The Response of the Reserve Bank of India to Covid-19: Do Whatever it Takes

Reading Time: 26 minutesEditor's Note

This Working Paper was first published as a chapter in Monetary Policy and Central Banking in the Covid Era, edited by Bill English, Kristin Forbes, and Angel Ubide, CEPR e-book, Centre for Economic Policy Research: June 2021.

DOWNLOADS

Executive Summary

India responded to Covid-19 as soon as it was becoming clear that a pandemic was in the offing. The government imposed a sudden nationwide total lockdown on March 25, 2020. This lasted until end of May 2020 and was then lifted in phases subsequently. The country suffered a severe economic contraction with GDP estimated to have fallen by 24% in Q1 FY 2021 and by 7.3% in FY 2020-21 as a whole. The policy response to the economic impact of both the pandemic and the consequent lockdown was the usual mix of fiscal, monetary and financial measures, but relatively light on fiscal measures. At 2-2.5% of GDP, India’s stimulus spending has been at the lower end amongst emerging markets.

This paper discusses the role of Reserve Bank of India (RBI) in India’s fight against the pandemic. It documents the various policies undertaken by the RBI in its capacity as the monetary authority, lead financial system regulator and supervisor of financial intermediaries, banker to and debt manager of the central and state governments, currency issuer and manager, and regulator and operator of the payment and settlement system. The paper also decodes numerous policy instruments at the disposal of RBI and effectiveness of measures such as the credit enhancement schemes, and loan moratoriums which may not have had the desired effects.

As the monetary authority, the Monetary Policy Committee (MPC) laid a triple objective of mitigating negative effects of the virus, reviving growth and preserving financial stability. To ease economic hardship while keeping inflation in check, the RBI slashed interest rates keeping the policy repo rate at a low of 4%. The cash reserve ratio (CRR) was lowered, which provided additional liquidity to help aid banking system. The goal was to ensure that no part of the financial system faced liquidity concerns or credit constraints.

To tide over the pandemic, it was paramount for government and the central bank policies to work in tandem. To ensure that governments did not have to cut their spending due to shortfalls in revenue, RBI needed to enable both central and state government to borrow adequately in debt markets. As a banker to the central and state governments, the limit on ways and means advances for both central and state government were increased. Aside from this, through open market operations, RBI purchased about 30% of central government’s net market borrowings in FY 2021 and has committed to continue to purchase substantial amounts in FY 2022 through the G-sec Acquisition Programme. Special OMOs – through Operation Twist (OT) involving the simultaneous purchasing of long-term government securities and selling corresponding short-term securities of similar amounts in a liquidity neutral fashion, have lowered long-term yield and smoothened the curve. The Reserve Bank was successful in managing the large government borrowing in FY 2021 at a weighted average borrowing cost for the central government, at just 5.79%, the lowest in 16 years.

As regulator of the banking system, it is crucial that the interests of both borrowers and lenders are aligned to ensure stability of the financial system. A host of measures were put in place to help in the continued smooth functioning of financial intermediaries including banks and NBFCs. On the one hand, these policy measures were aimed at protecting and helping borrowers in this time of economic and financial stress brought on by the pandemic and the consequent lockdowns. On the other hand, measures were also put in place to provide regulatory relief to financial intermediaries in terms of their access to liquidity and regulatory forbearance to protect their balance sheets. The overall aim was to keep credit flowing despite all the disruptions being experienced by the economy and financial markets.

Overall, the RBI, in cooperation with the Government of India, has succeeded in achieving its broad objective of keeping financial intermediaries, financial markets and the financial system as a whole sound, liquid, and functioning smoothly. It has maintained financial stability despite initial conditions of the Indian financial intermediaries being stressed as a consequence of legacy problems. But very significant challenges remain as this crisis unfolds further in both India and the rest of the world. It has also protected households as well as small and large businesses from experiencing acute financial stress for the time being, but stresses will emerge once regulatory forbearance is lifted.

Transmission of the highly accommodative monetary policy, and the corresponding liquidity management, has been largely successful. Interest rates have fallen across the board and g-sec yields are at almost record lows, with most real interest rates now being in negative territory. However, the RBI’s liquidity injection has been so large that there was an almost consistent systemic liquidity surplus of about Rs 6 trillion (about 3% of GDP) that needed to be absorbed by the RBI on a daily basis.

However, despite all the measures implemented to promote the flow of credit to all segments of the market, credit growth has continued to be sluggish except for a significant increase to the SMSE sector. Hence there is a mismatch between the performance of the real sector and financial markets. This could potentially lead to enhanced stresses experienced by both lenders and borrowers, leading to potential financial instability. Thus, financial stability challenges remain for the Indian financial system and its regulator in the months to come.

India responded to Covid-19 as soon as it was becoming clear that a pandemic was in the offing. Although there were only 500 confirmed cases at that time, the government imposed a sudden nationwide total lockdown on March 25, 2020. This lasted until end of May 2020 and was then lifted in phases subsequently. In the words of the government’s official Economic Survey, “India focused on saving lives and livelihoods by its willingness to take short-term pain for long-term gain” (Government of India 2021: 1). The short-term pain was indeed palpable, with GDP estimated to have contracted by 24.4 % year-on-year in Q1 FY 2021,[1] followed by a further contraction of 7.3 % year-on-year in Q2, and a faint recovery of 0.4 % year-on-year in Q3. The full FY 2020–21 GDP is estimated to have contracted by 8.0%, which has come on top of an ongoing economic slowdown over the previous eight quarters or so. The current expectation of most forecasters is that the Indian economy will stage a robust recovery and grow by 10–12.5% in FY 22.[2] Thus, overall, the economic cost of Covid-19 will be around two years of GDP growth and as yet indeterminate losses in employment and livelihoods.

In terms of lives, India has fared much better than the West, with about 120 deaths per million and fewer than 9,000 cases per million (as of March 31, 2021),[3] compared with the United States recording around 1,700 deaths per million and over 90,000 cases per million. However, the Indian record is a not as good as that of much of Asia, and similar but slightly worse than the rest of South Asia. Given the low levels of income in the country and high density of settlements, both urban and rural, India has been lucky to have not experienced a worse disease outcome. Looking to the future, possessing the highest vaccine production capacity in the world, India is potentially well-placed to implement a successful mass vaccination programme by the end of 2021, but the speed of vaccinations has faltered. So this will need more urgent and faster systematic implementation in light of the new wave now being experienced by India (in mid-April 2021).

The policy response to the economic impact of both the pandemic and the consequent lockdown was the usual mix of fiscal, monetary and financial measures, but relatively light on fiscal measures, which were largely focused on cushioning the impact on the poor and on tiny and small businesses. “This included direct food transfers to the poor and vulnerable, livelihood programmes, guarantees and liquidity enhancing measures” (Government of India 2021: 20). The additional fiscal stimulus was in the range of only about 2–2.5 % of GDP, which is at the lower end of the spectrum for emerging market economies (EMEs). The government of India has been very mindful of the need to preserve its fiscal firepower in view of its already extended fiscal situation,[4] and the uncertainty surrounding the length of time that the pandemic will affect the world and India. Consequently, much of the burden of policy measures has rested on active cooperation between the government and the Reserve Bank of India (RBI) in ensuring that the economy and the financial system remained stable and liquid. They have largely succeeded in achieving this broad objective, at least in the short term: financial markets have exhibited significant stability, with no lack of liquidity, inflation has been range bound between 4.1 % and 7.6 % over the year,[5] and financial institutions have remained viable as a consequence of the various policy measures taken.

This paper focuses on the specific measures taken by the Reserve Bank in this context.

At the beginning of the pandemic, starting in March 2020, as lockdowns spread across the world, the expectations of the RBI, along with most other leading central banks, were of a severe economic dislocation, the possible freezing of financial markets, widespread suffering of households and businesses, with their inevitable impact on financial intermediaries, along with a severe downturn in global trade. Judging from previous experience, emerging markets, including India, also faced the spectre of capital outflow with its associated impact on asset price volatility and financial stability. As the initial severe lockdowns had their expected economic impact, including in India, the negative economic expectations were reinforced by indices such as the global manufacturing Purchasing Managers Index (PMI) exhibiting its lowest level in April 2020 since 2008– 09, along with the services PMI being at its lowest level ever, and global trade was falling substantially.

With the experience of the 2008–09 North Atlantic Financial Crisis (NAFC) still relatively fresh in the minds of macro managers, fiscal and monetary authorities, along with financial regulators, were ready to use all instruments at their command to avert the then expected financial and economic disaster. Central banks, in particular, were well equipped to pull out all the stops.

In India, with the possibility of a relatively constrained fiscal response, the RBI had to do much of the heavy lifting. The RBI is a full-service central bank as the monetary authority, lead financial system regulator and supervisor of financial intermediaries, banker to and debt manager of the central and state governments, currency issuer and manager, and regulator and operator of the payment and settlement system. Its policy actions since February 2020 have therefore encompassed all these areas and have had the benefit of being coordinated. It has carried out more policy actions than any other EME central banks (Cantu et al. 2021)

A perusal of the various documents issued by the RBI since February 2020 provides the broad objectives that it desired to achieve through its policy measures. Its multiple objectives included:

- Minimise the adverse macroeconomic impact of the Covid-19 pandemic and the associated lockdowns

- Enhance effective transmission of monetary policy

- Ensure smooth and seamless transmission of monetary policy impulses

- Preserve financial stability

- Prevent financial markets from freezing up

- Maintain orderly functioning of financial markets and financial institutions

- Provision of adequate system level as well as targeted liquidity

- Keep the financial system and financial markets sound, liquid and smoothly functioning so that finance keeps flowing to all stakeholders

- Ensure normal functioning of financial intermediaries to facilitate flow of funds at affordable rates and rekindle investment impulses

- Sustain bank credit flows on easy terms

- Ensure access to finance for all, especially the sectors which were hit the hardest

- Ease financial strains on both households and businesses

- Facilitate trade, both exports and imports, through easy availability of credit and payment services

- Facilitate the completion of the enhanced market borrowing programmes of both the central and state governments in a non-disruptive manner

- Ensure an orderly evolution of the yield curve

- Ensure the orderly and smooth functioning of the payment and settlement systems, at both retail and wholesale levels

