that have been difficult to integrate and sustain. A comprehensive legal PFM framework as highlighted by the Fifteenth Finance Commission, and as adopted by many countries in the world, may be the best way forward for India.

Globally, there has been a sharp rise in the number of independent fiscal institutions or councils set up to enhance the credibility of the fiscal rules, help impose hard budget constraints on the public sector, and monitor the long-term sustainability of government fiscal stances. A fiscal council can be thought of as an independent, non-partisan agency—set up either through a statutory or executive mandate, to publicly assess the government’s fiscal performance against its stated objectives. Fiscal rules and fiscal councils have developed as complements. Good councils learn how to better interpret fiscal rules and to suggest improvements. Well-designed rules make the task of councils easier to perform and less controversial than poorly designed or weak rules. Thus, effective rules and functioning councils are expected to reinforce each other.

Over the past decade, there has been a global trend to set up independent public bodies that provide non-partisan oversight and analysis of fiscal policy and performance to inform public decision-making. Independent fiscal institutions are now a common component of fiscal frameworks in most advanced economies, and the overall number of countries with such fiscal councils has more than tripled over the past decade. While these fiscal institutions take many forms, their tasks typically include preparing or assessing macroeconomic or fiscal forecasts, monitoring compliance with fiscal rules, budgetary analysis, long-term fiscal sustainability analysis and, for some, policy costing. There are several examples of fiscal councils tasked with a role in national and subnational fiscal coordination as well. Empirical evidence suggests that fiscal councils can improve forecast accuracy and foster compliance with fiscal rules (Beetsma et al, 2019).

A variety of institutional models exist for the manner in which fiscal councils are set up and their placement within the government system:

- Stand-alone institutions that are typically set up as part of fiscal responsibilities laws, such as those in Germany, Hungary, Ireland, Portugal, and Romania.

- Councils under the legislative branch, which include budget offices within the legislature, typically established in presidential political systems like in the United States of America and Mexico. Other countries that have adopted this approach include Australia, Canada, Italy, Georgia, Kenya, and South Africa.

- Councils that come under the executive branch, such as those in Belgium, Croatia, Denmark, Japan, and the United Kingdom.

- Councils paired with other financial institutions, such as those in France and Finland.

Effective fiscal councils should have (a) legal and operational independence; (b) strong media presence; and (c) chair and board members with non-partisan affiliations. Key safeguards for operational independence include secured funding sources, access to information on a timely basis, and ability to manage their own staff. Effective fiscal councils establish contact with the media in line with the budget cycle and at the time their reports are published.

Experience suggests that such fiscal institutions have contributed to assessing and monitoring fiscal policy, helped in effective implementation of fiscal rules, and strengthened fiscal performance. Independent scrutiny makes for better compliance with fiscal rules through their influence on the accuracy of budget forecasts.

Several experts’ bodies and committees have recommended setting up an independent fiscal council in India. Most recently, the FRBM Review Committee as well as previous Finance Commissions have recommended establishing such an institution with suggested functions and structure. Once India emerges from the COVID-19-induced crisis, this would be a key step towards improving the credibility of fiscal management.

The mandate of a fiscal council could be broadened to cover not only the production of macroeconomic and fiscal forecasts to inform the budget, but also to advise on setting and recalibrating fiscal targets and rules at national and sub-national levels, as well as monitoring compliance with such targets and rules. The fiscal council can also work towards improving the quality of fiscal statistics at all levels of government.

The fiscal impact of the COVID-19 crisis has put a premium on strengthening the institutional anchor for sustainable public finances. As the crisis continues to cast a long shadow over public finances of many countries, the need to restore fiscal credibility encourages further reforms of fiscal frameworks. In many countries, efforts are being made to address pre-existing weaknesses and bottlenecks in PFM systems and set up improved reporting mechanisms to ensure financial transparency and accountability, which would help in reallocating funds to the frontlines of the COVID-19 crisis. It is crucial to ensure full transparency and good governance in all fiscal measures, especially given their size, exceptional nature, and speed of deployment.

