IMF Quota reforms and global economic governance: What does the future hold?

Reading Time: 31 minutesDOWNLOADS

This paper examines the issues related to the potential of quota reforms in the IMF in the future. It reviews the troubled history of quota reforms in the recent past. The 14th Quota Review, approved in 2010 in the wake of the North Atlantic financial crisis, was finally implemented in 2016; the 15th review, which should have been completed in 2015, was concluded with no change in 2019; and the 16th review is not slated to be completed until 2023. Meanwhile, very significant changes have taken place in the relative economic weights of advanced economies with respect to emerging market and developing economies, and which will continue in the same direction in the foreseeable future. Moreover, more recently, the very significant increase in geopolitical tensions between the United States, China and Russia on the one hand, and India and China on the other, suggests that achievement of consensus in the coming years on quota reforms will become that much more difficult. The paper documents the increasing imbalances between economic weights of dynamic economies and advanced economies and their quota shares and voice in the governance of the IMF. It raises the question of whether the current trend of decision-making will gradually make the IMF increasingly unrepresentative, and hence lacking in effectiveness in the future as the key institution devoted to providing a global safety net. It suggests that the way forward for the institution will involve greater cooperation between the United States and China, as the size of the Chinese economy approaches and surpasses that of the United States.

The world is on the cusp of an epochal change in global economic power, not seen during the past 200 ̶ 250 years since the start of the industrial revolution. What is remarkable is the pace of change that has taken place since the turn of the century.

After more than 200 years, the centre of gravity of the global economy is shifting back towards Asia from the North Atlantic. Yet little evidence of this change is reflected in the framework of global economic governance, where we see hardly any substantive change in the governance structures of the international financial institutions, such as the International Monetary Fund and the World Bank. The current system still reflects the economic power structure as it emerged after World War II, but which was updated through inclusion of Japan and Germany as they recovered from the ravages of that War. The international financial organisations remain dominated by the advanced economies (AEs) particularly the G7,[3] even as they have been losing their relative economic share, particularly over the last couple of decades.

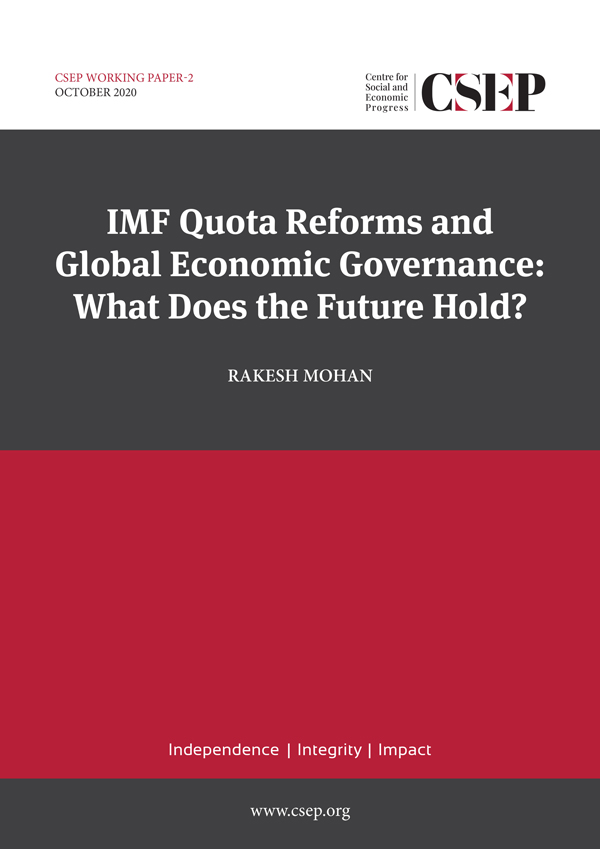

The global economic structure was broadly stable from 1945 until the turn of the millennium. The advanced economies’ (AEs) share in global GDP was around 60 percent (on PPP basis) through that period though there were changes in relative weights among the advanced economies themselves, particularly related to the postwar rise of Germany and Japan. Change has gathered pace since 2000, with economic weight shifting from the North Atlantic to Asia. This is expected to accelerate further over the next couple of decades. So, changes in global economic governance will have to be more substantive than the current incremental change envisaged.

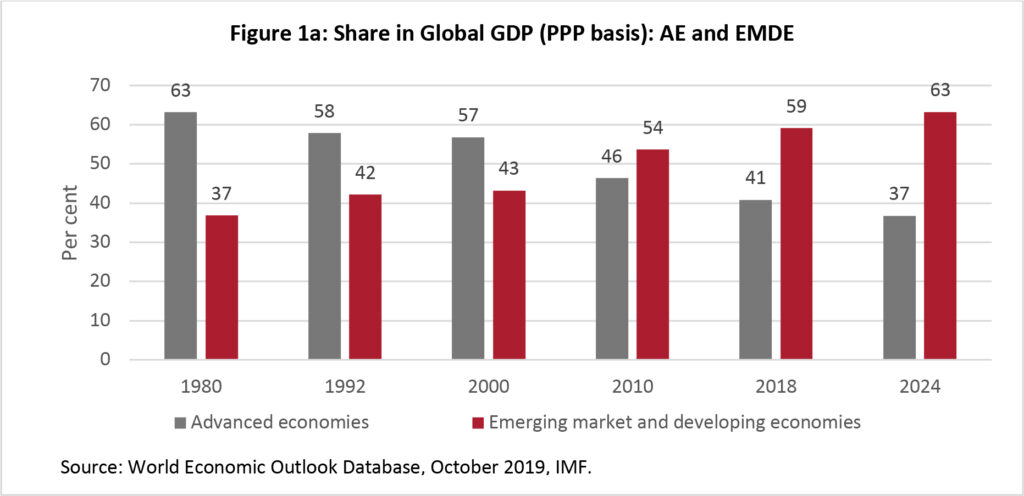

What is remarkable is the pace of change that has been experienced since 2000, with the share of AEs falling rapidly to just over 40 percent now, and the share of emerging market and developing economies (EDEs) increasing correspondingly from 40 to 60 percent (on PPP basis) over the same period. Furthermore, the G7 countries’ share has fallen from 44 to 30 percent, with the share of the BRICS[4] countries rising from 19 to 33 percent over the same period, dominated, of course, by the rise of China. The share of the European Union countries has correspondingly fallen from 24 to 16 percent. As we look ahead, current IMF projections are that the share of BRICS will increase further to 37 percent as that of the G7 falls to 27 percent in 2024 (Figure 1). Barring unforeseen circumstances, this pace of relative change will continue into the foreseeable future, with obvious implications for the need for very significant changes in the governance framework of the global economy in general, and of the IMF in particular.