- Maintain smooth and regular flow of currency across the country

- Facilitate the completion of the enhanced market borrowing programmes of both the central and state governments in a non-disruptive manner

- Prevent financial markets from freezing up

In accordance with these objectives, in cooperation with the government, the RBI implemented a plethora of policy changes throughout the year starting in March 2020. Some were at a general, macro level, while some others were at a micro level and detailed. An almost full chronology is provided in the table in the Annex. They can be grouped into four broad categories, though some were not easy to classify:

- Monetary policy

- Liquidity management and special credit facilities

- Fiscal cooperation

- Regulatory measures

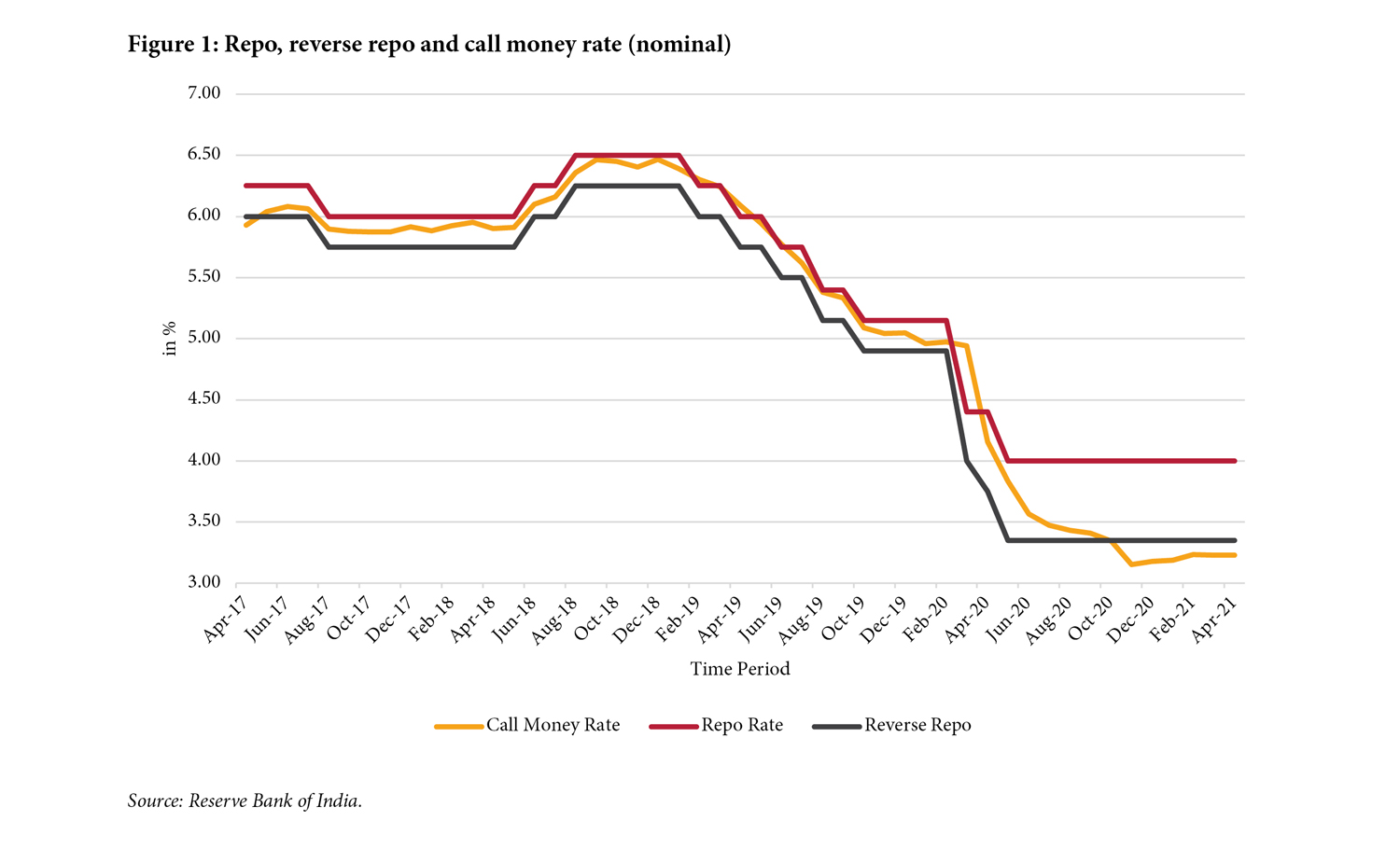

The Reserve Bank is a ‘flexible inflation targetter’[6] and its operational monetary policy signalling rate is the repo rate – the rate at which it lends to commercial banks on a collateralised basis through its Liquidity Adjustment Facility (LAF). The operating target of monetary policy is the weighted average call rate (WACR), which reflects the rate at which transactions are conducted in the unsecured segment of the overnight money market. The LAF attempts to maintain an interest-rate corridor between the interest rate of the Marginal Standing Facility (MSF) as the upper bound, and the fixed reverse repo rate as the lower bound, with the policy repo rate in between (RBI 2021c: 122). The fixed rate reverse repo and MSF of overnight tenor are conducted every day between 9am and midnight. The 14-day variable rate repo/reverse repo is conducted on a fortnightly basis based on assessment of liquidity conditions by the Reserve Bank.[7] The objective of the liquidity operations is to align the WACR with the repo rate. Prior to Covid, the LAF interest-rate corridor was kept relatively narrow at 50 basis points.

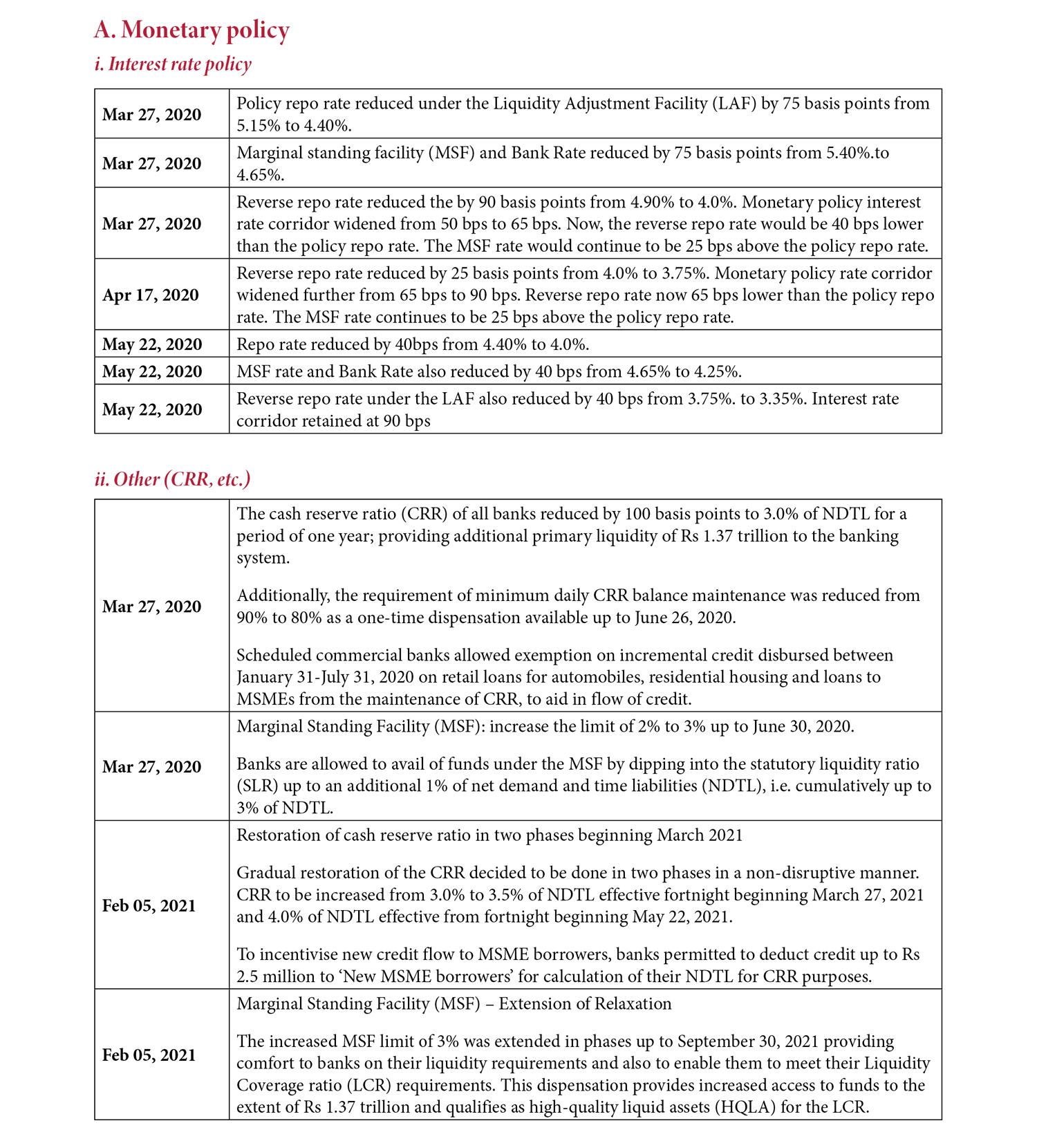

The RBI acted very quickly in March 2020 and convened the Monetary Policy Committee (MPC) on March 24, a week earlier than its previously scheduled date. The decisions taken were intended to “(a) mitigate the negative effects of the virus; (b) the revive growth; and above all, (c) preserve financial stability” (RBI 2020a). Starting from the aggressive policy actions taken in this meeting, the RBI reduced the policy repo rate from 5.15% to 4.0% over the year. This was done in two stages: first a reduction of 75 basis points to 4.40% on March 27, 2020 and then another 40 basis points on May 22, 2020. The rate has been stable since then. Correspondingly, the MSF rate has been reduced from 5.40% to 4.25%, and the reverse repo rate somewhat more by 155 basis points from 4.9% to 3.35%. Thus, the monetary policy interest-rate corridor has been expanded significantly from 50 basis points to 90 basis points (Figure 1). Although inflation was higher than the RBI’s tolerance band through much of 2020, it is now back within the policy range.