For India to achieve its full potential for economic growth and development, it needs to improve the quality and efficiency of public spending and financial management across all levels of government. India should work towards benchmarking its fiscal architecture to its peers, learning from the experiences of other federal countries, and adopting best practices. In this discussion note, we have identified some of the steps needed to bring India’s fiscal architecture to 21stcentury international standards.

The reforms we have outlined may take several years to be implemented fully. Regular monitoring will help decision-makers keep track of reforms over time. It will also help track progress and performance across States. Hence, there is need for an institutional mechanism driving budgetary and PFM reforms in a coordinated, transparent and inclusive way across levels of government to deliver consistency, transparency and accountability. Information technology can play a crucial role in making PFM processes more transparent, reliable and real-time by integrating and digitalising the entire PFM value chain. Many States have already started digitalising their budgetary, treasury and accounting processes through Integrated Financial Management Systems (IFMS). However, it requires further integration and comprehensive coverage to really unlock its full potential.

Towards this end, as recommended by the Fifteenth Finance Commission (2020), the Ministry of Finance should launch the process of stakeholder consultations soon and prepare a time-bound plan for the implementation of comprehensive PFM reforms at all levels of government. To bring States into these discussions, such a process could also become part of the discussion agenda of existing forums of Union-State consultations, such as the Inter-State Council or the governing council of NITI Aayog.

Bahl, R. & Bird, R.M. (2018). Fiscal decentralisation and local finance in developing countries. United Kingdom: Edward Elgar Publishing

Bahl, R. (2012). Metropolitan city finances in India: Options for a new fiscal architecture (ICEPP Working Paper No. 69). Atlanta, United States of America: Andrew Young School of Policy Studies, Georgia State University

Beetsma, R., Debrun, X., Fang, X., Kim, Y., Lledo, V., Mbaye, S., Yoon, S., & Zhang, X. (2019). Independent Fiscal Institutions: Recent Trends and Performance. European Journal of Political Economy, 57, 53-69. https://doi.org/10.1016/j.ejpoleco.2018.07.004

Fifteenth Finance Commission. (2020). Finance Commission in COVID Times: Report for 2021-26

Forman, K., Dougherty, S., & Blöchliger, H. (2020). Synthesising good practices in fiscal federalism: Key recommendations from 15 years of country surveys. OECD Economic Policy Papers, 28. https://doi.org/10.1787/89cd0319-en

International Monetary Fund. (2014). Budget institutions in G-20 countries: An update. IMF Policy Paper. Retrieved from https://www.imf.org/en/Publications/Policy-Papers/Issues/2016/12/31/Budget-Institutions-in-G-20-Countries-An-Update-PP4867

International Monetary Fund. (n.d). Government Finance Statistics (GFS). Retrieved from https://data.imf.org/?sk=a0867067-d23c-4ebc-ad23-d3b015045405

Rao, G. (2017). The effect of intergovernmental transfers on public services in India (Working Paper No. 218). New Delhi, India: National Institute of Public Finance and Policy. Retrieved from https://www.nipfp.org.in/media/medialibrary/2017/12/WP_2017_218.pdf

Sarma, A. & Chakravarty, D. (2018). Integrating the third tier government in the Indian federal system. Singapore: Palgrave Macmillan

Slack, E. & Bird, R.M. (2015). How to reform the property tax: Lessons from around the world. (IMFG Papers on Municipal Finance and Governance No. 21). Toronto, Canada: Munk School of Global Affairs, University of Toronto. Retrieved from https://munkschool.utoronto.ca/imfg/uploads/325/1689_imfg_no.21_online_final.pdf

Von Trapp, L., Lienert, I., & Wehner, J. (2016). Principles for independent fiscal institutions and case studies. OECD Journal on Budgeting, 15(2), 9-24 https://doi.org/10.1787/budget-15-5jm2795tv625

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.