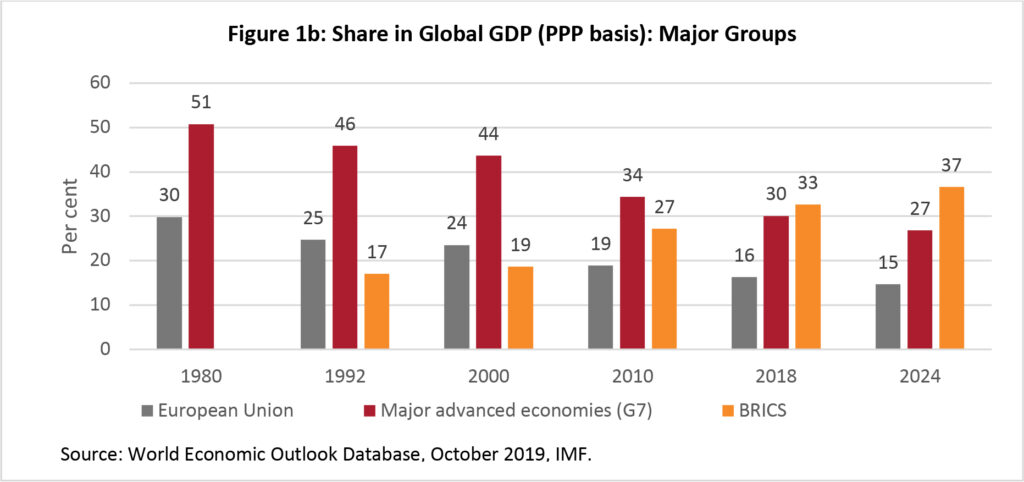

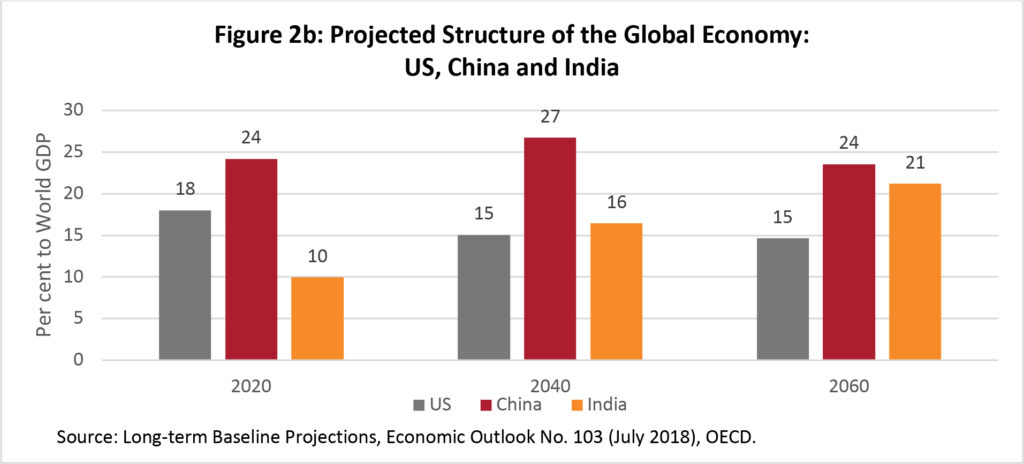

This constitutes a remarkable transformation in the structure of the global economy in a very short period of historical time. Such a pace of change is probably unprecedented in human economic history. It is no surprise then that the existing global economic power and governance structure is finding it difficult to cope with this phenomenal change. “The intimate links between the rise and fall of great powers and the international monetary and financial system is what makes studying the latter so fascinating” (Gourinchas and others, 2019). The last time that such a change took place was at the beginning of the 20th century. Britain was the leader of the world economic system until around World War I and British pound sterling was the operative global currency as the US dollar is now. It took almost 30 years, till the end of World War II, when the United States clearly took over leadership of the global economic system and currency (Kindleberger and Aliber, 2005). This change in the prevailing hegemon was anything but orderly and did not take place quickly. As China’s economy continues to gain in size relative to the United States in the coming years, and possibly even surpasses it (at market exchange rates) within the coming decade, the challenges facing global economic governance will intensify greatly (Figure 2).

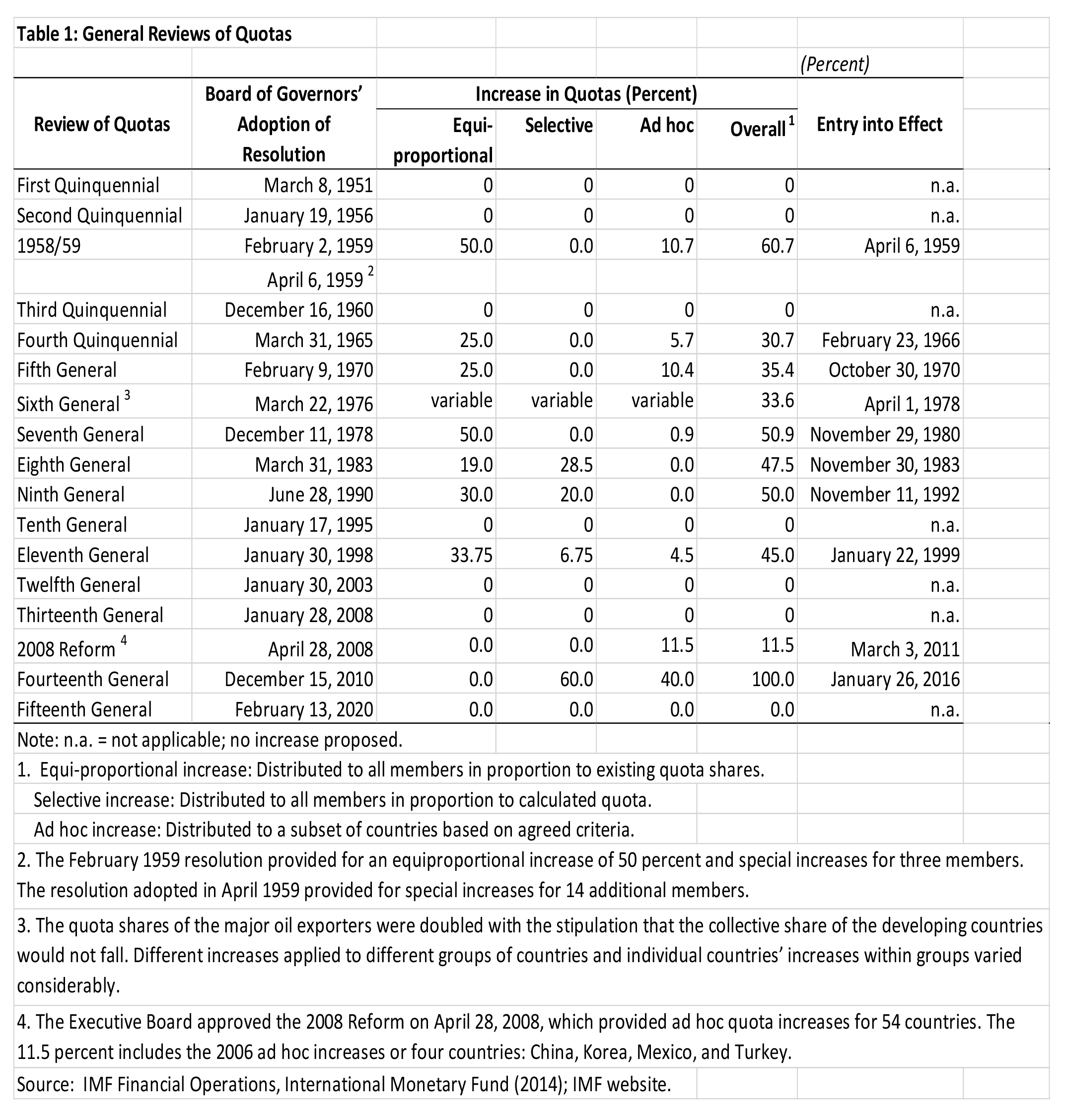

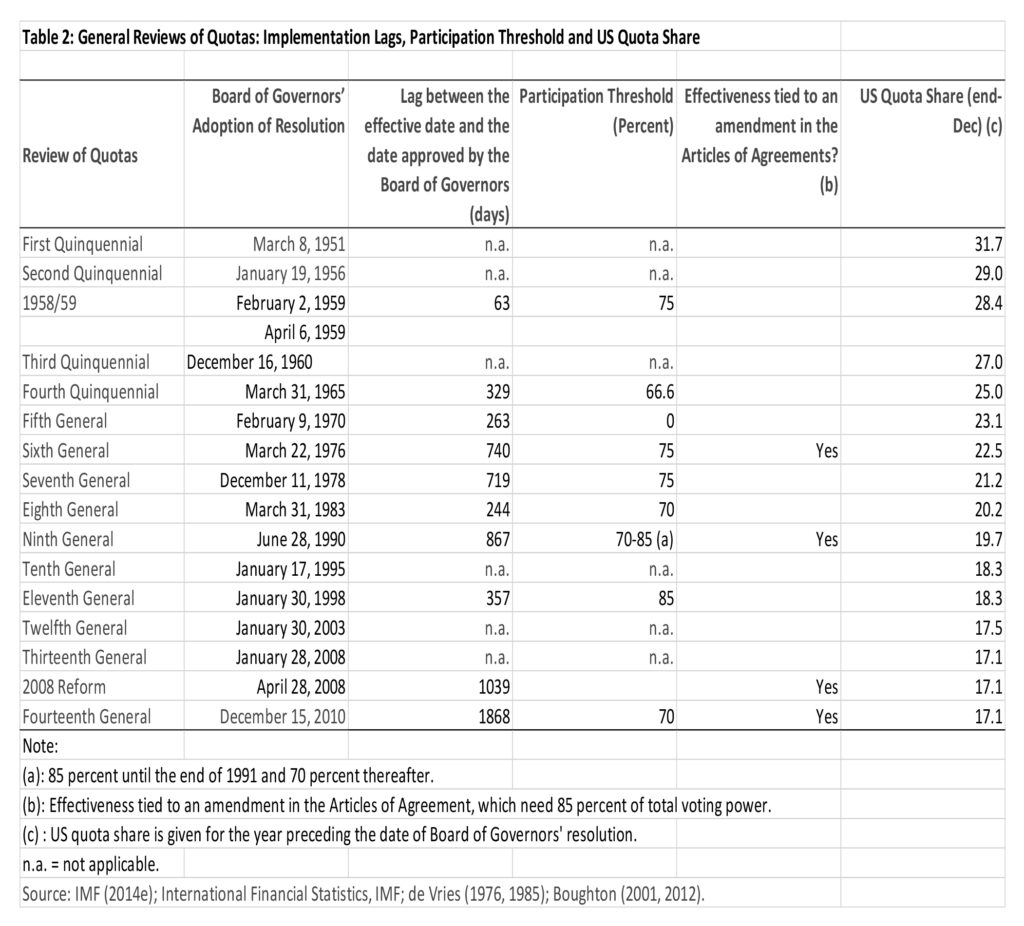

The reluctance exhibited by advanced economies to countenance broader governance changes, despite these momentous economic shifts, is illustrated by the five-year delay in ratification of the 14th Review of IMF Quotas by the United States Congress. The voting and quota structure of the IMF cannot be changed without an affirmative vote from the United States since such a vote requires a super majority in the IMF, which gives the United States an effective veto[5]. This quota reform was approved by the IMF’s Board of Governors in 2010, but it finally came into effect as late as January 2016. This reform doubled the IMF’s quota resources, and brought in some changes in its voting and quota structures. Thus the 2015 change reflected economic data as they existed seven years earlier in 2008. Given the rapid change in the global economic structure during this period, the 2016 quota reform was already obsolete when it came into effect.