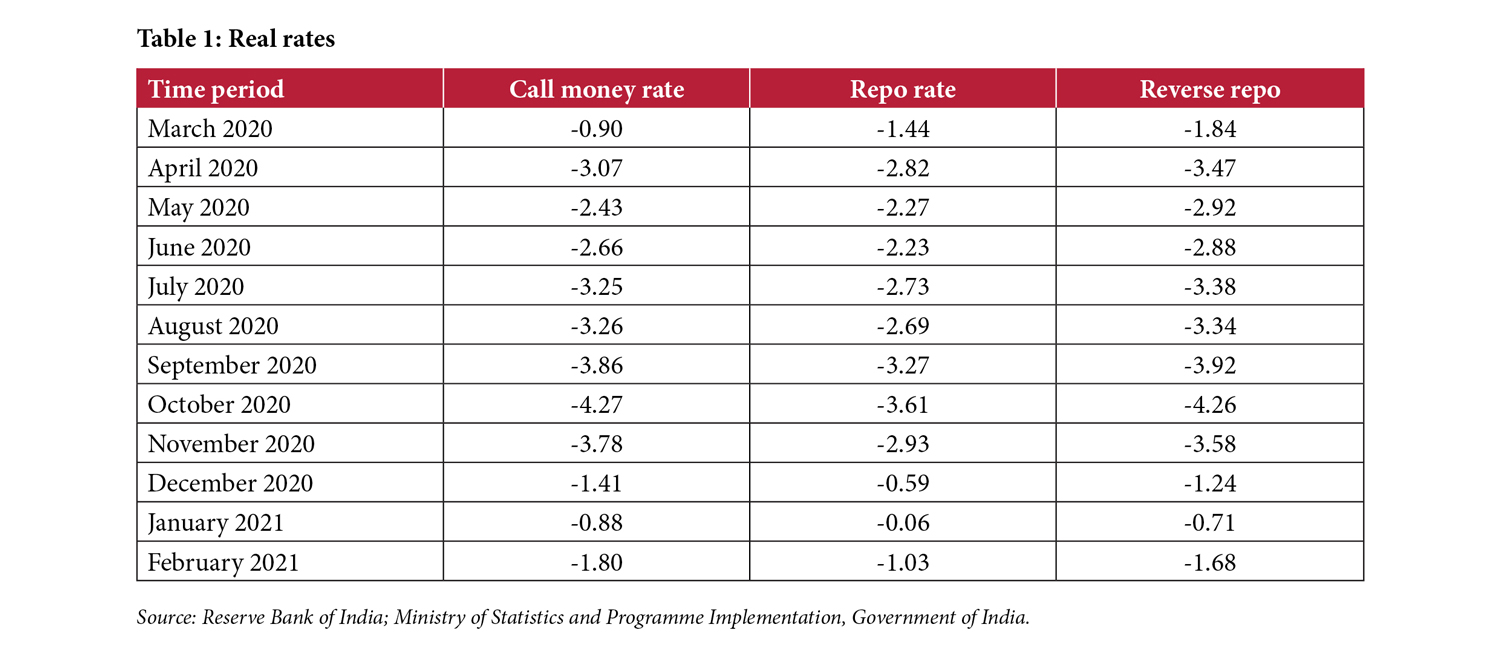

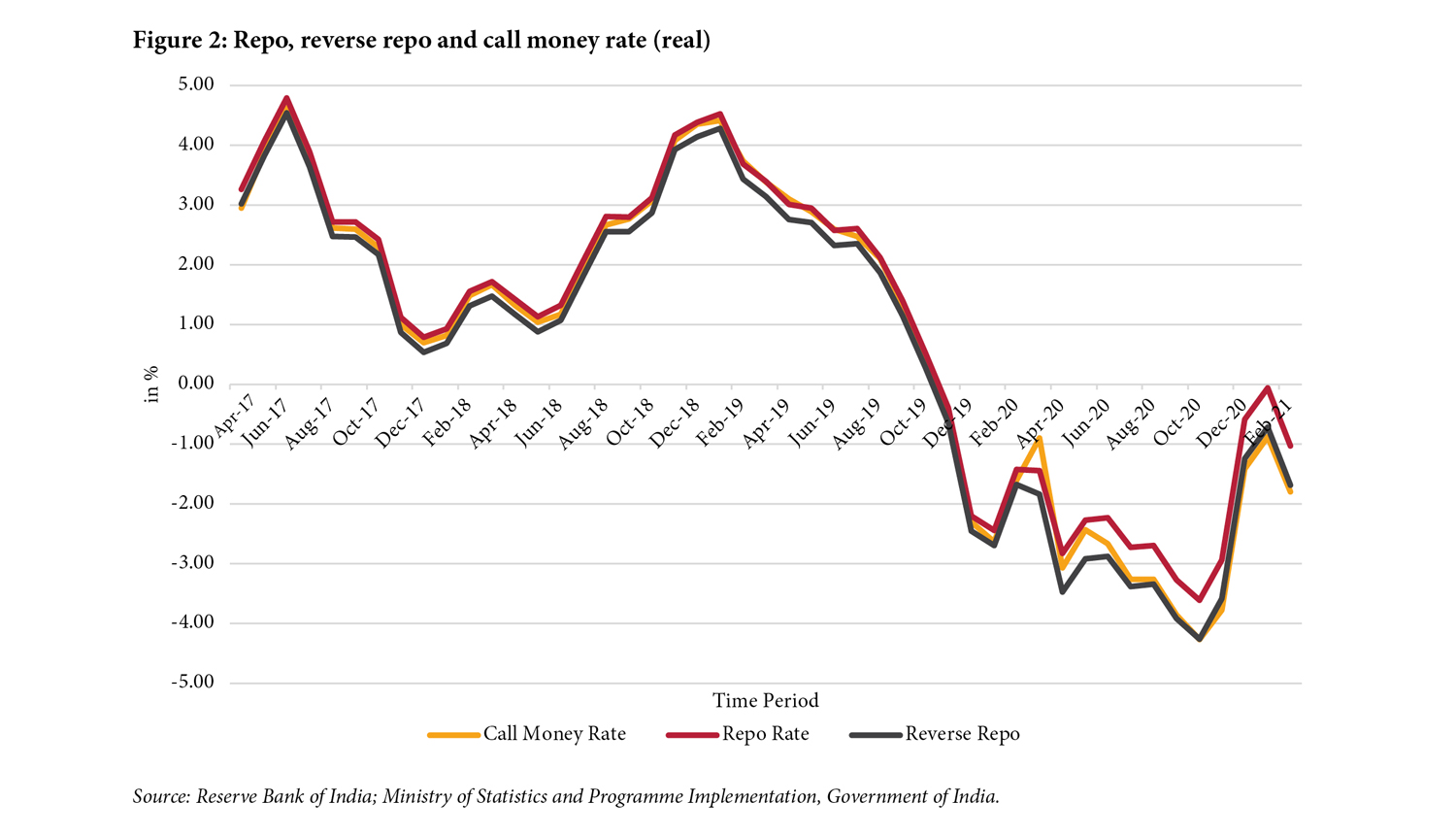

Although the RBI is some distance away from nominal negative rates, its real policy rates were in negative territory through much of 2020 and beyond because of elevated inflation levels. This has been transmitted to both bank deposit and lending rates, and the money market target rates (WACR) as well. The real yield on risk-free ten-year government securities were also negative through much of 2020. Thus, in view of the relatively higher inflation rates prevalent in India (and other EMEs), while the central bank has not had to resort to nominal negative policy rates, its highly accommodative monetary policy has indeed resulted in significant real negative rates (Figure 2 and Table 1).

Going forward, the RBI will need to constantly assess the consequences of such a prolonged period of real negative interest rates and high liquidity provision on inflation and financial stability; on household savings;[9] and possible bursting of asset bubbles. It should be of interest to compare the magnitude of real policy rates between advanced and emerging market economies, and their consequences as they unfold.

Forward guidance

For the first time, perhaps, the RBI engaged in some degree of forward guidance. “FG gained prominence in the Reserve Bank’s communication strategy to support the accommodative stance of the Monetary Policy Committee (MPC)” (RBI 2021d: 48). The nature of this forward guidance was repeated assurance to financial markets that the policy stance would remain accommodative until the revival of growth. As announced by the MPC in October 2020, it would “continue with the accommodative stance as long as necessary – at least during the current financial year and into the next financial year – to revive growth on a durable basis and mitigate the impact of Covid-19 on the economy while ensuring that inflation remains within the target going forward” (RBI 2021d: 48). The accommodative stance continued in the recent MPC meeting held in April 2021, with a stronger assurance that the RBI will do “whatever it takes”[10] in the wake of continued Covid threats. Repeated assurances have also been given that the RBI would maintain comfortable liquidity conditions, financial stability and an orderly yield curve. These statements have been interpreted by the RBI as constituting “explicit time contingent and state contingent forward guidance” (RBI 2021d: 51), even though they are perhaps not as explicit as the forward guidance employed by some other advanced economy central banks. Since real GDP growth is expected to recover to 10%+ levels in FY 2022, this forward guidance can be interpreted to be somewhat ambiguous.