The creation of new institutions led by emerging and developing economies, particularly by the BRICS countries, such as the AIIB[6], and the BRICS New Development Bank (NDB) and Currency Reserve Arrangement (CRA), is indicative of these countries’ dissatisfaction with the current slow pace of change in global economic governance. Prospective changes in quotas and voting shares in the IMF would essentially lead to reduction in the shares of the European countries and hence of the G7, which retain disproportionate weights in the IMF despite their shrinking share of the world economy.

The emerging economies’ demand for better representation must also be seen against the backdrop of the North Atlantic financial crisis that originated with US sub-prime troubles in mid-2007. The crisis led to stagnation and weakness in the mature economies, with the recovery being very slow for over a decade after the crisis, whereas emerging economies recorded stronger growth until recently. The ongoing change in economic weight between AEs and EDEs therefore accelerated.

More recent developments in the geopolitical sphere and in the structure of the global economy are contributing to the severe challenges in reforming the global economic governance system, and the IMF in particular. Until recently, say 2015, the rise of the Chinese economy was being successfully assimilated in the global economic system. China’s accession to the WTO in 2001 was widely welcomed and enabled by the incumbent economic powers. This enabled the rapid enhancement of China’s participation in global trade with its ascent to becoming the largest trading nation in the global economy within 20 years. China also became the dominant recipient of foreign investment in the world. The Chinese economy is therefore totally enmeshed within the global economy now. Chinese officials have also gained in prominence among the leadership teams of the IMF[7] and the World Bank in recent years. Furthermore, agreement was reached to include the Renminbi in the SDR[8] basket of currencies in 2016, indicating acceptance by the incumbents of China as a global economic power.

Since then, however, the world’s perception of China has changed significantly, particularly in the United States. As the economic weight of China approaches that of the United States, as their remarkable progress in technology reaches frontiers in many different areas, and as they demonstrate their military power increasingly, the country is perceived to be much more of a threat and competitor. In Asia itself the perception of China as a threatening power has also been exacerbated by its geopolitical aggressive actions in the South China Sea and at the Indian border.

Until recently, there was a great deal of cooperation among the EDEs led by the BRICS countries on issues of global economic governance. With the economies of Russia, Brazil and South Africa slowing in recent years, their voice in international discussions has diminished. Although the Indian economy continued relatively high growth until 2018, it has also shown signs of a slowdown that could extend to the medium-term. With the recent border conflict between India and China on the one hand, and increasing US-Russia tensions on the other, the role of BRICS as a relatively credible pressure group for governance reforms in the IMF and otherwise has also diminished. Within Asia, India’s reluctance to join the RCEP[9] trade agreement also reduces the possibilities of active cooperation among Asian countries.

The enhanced competition and conflict between the US and China on the one hand, and reduced cooperation among the EDEs and the BRICS on the other, pose very serious challenges to significant and meaningful global economic governance reform in the coming years. Clearly, the prospects of reaching some degree of consensus in reforming quotas and governance in the IMF, and of the international monetary system (IMS) overall, have therefore become much more difficult to achieve in the coming years. Unless this happens, however, particularly a much enhanced rule for China in recognition of its emerging economic weight, credibility of the IMF and other global institutions will be in question.

Governance of the IMF cannot be discussed fruitfully without placing it in the context of the IMS, which is what this conference is all about. The objective of the IMS is to contribute to stable and high global growth while fostering price and financial stability. As outlined in the Articles of Agreement that established it, the IMF is required to exercise oversight of the IMS. The obligations of member countries are to direct economic and financial policy towards these ends; to foster underlying economic and financial conditions needed to achieve orderly economic growth with reasonable price stability; and to avoid manipulation of exchange rates while following compatible exchange-rate policies. Thus, the IMF as a multilateral institution has a very specific mandate to ensure the stability and effective operation of the IMS. In order for it to do this effectively, overall credibility of the institution is of the most importance, and hence its governance arrangements.

What has been the performance of the IMS? As detailed in an earlier joint paper (Mohan, Patra and Kapur, 2013; henceforth MPK), the performance of the IMS in the post Bretton Woods period has been mixed. Although the period of the Great Moderation, from the early 1980s until the North Atlantic Financial Crisis (NAFC) in 2008-09, is generally believed to have been successful in terms of low and stable inflation and high growth, it is also characterised by a higher incidence of instability and financial crises. The frequency of banking and currency crises was higher during this period by historical standards.[10] In fact, the incidence of banking and currency crises in the whole post Bretton Woods period (1973-2010) was higher than other previous periods during the preceding century. “Arguably, the post Bretton Woods IMS of flexible/floating exchange rates, freer capital flows and the practice of independent monetary policy has not brought financial stability to the global economy”. So all has not been well with IMF’s superintendence of the IMS.

As MPK observe[11], almost every feature of the IMS has been malfunctioning. First, the system of floating exchange rates has seen greater volatility in exchange rates since the collapse of the Bretton Woods system, and exchange rates are seldom seen to reflect fundamentals. Moreover, there are now many different exchange rate arrangements with the practice of more and more managed floats as opposed to free floats. Second, the free flow of cross-border capital flows has not brought expected benefits to the global economy. They have often been subject to excess flows and sudden stops resulting in financial instability and destabilisation of exchange rates (CGFS, 2009). Third, the interconnection of financial markets along with free capital flows contribute to the enhanced possibility of contagion across countries leading to global financial instability. Fourth, as a consequence, many countries have resorted to higher accumulation of foreign exchange reserves: both with the precautionary motive and as safe assets supporting their respective currencies. This has given rise to a higher demand for US treasuries as the ultimate safe asset, though there has been moderation in growth of reserves in recent years. Fifth, the US dollar continues its role as the global economy’s reserve currency, with no alternative in sight. Expectations of emergence of the Euro as an alternative reserve currency have so far been belied. The weight of the Renminbi remains low and cannot be seen as an active reserve currency in the foreseeable future. Each of these problems in the IMS need to be addressed in the coming years, giving rise to consideration of what the role of the IMF can and should be in the future.

According to most current projections[12], much of global economic growth over the next couple of decades will come from EDEs, particularly from Asia. As the relative weight of the United States economy falls and that of Asia, particularly China, rises, it remains to be seen whether it would be possible for the US dollar to continue its role as the global reserve currency. Is there a possibility that the global demand for safe assets might outstrip the supply of US treasuries in the foreseeable future? The sharp increase in fiscal deficits and public debt in the US (and other AEs), first after the 2008 NAFC and even more sharply now post-Covid, the supply of US treasuries is likely to remain sizable now for at least some more years. Could there be a significant shift in the denomination of world trade transactions away from the US dollar? With continued increase in investment levels in Asia and hence demand for financial resources and intermediation, would Asian capital markets in Singapore, Hong Kong, Shanghai, Shenzhen and Mumbai begin to rival those in New York and London? Will the US Federal Reserve be able to continue its impressive role as the global lender of last resort as it has so ably demonstrated during the NAFC and now in the ongoing Covid crisis? Can we expect to confront the horns of the Triffin dilemma again, even if perhaps in a different form (Gourinchas and others, 2019; Bordo and Macauley, 2018)?

As the emerging economies grow individually and collectively, and as international financial markets become more interconnected, resolution of financial and balance of payment crises now need ever-larger magnitudes of international resources to fund the global financial safety net: witness the size of bailouts that had to be organised for relatively small European countries such as Ireland, Portugal, Cyprus and Greece (in addition to Spain) during the NAFC and its fallout. The resources available with the IMF had to be supplemented by European resources: in fact, the IMF was the junior partner in these programmes in terms of resources. A well-resourced European Stability Mechanism (ESM)[13] has emerged to take care of such problems that may arise in the future in Europe. European countries may therefore have little need for the IMF as a significant source of resources in times of crisis. In the current Covid crisis, for example, the ESM, along with the European Investment Bank (EIB), the European Central Bank (ECB) and the European Commission itself have been collectively active in providing relief to its member countries with no demand for IMF resources[14].

Similarly, the Chiang Mai Initiative (CMIM) also has substantive potential resources (about $240 billion) for addressing crises in Asia, but it has so far not been used[15]. In fact, the behavior of Asian countries during the NAFC reflected a certain degree of lack of confidence in IMF governance. They observed the very differential behavior of the IMF with regard to policy conditionality applied to European countries during the NAFC in contrast with what was done with Asian countries during the Asian financial crisis (AFC) of the late 1990s. Whereas much of policy conditionality imposed during the AFC involved both fiscal and monetary tightening, it was the opposite during the NAFC; moreover ,the IMF packages for Asian countries were seen to be of limited size relative to those provided in the NAFC. As a consequence, countries like South Korea and Indonesia preferred utilising various bilateral arrangements and the swap facility of the US Fed[16] during the NAFC rather than accessing IMF or CMIM resources. They also avoided the CMIM facilities because, beyond certain amounts, they involve linkage to IMF programmes and policy conditionality. When the idea of the “Asian Monetary Fund” was mooted at the time of the AFC it was opposed strongly by the advanced economies and the IMF as well. There was no such opposition to the ESM when that was set up during the NAFC.