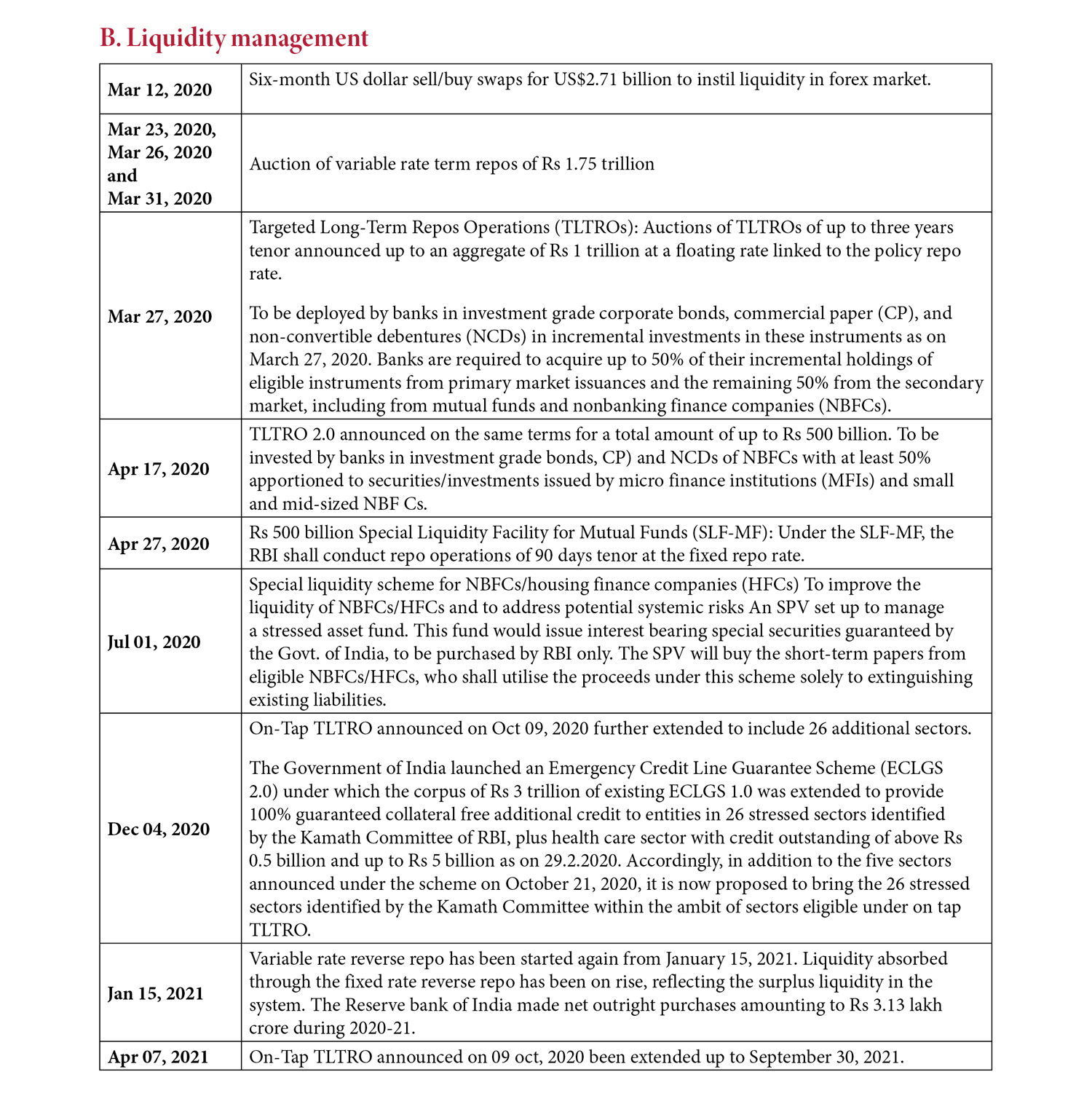

As already mentioned, the RBI performs active liquidity management on a daily basis through the operations of the LAF. These operations were enhanced significantly through the introduction of long-term repo operations (LTROs) in February/March 2020 for one year and three-year tenors “to support monetary transmission and augment credit flows to productive sectors” (RBI 2020e: 69), similar to the operations by the European Central Bank (ECB). Since the rate was linked to the policy repo rate, these resources were available to banks at a rate lower than prevailing market rates as well as banks’ own deposit costs. This was designed to facilitate monetary policy transmission and to support credit offtake. LTRO auctions were held amounting to Rs 1.25 trillion. As market rates went down over time, almost all the funds were returned to the RBI by September 2020.

Further liquidity facilities were provided through two targeted long-term repo operations (TLTRO 1.0 and 2.0) of up to three years tenor at the floating rate linked to the policy repo rate. Lending through this facility was targeted for banks to invest in specified instruments such as investment-grade corporate bonds, commercial paper (CP) and the like. The introduction of this facility was a response to some tightening observed in financial conditions consequent to sell-off pressures in financial markets arising from the initial reactions to the outbreak of the pandemic. TLTRO facilities were therefore designed to address the “sharp spikes in risk premium on corporate bonds, CPs and debentures dried up trading activity resulting in market liquidity” (RBI 2021d: 47). Subsequent TLTROs were introduced to provide relief to the small and mid-sized corporates, non-bank financial institutions (NBFCs), and micro finance institutions (MFIs). Later, in October 2020, the TLTRO facility was made on an on-tap basis up to end-March 2021; and in December 2020 an additional 26 sectors adjudged to be “stressed sectors” were made eligible to receive funds under the scheme. Investments made by banks under this facility can be classified as held to maturity (HTM) even above the 25% of total investment permitted to be included in the HTM portfolio. Four TLTRO auctions were held initially amounting to just over Rs 1 trillion. TLTRO 2.0 attracted lukewarm demand in view of ample liquidity in the system. TLTRO 2.0 has been extended till September 2021 at a recently held MPC meeting in April 2021.

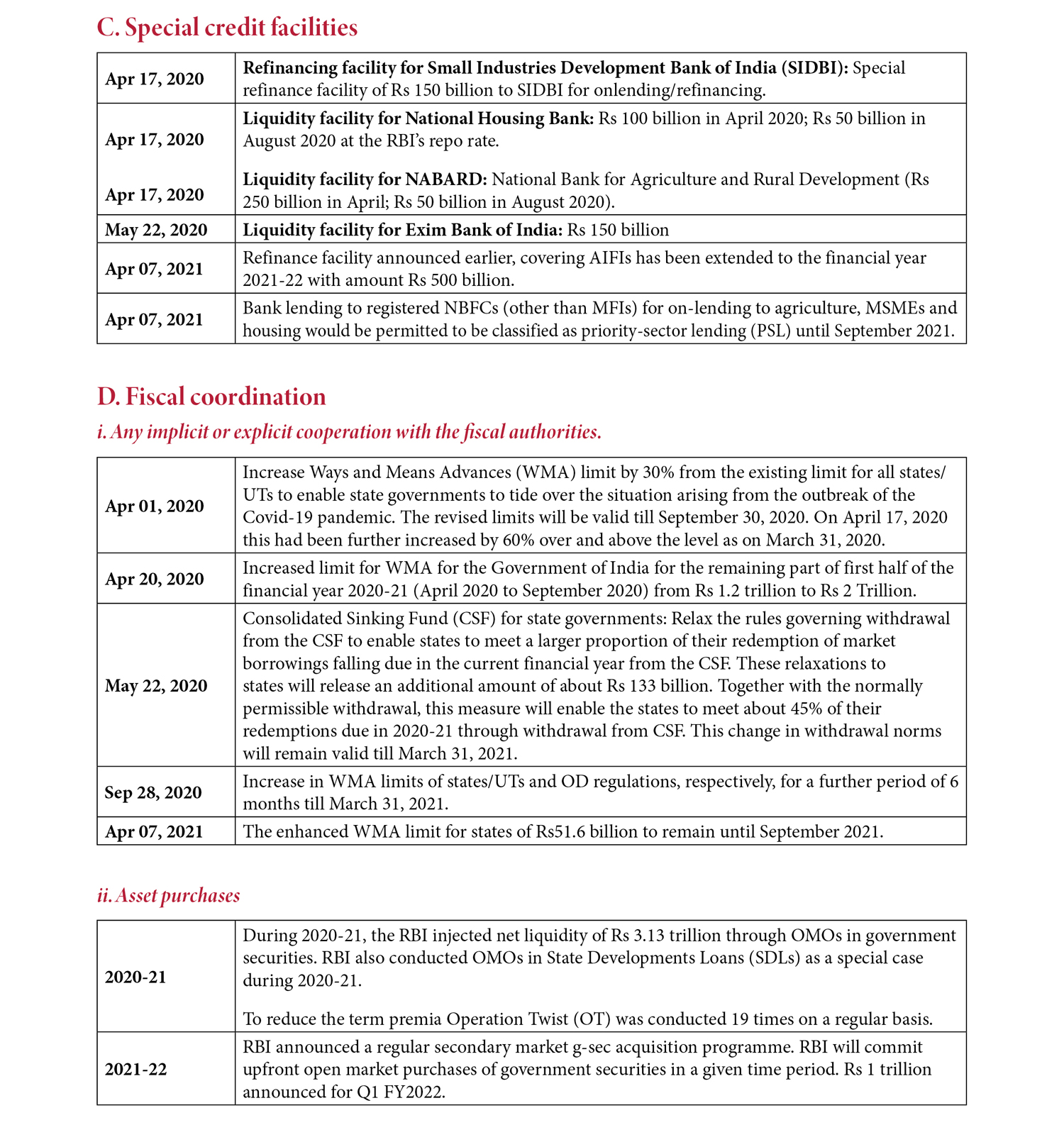

India has a number of sectoral development finance institutions: the Small Industries Development Bank of India (SIDBI), the National Housing Bank (NHB), the National Bank for Agriculture and Rural Development (NABARD) and the Export–Import Bank (EXIM Bank). Special refinancing facilities were provided at the policy repo rate to each of these institutions, amounting to an aggregate of Rs 750 billion, to relieve their liquidity stress and to enable them to extend credit at low rates in their respective sectors. Less than half of the potential liquidity provided has been used. This facility has been extended for the financial year 2021-22 with Rs 500 billion.