All these issues give rise to the perception among EDEs of a lack of evenhandedness on the part of the IMF. This is then related to the issue of appropriate governance of the IMF, the magnitude of its quota resources and their composition.

As of now, these Regional Financial Arrangements (RFAs) do expect to rely on the IMF’s staff for designing programmes, and may still need supplemental IMF resources as necessary. If crises break out in other parts of the world, there will be even greater need for the IMF to function effectively in its role in preserving financial stability and as a lender of last resort. To perform effectively, the Fund must have adequate permanent quota resources to retain and enhance its credibility and legitimacy. So it is essential that its quota resources are increased regularly, commensurate with the expanding size of the global economy and financial markets. Moreover, such regular quota reviews would also ensure that the emerging powers get their rightful share in the IMF’s governance, extending their evolution since 1950. In order to avoid the delay experienced in ratification of the 14th Review, consideration needs to be given to injecting some automaticity in the mandated five yearly quota reviews. The IMF articles already provide for this automaticity through the mandated quinquennial reviews – the issue perhaps is a breach of this in both letter and spirit, as reflected in the 15th review ending after delays without any progress on quotas as well as formula. The deadline for the 16th review has already been extended from 2020 to 2023, notwithstanding the Articles being very clear on no extension.

Decisions on IMF governance and the use of IMF resources can no longer be made in the cosy clubs of the G7 and G10 as they were in the past: some of the action has already shifted to the G20, which effectively brokered the 14th Review agreement led by the United States. However, now even the G20 seems to have been ineffective as seen from the 15th and 16th reviews.

For the Fund as a whole, quotas are expected to provide durable and sufficient magnitude of funds for lending to members as and when the need arises. Each member’s quota determines its voting power as well as its borrowing capacity, and hence the contentious nature of decision-making related to quotas.

A comprehensive history of the evolution of quotas and governance at the IMF is available in a previous co-authored paper (Mohan and Kapur, 2015). So a brief recap is sufficient here. At its founding the IMF was intended to be inclusive in its membership so that it could manage the global economic monitoring system effectively. It started with 40 members: the Axis powers[17] were originally excluded; and then, as a result of the Cold War so were all socialist countries, led by the Soviet Union. So it was anything but inclusive through most of its history. It became truly global with universal membership only in the 1990s after the fall of the Iron Curtain: it now has 189 member countries.

Although, from the beginning, the allocation of quotas has been intended to be based on formulae, in practice actual quotas have emerged from complex bargaining between member countries during each review. Until the 1990s, although the formal decision-making regarding enhancement and allocation of quotas in each review rested with the IMF Executive Board and approval by its Board of Governors, effective bargaining and resolution essentially took place in the G7.

The formulae used have changed continuously becoming increasingly complicated over time until the 14th review. The current formula agreed to by the IMF board in 2008 is perhaps the simplest in the IMF’s history, even if it may still suffer from serious flaws.[18],[19]

From the inception of the IMF, its Articles of Agreement mandate quota reviews to be undertaken at intervals not exceeding five years. Until recently they have indeed been undertaken relatively regularly even though the process has generally not been smooth. Each review entails decisions on two issues: the expansion of total quota resources and their allocation to member countries. In principle, the expansion of resources should bear some relationship to overall expansion in the global economy and global trade; and the reallocation of quotas should reflect the changing economic weight of countries over time. Discussions on both these issues have usually been contentious.

Advanced economies (AEs) have generally tended to resist significant expansion of IMF quota resources, whereas EDEs have favoured relatively larger increases in each review. US administrations often encounter difficulty obtaining Congressional approval, as they did in the recent 14th Review. Thus approvals for significant expansion of IMF quota resources have usually come in the presence of international economic and financial crises, or from unusual pressure applied by the IMF management and the rest of its membership. (It can be said, in general, that potential debtor countries have been more interested in increasing IMF quota resources than the creditor countries). The doubling of IMF quotas in the 14th review, finally implemented in 2015, took place in light of the NAFC when some of the advanced economies themselves became debtors. This expansion took place more than 15 years after the previous one in 1999 (Table 1).