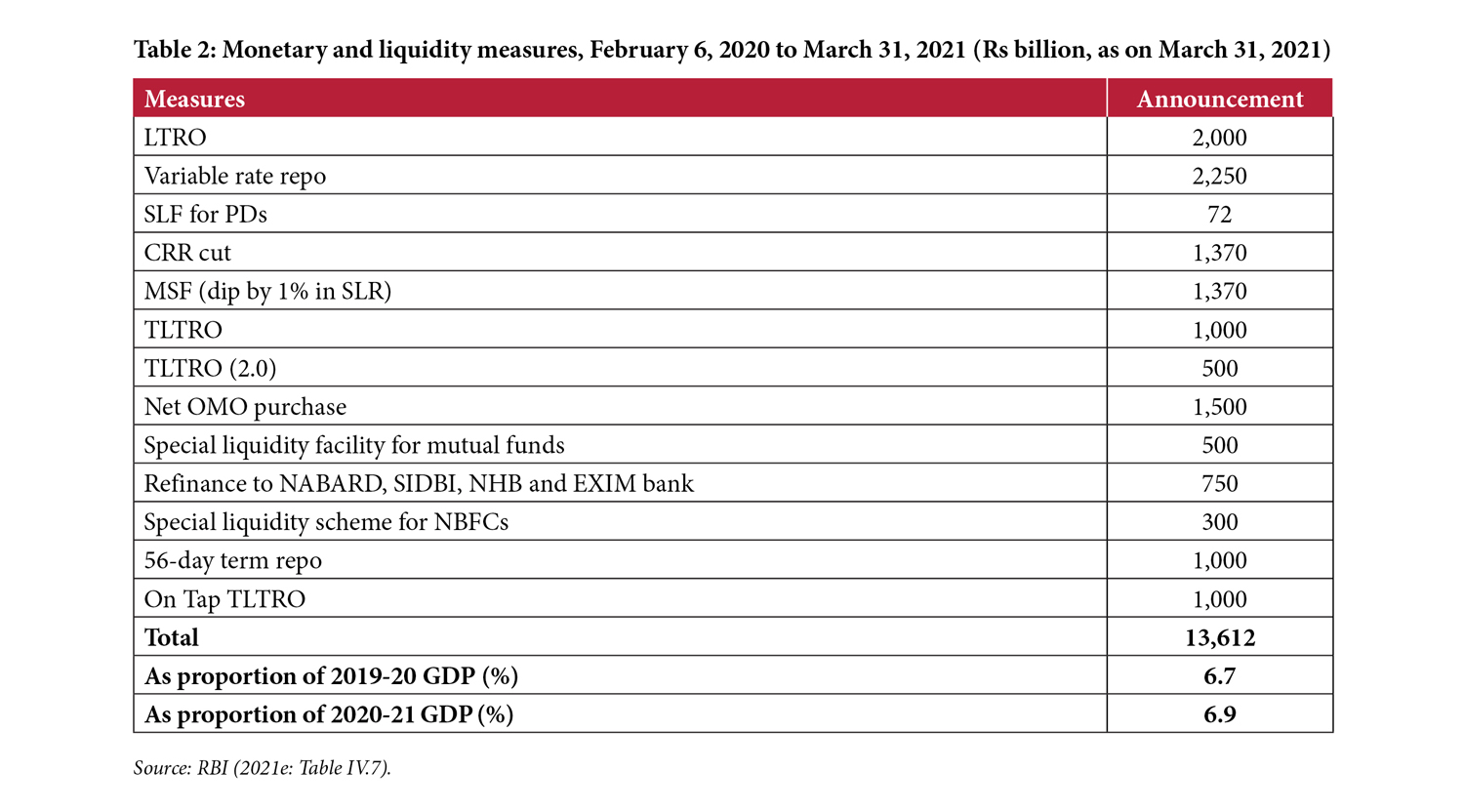

The overall objective therefore was to make sure that no part of the financial system faced any difficulty in accessing funds during this whole Covid period. The total potential liquidity injection amounted to Rs 13.6 trillion, about 6.9% of GDP, by March 31, 2021 (Table 2). The liquidity operations were a combination of market liquidity provisions supplemented by targeted ones in terms of both specified instruments and sectors.

Ways and means advances

As their banker, the Reserve Bank of India provides a facility of Ways and Means Advances (WMA) to the government of India and to state governments to help them tide over temporary mismatches in the cash flow of their receipts and payments. These advances are usually given at 2% above the repo rate, up to a specified limit announced every six months, and are repayable in each case in 90 days. In other words, this is an overdraft facility available to both the central and state governments.

In view of the nationwide lockdown imposed in late March 2020 and the consequent disruption in financial markets and in tax receipts, the WMA limit for the central government was increased from the initial Rs 1.2 trillion to Rs 2 trillion for the first half of FY 2021. The corresponding limit for the first half of FY 2020 had been Rs 750 billion.

Similarly, the limit for state governments was increased in stages by 60%, and extended to the second half of FY 2021. These measures did much to reduce the cash flow problems then being faced by both the central and state governments.

Asset purchases

The Reserve Bank is the debt manager for both the central and state governments. In principle, it acts as the front and back office of a conventional government debt office. The Ministry of Finance itself is formally the middle office. Since 2003, after the enactment of the Fiscal Responsibility and Budget Management Act, the RBI is no longer allowed by law to participate in the government securities primary market, except in very exceptional circumstances. Although some countries did choose this route as a consequence of Covid-induced fiscal stresses, and despite many pressures, the government of India and the RBI eschewed that route for financing the much-increased borrowing requirements of the government.

The RBI did, however, maintain an active programme of asset purchases of government securities in the secondary market through its open market operations (OMOs) amounting to about Rs 3.13 trillion, about 1.5% of GDP, through FY 2021. This accounted for about 30% of the central government’s total net market borrowings of about Rs 10.5 trillion. The RBI does not normally conduct OMOs in state government securities (known as State Development Loans, or SDLs). Because of the increased risk perception due to Covid, yields on SDLs started rising, so the RBI has also been conducting special OMOs in SDLs in order to help the state government market borrowing programmes and to constrain market SDL yields from rising.

In April 2021, the RBI put in place a secondary market government security (G-sec) acquisition programme (GSAP) with an upfront commitment to a specific amount of open market purchases of government securities to enable a stable and orderly evolution of the yield curve amidst comfortable liquidity conditions.

Operation twist

Starting in December 2019, and continuing to the present, the RBI has been conducting special OMOs—through Operation Twist (OT)—involving the simultaneous purchasing of long-term government securities and selling corresponding short-term securities of similar amounts in a liquidity neutral fashion. “These operations were aimed at compressing the term premium and reducing the steepness of the yield curve. Moderation in the long-term risk free (g-sec) rates, in turn, gets reflected in other financial market instruments that are priced off the g-sec rate, thereby improving monetary transmission” (RBI 2021d: 48). The RBI conducted 19 such operations, usually of Rs 100 billion each, during 2020-21, amounting to a total of just over Rs 2 trillion.

As a consequence of all these measures, and as the debt manager of the government, the RBI succeeded in managing the highest ever level of the government’s market borrowing programme. The weighted average borrowing cost for the central government, at 5.79% during 2020-21, was at a 16-year low. The comparable cost in the previous year was 6.84%. The weighted average maturity of the stock of public debt is also at its highest level ever (RBI 2020i).

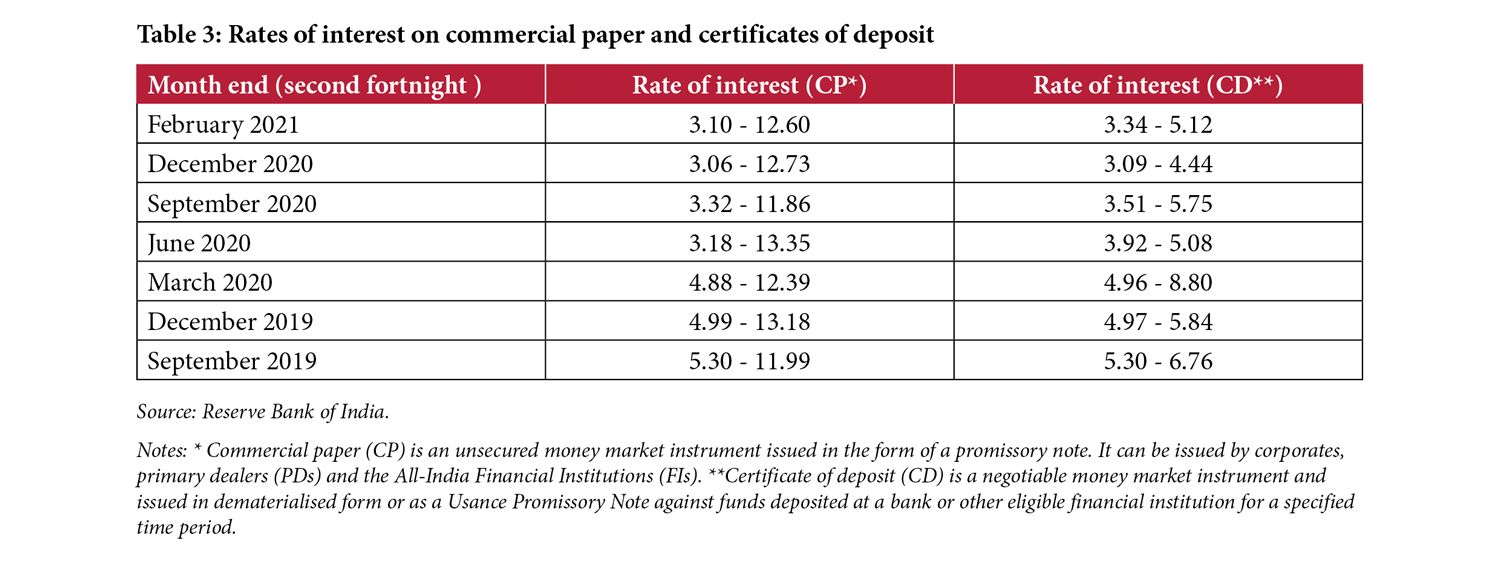

Corporate bond spreads also narrowed considerably across the maturity spectrum and rating categories and have reached pre-Covid levels. Moreover, in view of the lower rates, corporate bond issuance in the April to February period of FY 2021 exceeded that in the previous year’s comparable period by about 20%. The reduction in rates was across the board in all financial markets, including other instruments such as commercial paper (Table 3). This could give rise to financial stability issues if there is an increase in bond defaults consequent to lower-than-expected economic recovery.

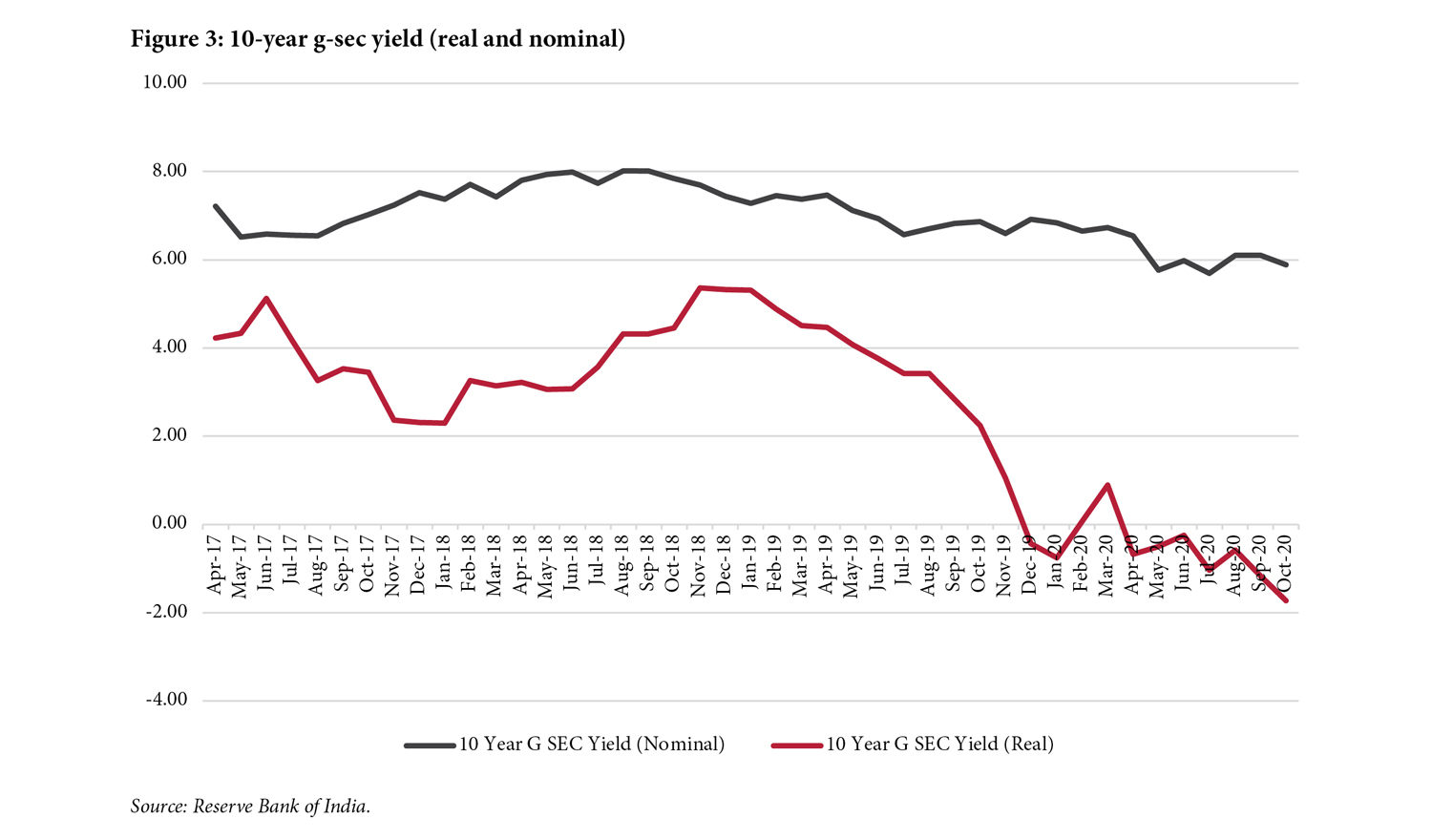

Overall, although the RBI avoided direct funding of the substantially enhanced fiscal deficits of both the central and state governments, its multiple actions—encompassing much increased Ways and Means Advances, large asset purchases, a sizeable Operation Twist programme and occasional devolvement of bond auctions on primary dealers—amounted to substantial cooperation with the fiscal authorities. Its objective was clearly to successfully manage the government’s very large market borrowing programme while keeping borrowing costs low. The yield on ten-year g-secs was 6.5% at the beginning of FY 2021 and ended the fiscal year (March 2021) at 6.18%, averaging just under 6% (See Figure 3).The moderation of interest rates across the whole yield curve, including in particular the long-term rates, reduced the cost of borrowing for the government substantially. “Moderation of long term rates, in turn, softened interest rates across the spectrum of instruments and issuer category, which rekindled market activity and restored normalcy while maintaining financial stability”. (RBI 2021d: 50). This operation was made much easier thanks to the RBI’s role as debt manager of the government.

The possibility of increasing inflation in both India and the rest of the world, leading to potential hardening of US Treasury yields, will clearly challenge the RBI’s yield control objectives in the coming months.

Along with the extensive measures enacted by the RBI in terms of monetary policy, liquidity management and fiscal cooperation, a host of measures were put in place to help in the continued smooth functioning of financial intermediaries including banks and NBFCs. On the one hand, these policy measures were aimed at protecting and helping borrowers in this time of economic and financial stress brought on by the pandemic and the consequent lockdowns. On the other hand, measures were also put in place to provide regulatory relief to financial intermediaries in terms of their access to liquidity and regulatory forbearance to protect their balance sheets. The overall aim was to keep credit flowing despite all the disruptions being experienced by the economy and financial markets.

“These policy actions, which in the initial phase of pandemic, were geared towards restoring normal functioning and mitigating stress, are now getting increasingly oriented towards supporting the recovery and preserving the solvency of businesses and households” (RBI 2021a: 1). The emphasis now is to help the financial system to return to some degree of normalcy, while aiding the most affected sectors to recover from the crisis.

Credit enhancement measures

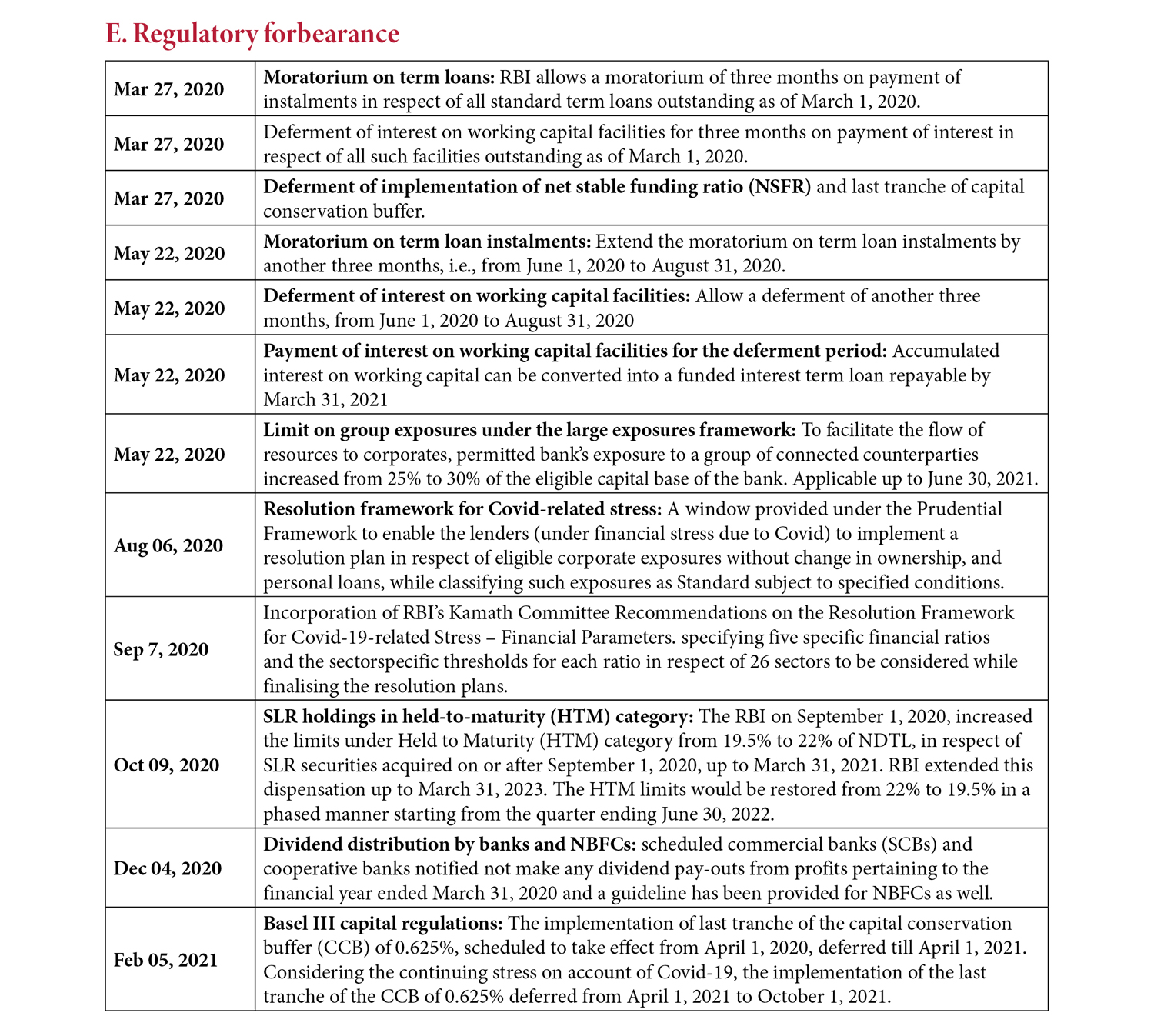

Taking cognisance of the total and sudden lockdown imposed by the government, right at the outset the RBI put in place a moratorium on the payment of instalments on all term loans that were standard prior to Covid. Similarly, payment of interest on working capital facilities was also deferred – banks were allowed to turn these into term loans. These measures were designed to provide temporary relief to borrowers facing liquidity stress due to the pandemic and also to provide banks with flexibility to deal with such borrowers.

Initially these moratoriums were allowed for a period of three months and then extended until August 31, 2020. The cessation of the moratoriums was stayed by the Supreme Court of India in early September. That stay has now been lifted in late March 2021, so the non-payment of instalments between September 2020 and now is in a state of limbo. Whereas regulatory forbearance was given to the banks for non-payment of instalments by borrowers during the moratorium, they will now[11] have to be classified as per the income recognition and asset classification norms after August 31. The Supreme Court has also prohibited the charging of interest on interest during the moratorium period.