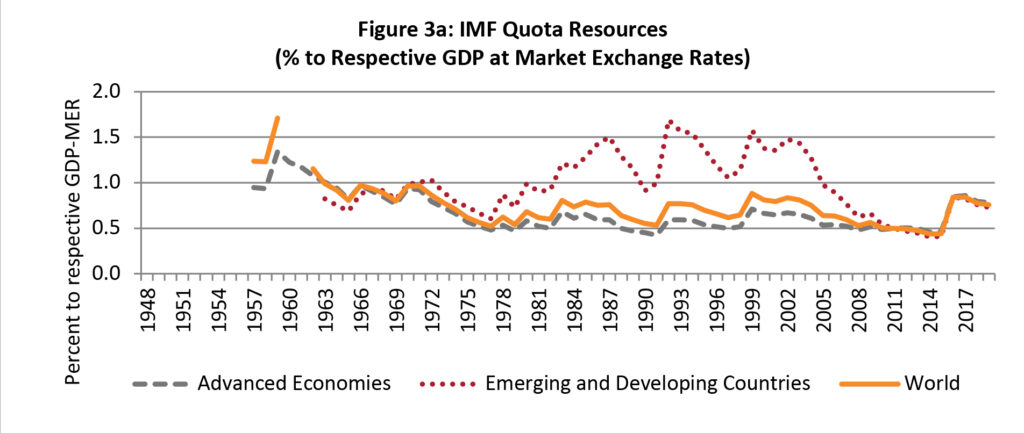

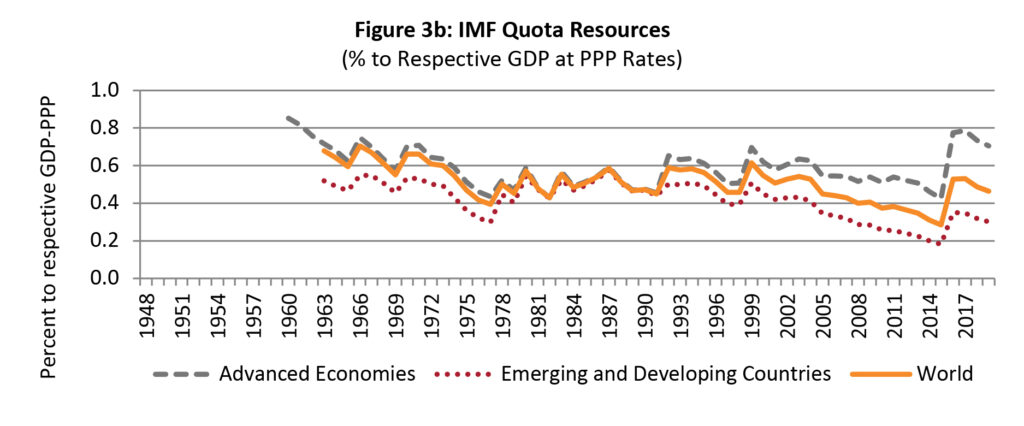

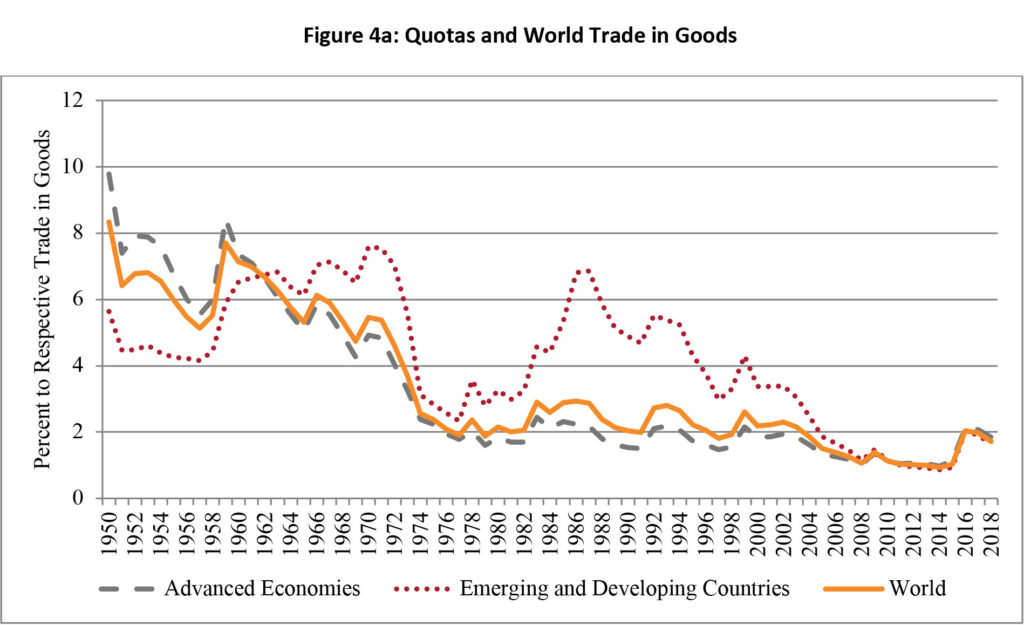

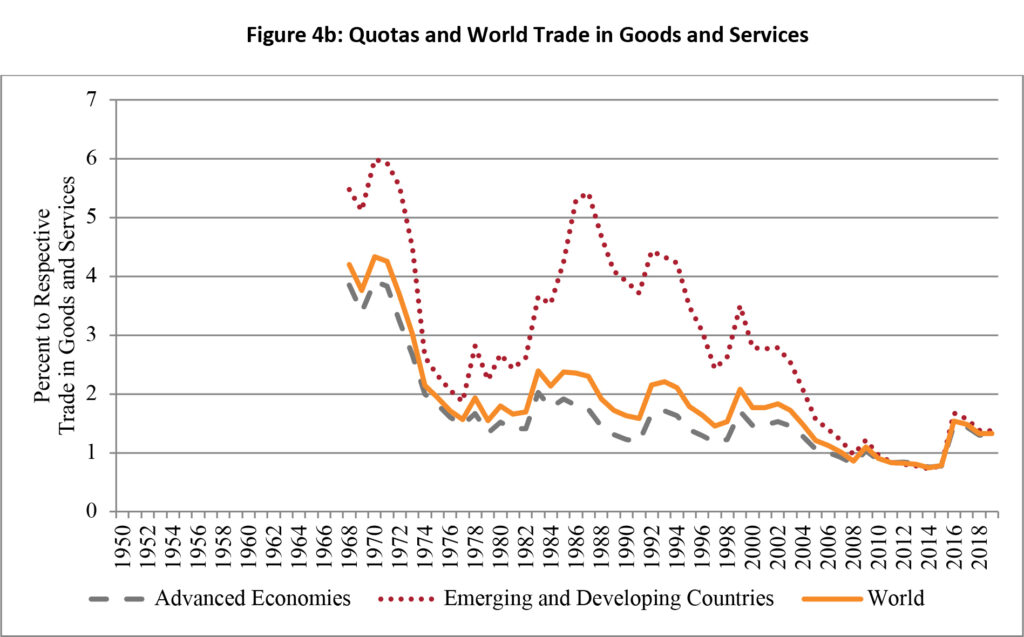

The consequence is that IMF resources have not kept up as a proportion of either global GDP or global trade volumes (Figures 3 and 4). With globalisation and increasing interconnectedness of financial and capital markets, the magnitude of rescue packages has been increasing in times of crisis. Hence the falling share of IMF quota resources contributes to reduction in the credibility and effectiveness of the IMF. There have been delays in quota reviews and also in their implementation: there have been significant lags between the approval of reviews by the IMF’s Board of Governors and the date of their effectiveness (Table 2). Such delays have meant that that the IMF gets the resources it needs somewhat late in relation to its needs. This has necessitated increased reliance on borrowed resources: earlier on the General Arrangement to Borrow (GAB) and now on the New Arrangement to Borrow (NAB), supplemented by Bilateral Borrowing Arrangements (BBA) in recent years after the NAFC.[20] If, instead, IMF quota resources were to be enhanced by magnitudes similar to the various arrangements to borrow there would be consequent significant reallocation of quotas, which will inevitably increase the shares of the dynamic EDEs at the expense of AEs, particularly European countries.

At present, the total quota resources of the IMF amount to SDR 477 billion (US $ 651 billion), which are supplemented by NAB of SDR 182 billion (US $ 249 billion) and BBA of SDR 318 billion (US $ 434 billion). The NAB resources are slated to double SDR 365 billion (US $ 500 billion) by the end of 2020. There has also been agreement on the framework to begin a new round of bilateral borrowing which will become effective at the beginning of 2021.[21] Thus, quota resources will soon amount to less than half of total IMF resources. The availability of such large borrowed resources through generous contributions of the membership demonstrates that the need for adequately resourced IMF is recognised by its larger members. It, therefore, serves to provide a degree of perceived stability to the IMS along with a certain degree of complacency regard to availability of liquidity if needed. On the other hand, however, such availability of resources reduces the pressure for enhancement of permanent quota resources and, consequently, the reapportionment of quotas and associated changes in voice and representation that would otherwise accrue to the fast-growing emerging market countries, particularly China.

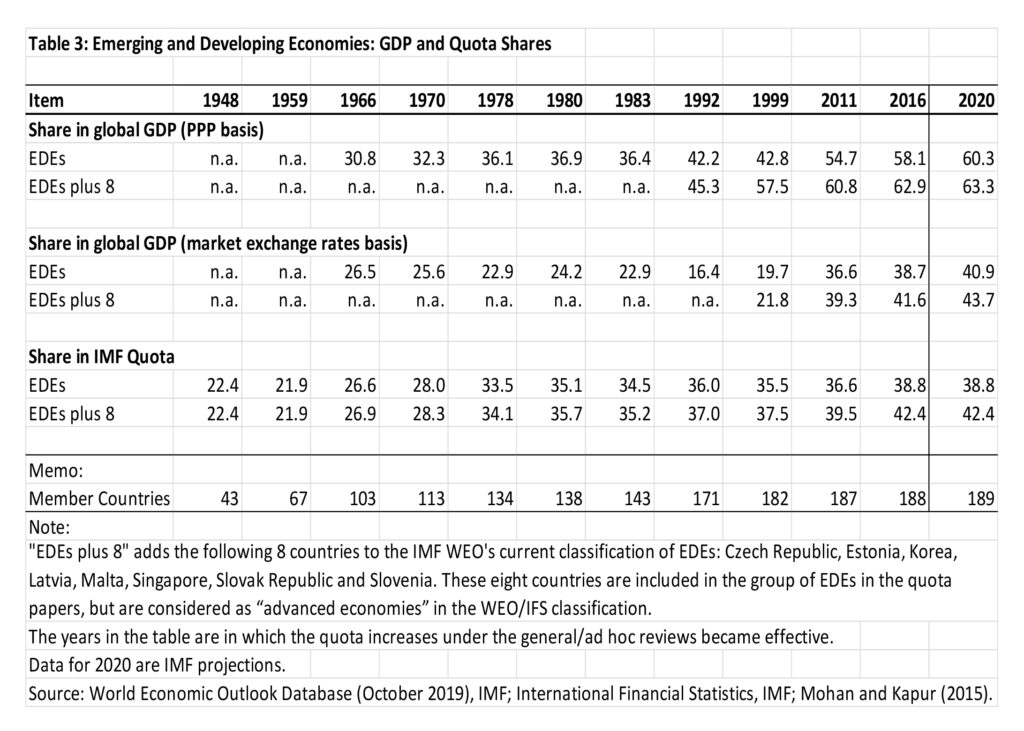

Until the 1980s the pace of change in the distribution of global GDP was relatively slow as between AEs and EDEs, and their share in IMF quotas was broadly consistent with their GDP shares. This is despite the Asian economic miracle which started in the 1970s and gathered pace in the 1980s and beyond, since the initial economic weight of these countries was small. There was little palpable change in the EDEs overall economic weight in the world, increasing from around 30 percent in the mid-1960s to just over 40 percent by 2000 in terms of global GDP (PPP basis), with the 1990s increase being partially accounted for by the addition of all the former socialist countries IMF’s membership.[22] It is in the 1990s, and accelerating after 2000, that their share in global GDP began to increase whereas their quota share did not keep pace accordingly. There has been a dramatic increase in their share of global GDP since 2000 from just over 40 percent to about 60 percent now in PPP terms, and a doubling from about 20 percent in 2000 to about 40 percent in MER terms. Over the same period the EDE share in IMF quotas has remained relatively stagnant increasing from around 35 percent in 2000 to just 39 percent now, even after the 14th review which was finally implemented in 2016 (Table 3). The underrepresentation of EDEs in IMF quota distribution and hence in governance is therefore becoming more and more stark by the day.

The advanced economies have effectively been dragging their feet on governance changes over the past couple of decades just as the weight of EDEs in global GDP started increasing rapidly (Table 4). There was no significant expansion in total IMF quotas from 1998 until the 14th Review (2010) implementation in 2016. Redistribution of quotas can only take place when there is an overall expansion of IMF quota resources. Countries retain their existing quotas through each review and it is only the incremental expansion that is subjected to the distribution formula that is agreed to in the review. Hence there is a built in hysteresis in quota shares and hence voice and representation in the governance of the IMF. The increase in EDE weight is of course dominated by that of China (Table 5). The share of China in global GDP on PPP basis has already surpassed that of the United States. If current trends continue, as they are likely to, China’s GDP at market exchange rates is also likely to exceed that of the United States within the next decade.

The problem of further reform of governance in the IMF has now been compounded by the standstill agreed to in the 15th review completed in 2019.[23] First, as a consequence of the unprecedented delay in implementation of the 14th review until 2016, the 15th review, could not be conducted in 2015 as it should have been according to the five-year review schedule: it was finally concluded in 2019. Second, the 16th Review should in fact have been completed this year in 2020: it is now scheduled to be conducted in 2023. It is then unlikely for an agreement on the 16th Review to be reached before 2025 and, going by past patterns, for implementation to take place much before 2027.[24] The quota distribution resulting from the 14th Review was based on 2008 economic data will therefore stand until around 2027. By then it will be out of date by almost 20 years, thereby accentuating the governance imbalance immensely.

As illustrated in Table 5, if the 14th Review quota formula is applied to 2016 data, China’s calculated quota share (CQS) would already be 12.9 percent, about double its actual current share of 6.4 percent (IMF, 2018).[25] Moreover, the share of the United States on this basis would have fallen to 14.7 percent, that is less than the 15 percent it needs to retain its veto power in the IMF with respect to major decisions, such as quota reviews, which require a super majority of 85 percent. If the 15th Review had not resulted in a standstill, and if it had retained the 14th Review formula, this would probably have been the consequence. The share of the G7 would have fallen, as of the AEs as a whole. Correspondingly, the share of the BRICS countries would have risen, along with EDEs as a whole. In the event, no consensus could be reached and the 15th Review exercise was effectively shelved. Instead, it was agreed to double the NAB in order to keep the IMF adequately resourced. Presumably, the advanced economies were not ready to accept the consequences of a proper review at this time for obvious reasons.

After the failure of the 15th Review, the IMF’s Board of Governors (BOG) has, however, given the following direction to its executive board:

“The Sixteenth General Review of Quotas under Article III, Section 2(a), will continue beyond December 15, 2020 and shall be concluded no later than December 15, 2023. In this context, the Executive Board is requested to revisit the adequacy of quotas and continue the process of IMF governance reform, including a new quota formula as a guide, and ensure the primary role of quotas in IMF resources. Any adjustment in quota shares would be expected to result in increases in the quota shares of dynamic economies in line with their relative positions in the world economy and hence likely in the share of emerging market and developing countries as a whole, while protecting the voice and representation of the poorest members.” (IMF, 2020)

The directions from the BOG, therefore, do enjoin the Board to:

- Assess the adequacy of the quotas.

- Ensure the primary role of quotas in IMF resources.

- Evolve a new quota formula.

- Increase the shares of dynamic economies.

- Protect the voice and representation of the poorest members.

It remains to be seen, however, whether it will be possible for the IMF Executive Board to comply with these directions in both letter and spirit within the next three years. What are the key problems that are likely to arise?

First, the enhancement of total quota resources would have to be very significant if the second objective is to be realised. If the NAB and the BBA are to be eliminated in order to restore the primary role of quotas in IMF resources, they would need to be at least doubled, as they were in the 14th Review. Expansion of quotas has always been resisted by the advanced economies, particularly by the United States Congress. There is little reason to expect any change in this regard in the years to come. Because of the economic ravages wrought by Covid 19, budgets of all countries, AEs and EDEs alike, have been severely extended increasing their debt GDP ratios beyond previous levels. Economic recovery from the current severe crisis is currently unpredictable; and so is the restoration of national budgets to some degree of normalcy by 2023. So the appetite of national legislatures to agree to a significant increase in the IMF quotas, and hence their contributions, is likely to be low by the time the 16th Review is conducted. It is notable that, during the NAFC, when the new debtor countries were largely the AEs, relatively quick agreement took place to double quota resources in the 14th Review. This time, despite the crisis being truly global, there has been no inclination to take any action on the IMF’s quota resources. Instead, agreement has been reached to double the NAB and continue with the BBA thereby preserving the status quo as far as governance is concerned. With Europe having become almost self-sufficient in terms of a financial safety net through the establishment of the ESM, and the recent agreement to activate the European Commission for providing relief to its member countries, the demand for IMF resources has come almost exclusively from EDEs. So the vast majority of debtor countries are once again EDEs.

Second, the United States is unlikely to accept its quota share falling below the 15 percent threshold. It will be difficult to avoid this if the 14th review quota formula is persisted with. In fact, application of 2016 data to CQS already shows the US quota share falling to 14.7 percent (Table 5). Thus if 2022 data are used in the 16th Review it is likely that the US share will fall even further. This would suggest that the CQS formula will again need to be revisited in the 16th Review as directed by the Board of Governors. Judging from past experience such a review will be extremely contentious and it will not be easy to arrive at a consensus. More on this below.

Third, increasing the share of EDEs will mainly result in a very substantial increase in the share of China. The CQS applied to 2016 data already shows China’s share will increase to 12.9 percent. Application of 2022 data will no doubt increase this further. As of now, China has already begun recovery from the Covid crisis much faster than the rest of the world. It is, therefore, possible that the increase in its economic weight in the world could even accelerate by 2022, thereby implying an even greater increase in its quota share if the 14th Review formula is applied. As commented earlier, apart from resistance from advanced economies, particularly the United States, there could now be emergence of similar resistance from other EDEs since many have already slowed down: the differential impact of the current crisis on EDEs is, however, difficult to assess at present.

It is also possible that other EDEs may be somewhat wary of China’s dominance in global economic governance. There has not yet been much experience of China assuming such leadership in global governance fora. Hence, even if many of the EDEs may not be satisfied with current governance structure of the IMF, it is possible that they may prefer predictability of the current arrangements rather than venturing into uncertainty regarding a larger Chinese role. The recent border clash between India and China and the consequent actions by India in terms of economic and trade restrictions on China would cast into doubt future cooperation between these two largest EDEs. Similar issues may cloud the willingness of other Asian countries as well in terms of acceptance of Chinese leadership. Thus achievement of consensus among EDEs themselves will be problematical in the 16th Review.

Fourth, the ongoing Covid crisis has now plunged the global economy into a deep recession and increased uncertainty with regard to its future evolution. With the economies of the lowest income countries in sub-Saharan Africa and elsewhere taking a substantial hit due to the Covid crisis, increasing their voice and representation through quota enhancements could become that much more challenging, once again suggesting a significant change in the quota formula. Even before the emergence of this latest crisis, emerging economies were no doubt experiencing a significant slowdown, some due to the downturn in oil and commodity prices, and others due to the surfacing of unaddressed structural problems. As of now it is too early to say when the global economy will return to some degree of normality. It remains to be seen which segments of the global economy will suffer more and which will recover faster. Until now, Asian countries have exhibited a lower impact of Covid, which suggests the probability of a faster recovery, particularly by China.

Fifth, when the global economy does return to a path of sustained growth, which is certainly feasible given appropriate policy responses and fading of the virus, it is likely that emerging markets will resume a growth path which is in excess of that of the AEs. The economic growth of BRICS countries, particularly China and India, should then continue to be higher than that of the AEs for the foreseeable future. They will then continue to acquire larger economic weight because of their population size and higher growth, despite relatively low per capita incomes. Their demand for increased voice and representation in the IMF and other fora for global economic governance can therefore be expected to continue to increase in the foreseeable future.

The IMF and its member countries therefore have their work cut out for arriving at some degree of consensus as they approach the 16th Review. With the current voice and representation through quota shares being based on the members’ economic weights in 2008, the 16th Review will undoubtedly involve a very significant change in the current governance framework as it gets updated to at least the 2022 global economy data. It would probably involve the largest change since the IMF’s inception. The decisions taken in this review will therefore determine the IMF’s future for quite some time to come.

As a response to the 2008-09 financial crisis, and now the COVID crisis, all advanced economies, the United States, the United Kingdom, the Eurozone and Japan, have practiced unconventional, excessively accommodative monetary policies for an extended period. Interest rates have been near zero in all these jurisdictions for almost 10 years. Although these policies did succeed in staving off a depression, economic recovery was slow. Just as the global economy was approaching some degree of normality, the Covid crisis hit early this year. In response, another bout of accommodative monetary policies and even more expansionary fiscal policies have been put in motion in all the leading economies of the world, and other jurisdictions have followed suit. Global trade had not yet fully recovered from the NAFC and it has now suffered another body blow. It is too early to speculate how long this crisis will last and how long it will take for the global economy to recover to its pre-Covid state. And then what its growth path will be post the recovery. Will the road to recovery be smooth or will we see the emergence of potholes and speed breakers on the way?

The excessively accommodative monetary policies and associated low interest rates had already led to much greater borrowing by both public and private sectors worldwide since the NAFC. Hence large debt overhangs have emerged in advanced economies and emerging markets alike. The increase in debt globally has already been larger, faster, and more broad-based since the NAFC than in the previous three waves (Kose and others, 2020). The Covid response will only serve to accentuate this trend even further with exploding debt GDP ratios in AEs and EDEs alike. Along with the widespread ongoing trade disruption, this should thus be seen as a leading indicator for the enhanced probability of financial crises occurring in the near and medium term. Moreover, financial globalisation is unlikely to be reversed with new possibilities of cross-border contagion.