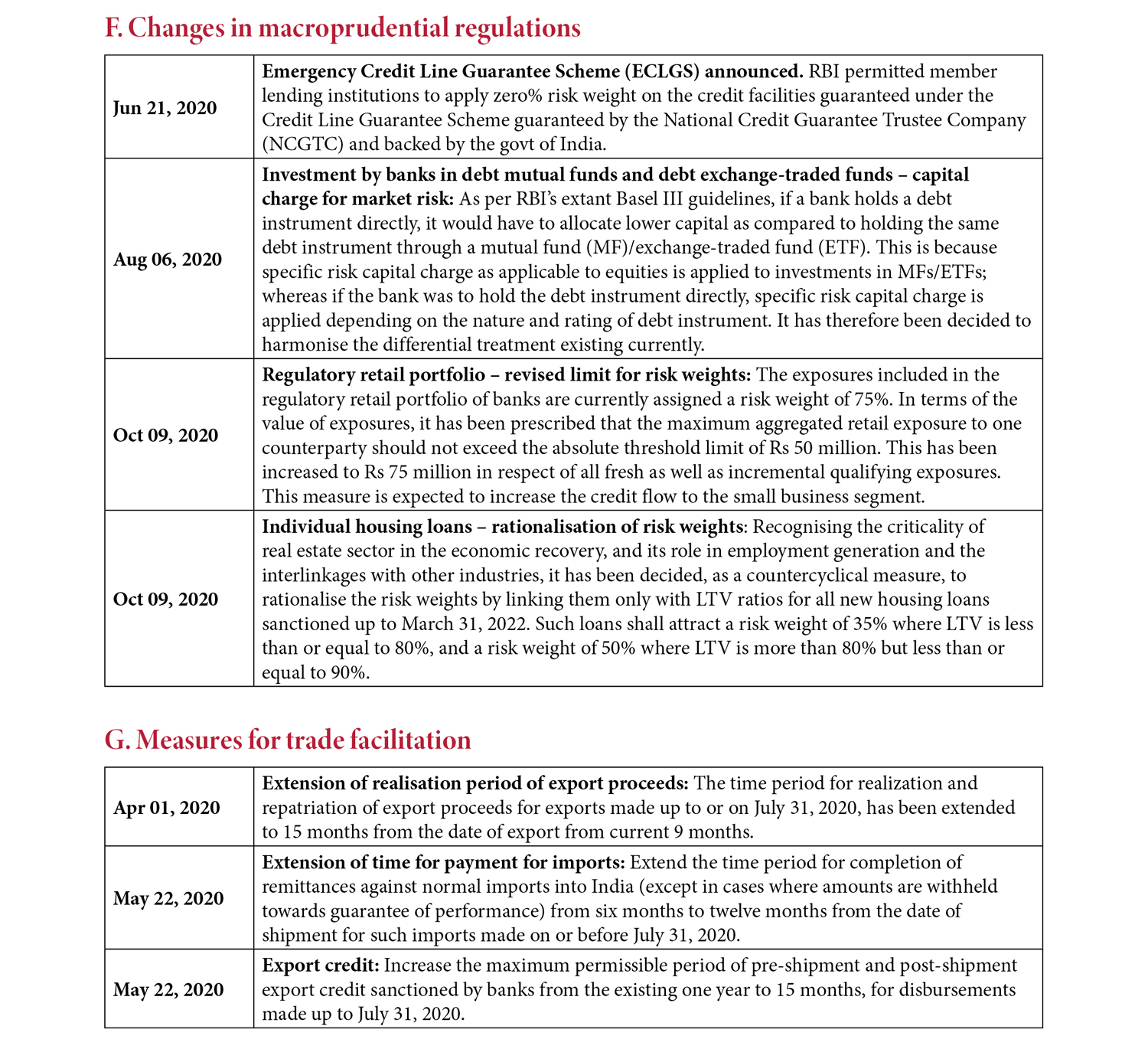

A number of measures were also enacted to promote the extension of credit to micro, small and medium-sized enterprises (MSMEs). These include the extension of credit guarantees from the government to financial intermediaries for MSME lending,[12] some regulatory forbearance on classification of MSME stressed assets, and macroprudential regulations related to risk rates on MSME loans. There has been a general perception that MSMEs have been hit harder by the Covid crisis; hence these special measures to keep credit flowing to them.

In order to protect banks from excessive concentration of risk in exposure to a group of connected borrowers, the RBI places limits on such exposures. The existing limit was 25% of the eligible capital base of the bank. In view of difficulties faced by some large borrowers in accessing credit, this limit was raised to 30% to facilitate the flow of resources to such large corporate entities.

In order to preserve bank capital to encourage credit flow banks have been prohibited from giving any dividend payouts to the shareholders for FY 2020.

Regulatory forbearance

It was expected that the unfolding of the pandemic and its associated economic impact on the overall macroeconomic environment would have a negative effect on the asset quality, capital adequacy and profitability of financial intermediaries, including banks. The unprecedented injection of abundant liquidity into the system, accompanied by the lowering of interest rates, helped to cushion financial institutions from the worst impact of the crisis. It was also felt necessary to buttress these systemic measures with corresponding regulatory forbearance. The general principle governing the new forbearance measures was that they would apply only to new stressed assets arising on account of Covid, and not to the legacy nonperforming assets (NPAs).

The Indian banking system has been under significant stress due to the accumulation of a large amount of NPAs over the last decade or so. Various policies and measures have been put in place for the resolution of these stressed assets over the last five years or so. The RBI had introduced a principle-based resolution framework for addressing borrower defaults under a normal scenario in June 2019 (RBI 2019). The outbreak of the pandemic led to new fears over the appearance of a significant financial stress among a number of borrowers who otherwise had a good track record, which could then lead to difficulties in their long-term viability. This could give rise to new financial stability risks.

The RBI felt that it would be helpful to allow lenders to implement resolution plans for such borrowers while keeping their loans in standard classification. It has therefore introduced a new resolution framework for such borrowers, “with the intent to facilitate revival of real sector activities and mitigate the impact on the ultimate borrowers” (RBI 2020d: 3). Covid-related stressed sectors were then identified for eligibility for the scheme by an RBI committee (RBI 2020h). These resolution plans are also available to NBFCs in addition to commercial banks. Forbearance was also extended through another scheme for restructuring needed by MSME borrowers facing stress the pandemic.

The RBI mandates a ‘statutory liquidity ratio’ (SLR) by which commercial banks have to hold a minimum percentage of their assets in government securities. This ratio is currently mandated to be 18% of their NDTL. Securities held under this mandate are given ‘held- to-maturity’ (HTM) status, protecting banks from losses that could occur from market- to-market valuation arising from increases in yields. In view of the enhanced government market borrowing programme, the HTM ratio has been increased from 19.5% of NDTL to 22%, allowing banks to hold a larger proportion of government securities while shielding them from potential losses leading to financial stability risks. In fact, however, banks’ portfolios of government securities now amount to about 30% of NDTL, thereby placing them under significant risk in the event of g-sec market yields rising.

The implementation of the last tranche of 0.625% of the capital conservation buffer (CCB) was scheduled to take effect from April 2020. This was first deferred to April 2021, and then again to October 2021, in order to “aid in the recovery process” from Covid-induced stress (RBI 2021b).

Macroprudential measures

In the couple of years preceding the 2008-09 North Atlantic Financial Crisis (NAFC), the RBI had undertaken various macroprudential measures in the interest of preserving financial stability. Having had this positive experience, the RBI has once again put in place a few macroprudential measures in the light of Covid.

As prescribed by existing Basel III guidelines, differential risk capital charges are applied to debt instruments held by banks directly that are lower than those applied to similar instruments held indirectly through mutual funds, since the latter are seen to have an equity element. These risk capital charges have now been harmonised with the expectation of helping the operation of the bond market (RBI 2020f).

Under Basel guidelines, a bank’s aggregate exposures included in retail portfolios attract a lower risk weight of 75% as long as individual exposures do not exceed a specified relatively low limit. This measure helps in reducing the cost of credit to individuals and small businesses. As part of the overall strategy of enhancing the flow of credit to MSMEs, the RBI has increased the limit of aggregate exposures from Rs 500 million to Rs 750 million (RBI 2020f).

In previous episodes of potential financial instability, macroprudential measures were used to curb housing finance through the counter-cyclical increase in risk weights applicable to certain categories of housing loans. In the current situation, however, retail investment in housing has suffered a downturn following lockdowns and other Covid- induced economic disruptions. The RBI has therefore tweaked risk weights to make them more favourable for certain categories of housing loans depending on specified loan-to-value (LTV) ratios, in order to ease bank lending for housing (RBI 2020f).

The Bank for International Settlements (BIS) has compiled a database on central banks’ monetary responses to Covid-19. A perusal of the database shows that the RBI has used most of the tools and measures listed except for the purchase of private sector assets (Cantu et al. 2021: Table 1). Policy intervention by the RBI can be evaluated as relatively comprehensive and broad-based. Just like other central banks, its skills in managing such a crisis had been honed during the NAFC in 2008-09. While, unlike advanced economy central banks, it did not have to practice unconventional monetary policy at that time, it was able to learn from their practices in designing its policy response this time.

There was one dog that didn’t bark. Unlike during previous episodes of global economic and financial instability, there were no capital outflows except in the few weeks after the onset of the pandemic; in fact, the opposite took place. India has received enhanced capital flows in FY 2021, leading to significant accretion of its forex reserves through the RBI’s normal forex interventions. There were no new capital flow measures. However, going forward, in the event of hardening yields of advanced economy treasury bonds, particularly those of the United States, there could be a potential outflow necessitating substantial forex intervention à la 2008 and associated domestic liquidity measures. One positive feature of the enhanced forex flows in FY 2021 is that debt inflows, which are usually the first to exit, were negligible.

Overall, the RBI, in cooperation with the Government of India, has succeeded in achieving its overall objective of keeping financial intermediaries, financial markets and the financial system as a whole sound, liquid, and functioning smoothly. It has maintained financial stability despite initial conditions of the Indian financial intermediaries being stressed as a consequence of legacy problems. But very significant challenges remain as this crisis unfolds further, both in India and the rest of the world.

It has also protected households as well as small and large businesses from experiencing acute financial stress. It remains, however, to be seen what will happen as the impact of the lifting of the debt moratoriums starts to be felt. It is estimated that around 40% of the amount of all outstanding loans took advantage of the moratorium. MSMEs, in particular, were outliers with almost 70% of their debt being in this category, while only about a third of corporate loans used the moratorium.