Consequently, at the current juncture there is an even greater need for the IMS and the International Monetary Fund within it to be seen to be effective and credible. Thus it needs to be adequately resourced and to exhibit enhanced and credible governance.

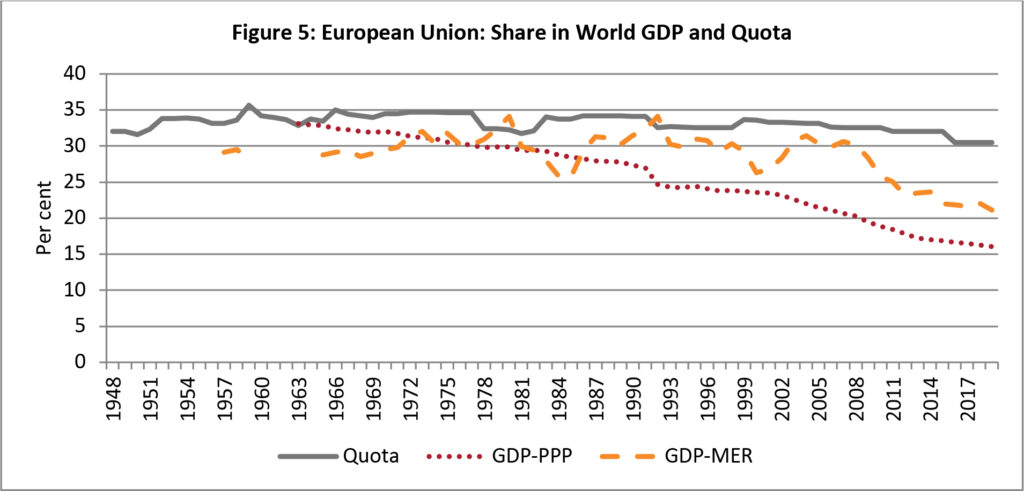

For it to regain credibility and effectiveness, the IMF’s governance structure clearly has to become more inclusive. The US needs to retain its leadership role, in its own as well as in the wider international interest. European countries remain overweight, with the ‘advanced Europe’ group (European Union, Norway and Switzerland) taking a third of board seats, and more than a third of board voting power. The relative constancy of their quota shares is striking, since their share in GDP has been falling consistently (Figure 5). The European Union share (including the UK) of global GDP is now just over 16 percent (PPP basis) or 21 percent (MER basis). The key governance change in the IMF will therefore involve a significant reduction of the quotas of European countries and associated reduction in the seats that they occupy in the IMF board, along with a corresponding increase in the share of EDEs and of the United States.

Furthermore, the Bretton Woods institutions since inception have been headed by European nationals in the IMF and US nationals in the World Bank. This pattern has continued for more than seven decades now. Thus, nationality has turned out to be the guiding criterion to head the Bretton Woods organisations and nationals of other countries, irrespective of their merit, have been excluded from the process. This must be corrected. Other institutions such as the World Trade Organisation have already shown the way; there is no reason why the Fund in coming years cannot find procedures that could result in the same outcome.

As discussed elsewhere in this conference, the way forward could include a wider rearrangement of the international monetary system with corresponding changes in the evolving role of the IMF. As already noted, the various RFAs, particularly the ESM and CMIM, now collectively have potential resources that could exceed those of the IMF. If the CMIM transforms itself to becoming the Asian Monetary Fund with an appropriate institutional structure, it could perform the same role in Asia as the ESM is already doing in Europe. Furthermore, the US Federal Reserve has acted as an effective lender of last resort to selected central banks through their swap facilities during the NAFC and now in the Covid crisis. In the current crisis, they have expanded their range of facilities with a new repo facility for central banks that are not eligible for their swap facilities. In addition, there has been an increasing range of bilateral swap facilities being offered by central banks to selected counterparts that have emerged in different parts of the world. The speed of these facilities is usually much faster than those provided by the IMF, with generally lower conditionality and lack of perceived stigma.

The IMF is obviously aware of these developments and has been seeking a greater coordinating role, though without significant success so far (IMF, 2017, 2018a).[26] In the same vein, Ted Truman is proposing a multilateral swap mechanism through which the major central banks can use their foreign exchange reserves to augment the resources of the International Monetary Fund and thereby strengthen the GFSN. In any case, EDEs have also been following external management policies that involve accumulation of precautionary foreign exchange reserves that then enhance their ability to maintain financial stability, maintain their own policy independence, while reducing their need to resort to external financing in times of need.

Overall, the global financial safety net has therefore changed significantly over the last 10 to 15 years with a range of different facilities becoming available in addition to those of the IMF in the event of financial crises occurring. If the IMF is to evolve into a somewhat different role as a coordinator of these different facilities, along with operating its own, the need for reforming its governance assumes even greater importance. It would need to reflect better the changing global economic composition, with EDEs getting appropriate recognition and role in its governance along with enhanced quota allocations. Only then can we expect acceptance of such an enhanced role in global economic governance.

What could be the key ingredients of such a change? Very clearly, reviews of IMF quotas and governance need to be more radical – with significant implications for overall quota and voting shares.

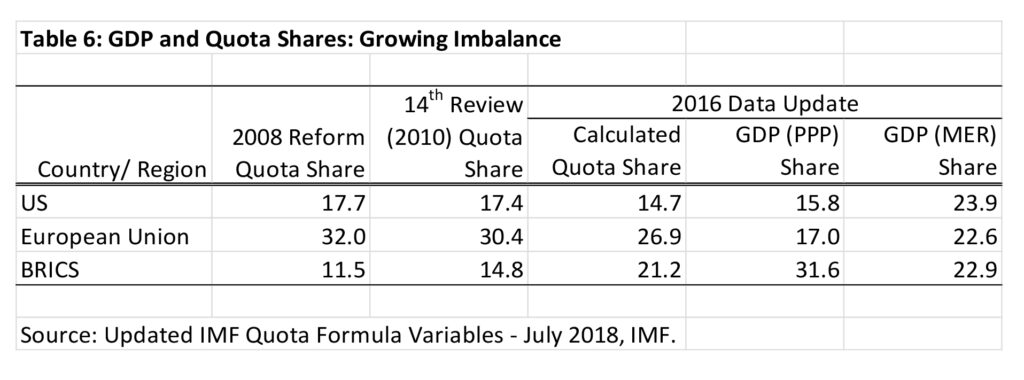

First, as China approaches or even surpasses the United States in its share of global GDP at market exchange rates[27] its quota share would have to be of a magnitude similar to that of the United States. Second, the share of the European Union countries, including that of the UK, will have to reduce significantly. At present, whereas the GDP shares of the United States and the European Union are broadly similar at both the PPP[28] and MER[29] bases, their quota shares in the IMF are totally inconsistent. After the 14th Review, the quota share of the United States is 17.4 percent, while that of the European Union (including the UK) is still as high as 30.4 percent. Third, the quota share of BRICS countries would have to increase significantly. There is a similar imbalance between the economic weights of the BRICS countries and the European Union. Whereas the BRICS share in global GDP is similar to that of the United States and European Union on an MER basis, it is already much higher than both on PPP basis, at almost double that of the United States (Table 6). Fourth, the role of other EDEs, particularly low-income countries, in governance of the IMF also needs to be enhanced. One way of doing this would be to increase allocation of the basic votes which every country gets regardless of size. In addition, as the number of board seats that European countries have today reduces, consistent with reduction in their quota shares, the number of board seats allocated to EDEs can then be increased. At present the whole of sub-Saharan Africa has only two board seats in the IMF: at a minimum, this number must be increased to three, as it already has in the World Bank.

The kind of changes proposed above, both in the nature of the international monetary system as a whole and the role of the IMF within it, and in the transformation of relative quota shares, will be extremely contentious and hence difficult to implement. On the one hand, it will require a certain degree of enlightened leadership, while on the other will need a spirit of compromise from all sides.

Whereas there needs to be an overhaul of global economic governance, giving a greater role to emerging economic powers, it is still necessary for the US to retake leadership in the IMF and in global economic governance, but now it will need to indicate that it is willing to share it with a resurgent China.

US financial markets continue to be the most dominant in depth and efficiency – and the dollar is still the world’s dominant reserve currency and is likely to remain so for the foreseeable future. US leadership of the IMS and hence of international institutions remains of great value. It is important that, among the advanced economies, the US retains its dominant position. The Bretton Woods institutions owe their founding to US vision after the Second World War. Although the role of the emerging economic powers is increasing, their soft power is not rising at the same pace, underlining the importance of maintaining US leadership.

As already noted, what is remarkable is that, in addition to the under-representation of the BRICS, and of China in particular, the country that is most underrepresented in the IMF, in relation to its share in global GDP, is the US. Thus correction of this striking imbalance in favour of the US is essential to preserve US leadership in the IMF and overall in global economic governance. The chances of obtaining congressional approval for future radical quota reviews would also be enhanced if such a correction is done so that there is no imminent probability of the US quota share falling below 15 percent. The existing quota formula will need revision to accomplish this: essentially the role of GDP would need to be increased and that of openness reduced. With such a revision, the share of both the United States and China will increase, with the latter approaching that of the United States, or exceeding it over the next decade or so. If an appropriate correction is carried out in this manner, it would both postpone by some years the prospect of the US quota share dropping below the important 15 percent threshold, and enable China to also approach this threshold over some period of time.

It would also better reflect the changing composition of the global economy on a dynamic basis, with the emerging economic powers getting better representation along with the United States. On this matter there is a confluence of interest between the emerging economic powers and the United States.

Such an agreement would require great enlightenment, statesmanship and wise diplomacy on all sides. In view of the vastly increased geopolitical tensions in both economic and political spheres, the likelihood of such an approach cannot be deemed to be high at this time. The consequence of the absence of such progress would essentially mean the withering of the IMF as the key institution responsible for the international monetary system. We would then observe an increasing number of regional and other arrangements for the maintenance of financial stability, just as we observed the emergence of a potpourri of trade arrangements with the weakening of the World Trade Organization over the past decade.

The international monetary system and the GFSN will then essentially be a fragmented one, and the role of the IMF in global economic governance will be reduced and of a different character.

Bordo, Michael D. and Robert N. McCauley (2018). Triffin: Dilemma or Myth? NBER Working Paper No 24195. Cambridge, Mass. National Bureau of Economic Research.

https://www.nber.org/papers/w24195.pdf

Committee on the Global Financial System (2009). Capital Flows and Emerging Market Economies. CGFS Papers No 33. Basel: Bank for International Settlements (BIS).

https://www.bis.org/publ/cgfs33.pdf

Gourinchas, Pierre-Olivier, Helene Rey and Maxime Sauzet (2019). The International Monetary and Financial System. Cambridge, Mass. National Bureau of Economic Research. NBER Working Paper 25782.

http://papers.nber.org/tmp/30985-w25782.pdf

International Monetary Fund (2017). “Collaboration Between Regional Financing Arrangements and the IMF”. Washington D.C. International Monetary Fund: IMF Policy Paper.

International Monetary Fund (2018a). “The Exchange of Documents Between The Fund And Regional Financing Arrangements”. Washington D.C. International Monetary Fund: IMF Policy Paper.

International Monetary Fund (2018b). “Updated IMF Quota Data—July 2018”. Washington D.C. International Monetary Fund.

https://www.imf.org/external/np/fin/quotas/2018/0818.htm

International Monetary Fund (2020). “Fifteenth and Sixteenth General Reviews of Quotas—Report of the Executive Board to the Board of Governors”. Washington D.C. International Monetary Fund.

Kawai, Masahiro (2015). From the Chiang Mai Initiative to an Asian Monetary Fund. ADBI Working Paper No 527. Tokyo: Asian Development Bank Institute.

https://www.adb.org/sites/default/files/publication/160056/adbi-wp527.pdf

Kindleberger, Charles P. and Robert Z. Aliber (2005). Manias Panics and Crashes: A History of Financial Crises. Hampshire: Palgrave Macmillan.

Kose, M. Ayhan, Peter Nagle, Franziska Ohnsorge and Naotaka Sugawara, (2020). Global Waves of Debt: Causes and Consequences. Washington D.C.: World Bank.

http://pubdocs.worldbank.org/en/377151575650737178/Debt-Chapter-1.pdf

McKinsey Global Institute (2018). Outperformers: High-Growth Emerging Economies and The Companies That Propel Them.

https://www.mckinnot sey.com/~/media/McKinsey/Industries/Public%20and%20Social%20Sector/Our%20Insights/Outperformers%20High%20growth%20emerging%20economies%20and%20the%20companies%20that%20propel%20them/MGI-Outperformers-Full-report-Sep-2018.pdf

Mohan, Rakesh, Michael Debabrata Patra and Muneesh Kapur (2012). The International Monetary System: Where Are We and Where Do We Need to Go? IMF Working Paper No 13/224. Washington DC: International Monetary Fund.

https://www.imf.org/external/pubs/ft/wp/2013/wp13224.pdf

Mohan, Rakesh and Muneesh Kapur (2015). Emerging Powers and Global Governance: Whither the IMF? IMF Working Paper No 15/219. Washington DC: International Monetary Fund.

https://www.imf.org/external/pubs/ft/wp/2015/wp15219.pdf

OECD (2020). Economic Outlook: Statistics and Projections (database) “Long-term baseline projections, No. 103”,

https://stats.oecd.org/viewhtml.aspx?datasetcode=EO103_LTB&lang=en

FOOTNOTES

[3] The Group of Seven (G7) consists of the seven largest advanced economies in the world: Canada, France, Germany, Italy, Japan, the United Kingdom and the United States.

[4] An informal grouping of Brazil, Russia, India, China, South Africa.

[5] This congressional blockage was ironic because the US was the principal architect of the 2010 accord in the IMF board of governors. The US has 17.7 percent of IMF quota shares and hence an effective veto over important decisions that require a ‘super-majority’ of 85 percent.

[6] Asian Infrastructure Investment Bank was founded in 2016 under China's leadership.

[7] By informal agreement one of the four deputy managing directors of the IMF is now nominated by the government of the People's Republic of China. A recent CEO of the international Finance Corporation was also a Chinese national.

[8] Special Drawing Rights.

[9] The Regional Comprehensive Economic Partnership (RCEP) is a proposed free trade agreement in the Indo-Pacific region between the ten member states of the Association of Southeast Asian Nations (ASEAN), namely Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam, and five of ASEAN's FTA partners—Australia, China, Japan, New Zealand, and South Korea.

[10] See Pp 6-7 and Table 2 in Mohan, Patra and Kapur, 2013.

[11] Pp 40-41 in MPK.

[12] e.g. McKinsey Global Institute (2018); OECD (2018).

[13] The ESM has a capital of € 700 billion of which over € 80 billion is paid in; its lending capacity is €500 billion, of which €410 billion is still available (During the NAFC it lent almost € 110 billion to programme countries, along with another € 180 billion that were committed by the EFSF). In the current COVID crisis, it has announced the availability of up to € 240 billion as part of the European programme of “Rescue Funds”, but there has been no request for the funds so far.

[14] https://www.esm.europa.eu/content/europe-response-corona-crisis

[15] The Chiang Mai Initiative still does not have an adequate institutional framework giving rise to for transforming it into an “Asian Monetary Fund”. E.g. in Kawai, 2015.

[16] Only South Korea could access the US Fed swap facilities, not Indonesia.

[17] Germany, Italy, Spain and Japan.

[18] See table 2, pp. 18/19 in Mohan and Kapur, 2015, for details of changes in the formulae used over time.

[19] The current quota formula is a weighted average of GDP (weight of 50 percent), openness (30 percent), economic variability (15 percent), and international reserves (5 percent). For this purpose, GDP is measured through a blend of GDP—based on market exchange rates (weight of 60 percent) and on PPP exchange rates (40 percent). The formula also includes a “compression factor” that reduces the dispersion in calculated quota shares across members.

https://www.imf.org/external/np/exr/facts/pdf/quotas.pdf

[20] https://www.imf.org/en/About/Factsheets/Where-the-IMF-Gets-Its-Money#:~:text=2016%20Bilateral%20agreements&text=Bilateral%20Borrowing%20Agreements%20serve%20as,financing%20needs%20of%20its%20members. Accessed on August 20, 2020.

[21] https://www.imf.org/en/News/Articles/2020/03/31/pr20123-imf-executive-board-approves-framework-for-new-bilateral-borrowing-agreements. Accessed August 24, 2020.

[22] In market exchange rate (MER) terms, their weight actually fell from just over 25 percent in the mid-1960s to about 20 percent around 2000.

[23] https://www.imf.org/en/News/Articles/2020/02/13/pr2050-imf-board-of-governors-approves-a-resolution-on-quota-reviews

[24] This makes the strong assumption that there will indeed be an agreement for an increase in quotas as well as a new quota formula. The possibility of this review going the way of the 15th Review cannot be ruled out at present.

[25] The IMF seems to have slowed down in releasing data on the annual quota updates/reviews to the public. For example, as of September 2020, we have CQS based on 2016 data, whereas CQS based on 2018 data should have become available by now. Second, the IMF is now releasing somewhat limited data compared with earlier releases. The typical comprehensive Board paper, rich in analytics, was not released along with the data for 2016. The excel file gives only country-wise data and no information is provided on group-wise shares. For individual researchers it is a tedious exercise to compile these aggregates, which are more insightful. Both the lack of the data and the analytical note constrain an analysis by the outside public/experts and perhaps takes the issue away from limelight and reduces outside pressure for IMF governance reforms.

[26] In the context of the Covid Crisis, the IMF Managing Director took a step forward and held a coordination meeting with the heads of RFAs in April 2020.

[27] In PPP terms China’s share in global GDP is already higher than that of the United States.

[28] About 16-17 percent each.

[29] About 22-24 percent each.

Rakesh Mohan

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.