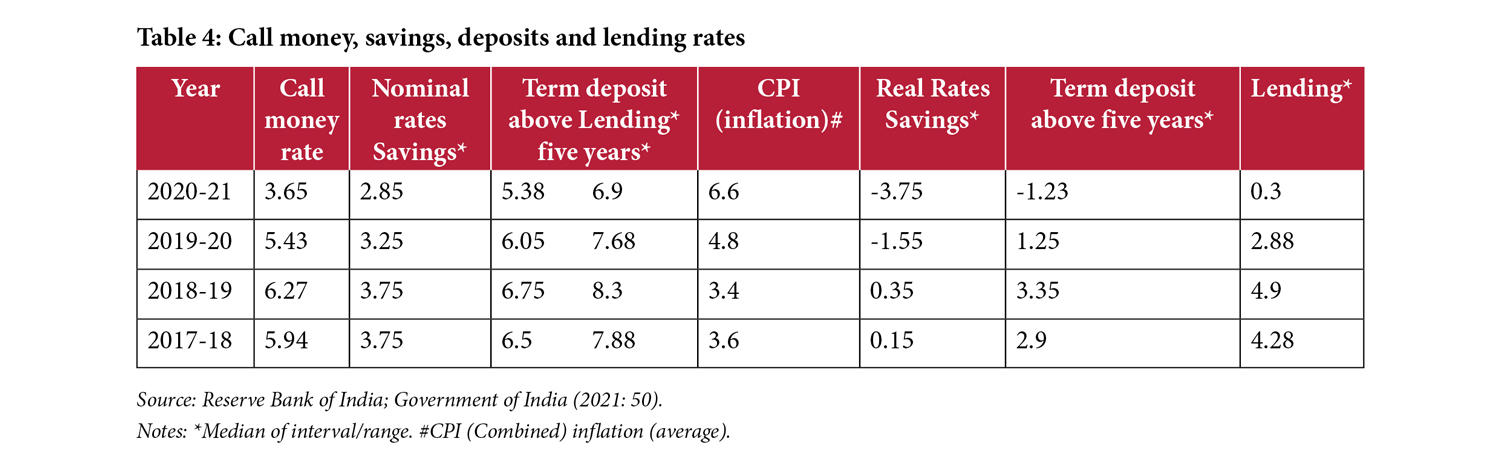

Transmission of the highly accommodative monetary policy, and the corresponding liquidity management, put in place right at the beginning of the Covid crisis has been largely successful. Interest rates have fallen across the board and g-sec yields are at almost record lows, as are private sector bond market and commercial paper yields and bank deposit and lending rates (Table 4). However, the RBI’s liquidity injection has been so large that there has been an almost consistent systemic liquidity surplus of about Rs 6 trillion (about 3% of GDP) that needs to be absorbed on a daily basis. This liquidity injection is a consequence of the RBI’s aggregate domestic asset purchases of around Rs 3 trillion and forex interventions amounting to over Rs 5 trillion over FY 2021. Therefore, the target money market interest rate (WACR) has been somewhat below the reverse repo rate.

The key positive consequence of this monetary policy and liquidity management strategy has been the successful completion of the much-enhanced government borrowing programme at low cost. Corporate bond markets have also responded because of the low cost and corporate bond issuance was in fact higher than in the previous year.

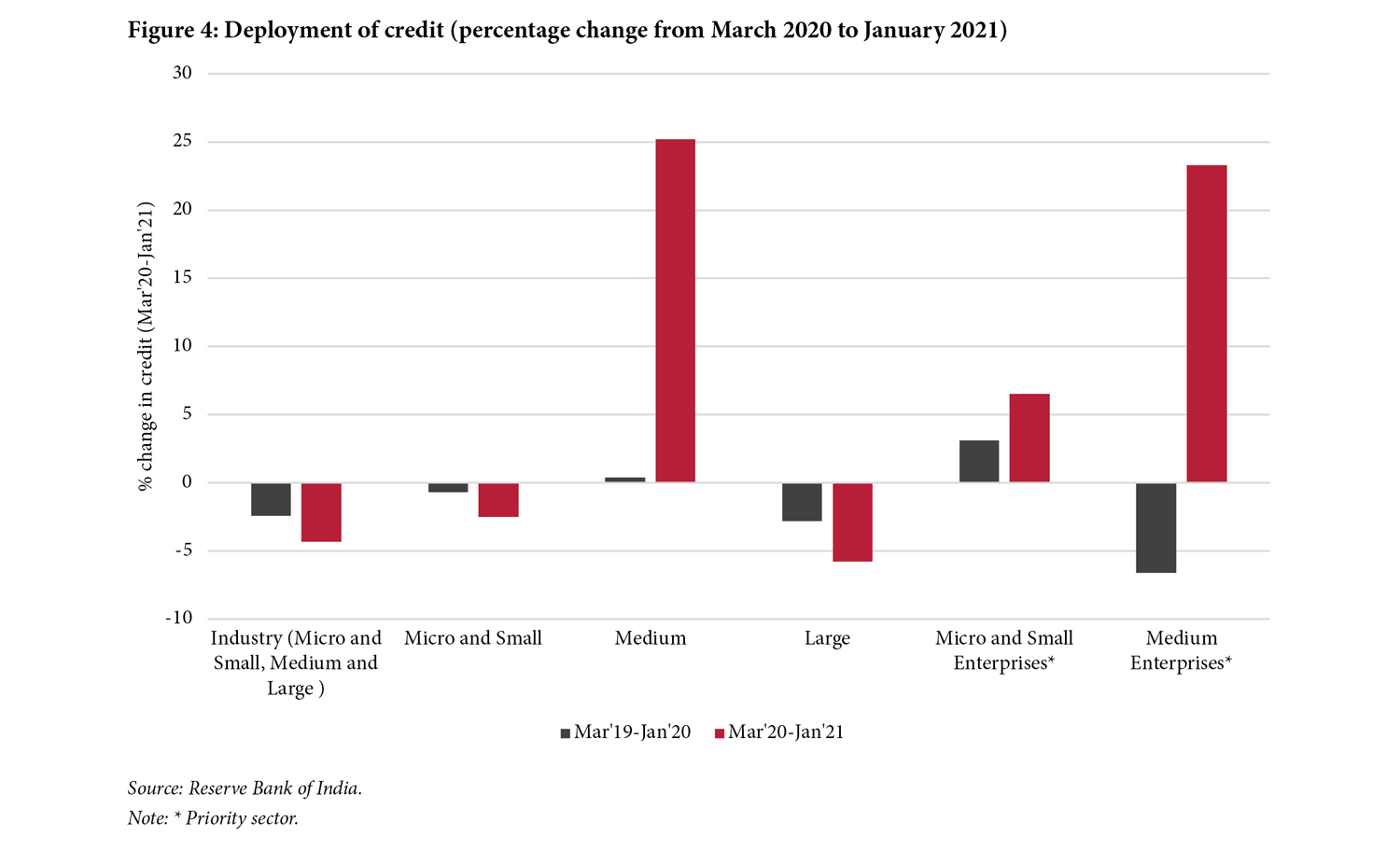

However, despite all the measures implemented to promote the flow of credit to all segments of the market, credit growth has continued to be sluggish except for a significant increase to the SMSE sector (Figure 4). Hence there is a mismatch between the performance of the real sector and financial markets. This could potentially lead to enhanced stresses experienced by both lenders and borrowers, leading to potential financial instability. As estimated by the RBI’s Financial Stability Report (RBI 2021a), the gross NPA ratio of Indian commercial banks could increase to 13.5% by September 2021, as compared with 7.5% in September 2020. Thus, financial stability challenges remain for the Indian financial system and its regulator in the months to come.

Cantú, C., Cavallino, P., De Fiore, F. and Yetman, J. (2021). A Global Database on Central Banks’ Monetary Responses to Covid-19, BIS Working Paper No. 934, Bank for International Settlements.

Government of India. (2021). Economic Survey 2020-21, Volume 1 (www.indiabudget.gov. in/economicsurvey/).

Mohan, R. and Ray, P. (2019). Indian Monetary Policy in the Time of Inflation Targeting and Demonetization, Asian Economic Policy Review 14: 67-92.

Reserve Bank of India (2019), Prudential Framework for Resolution of Stressed Assets.

Reserve Bank of India (2020a), Governor’s Statement – Seventh Bi-monthly Monetary Policy Statement, 2019-20, 27 March 2020.

Reserve Bank of India. (2020b). Monetary Policy Report, April.

Reserve Bank of India. (2020c). Statement on Development and Regulatory Policies, June.

Reserve Bank of India. (2020d). Statement on Development and Regulatory Policies, August.

Reserve Bank of India. (2020e). Monetary Policy Report, October.

Reserve Bank of India. (2020f). Statement on Development and Regulatory Policies, October.

Reserve Bank of India. (2020g). Annual Report 2019-20.

Reserve Bank of India. (2020h). Report of the Expert Committee on Resolution Framework for Covid-19 Related Stress, September.

Reserve Bank of India. (2020i). Governor’s Monetary Policy Statement, December.

Reserve Bank of India. (2020j). Statement on Development and Regulatory Policies, December.

Reserve Bank of India. (2021a). Financial Stability Report, Issue No, 22, January.

Reserve Bank of India. (2021b). Statement on Development and Regulatory Policies, February.

Reserve Bank of India. (2021c). Report on Currency and Finance.

Reserve Bank of India. (2021d). Unconventional Monetary Policy in Times of Covid-19, RBI Bulletin, March, pp. 41-56.

Reserve Bank of India. (2021e). Monetary Policy Report, April.

H. Supervisory measures

- All supervised entities (SEs) were directed to implement their operational and business continuity plans for the smooth conduct of business processes in the wake of the Covid-19 pandemic.

- Special advisories were issued for management of cyber security risks with a focus on securing sensitive data such as customer and payment system data, among others.

- Reduction of compliance burden for brief period by granting flexibility in audit coverage and in furnishing supervisory data.

- All SEs were also advised to conduct stress tests to quantify and estimate the impact of Covid-19 on their financial projections so as to strengthen their capital adequacy positions accordingly.

- Companies are allowed to park the unutilised ECB proceeds in term deposits with AD Category-I banks in India for a maximum period of 12 months. This period has been extended to March 1, 2022 for ECB drawn down before March 1, 2020.

FOOTNOTES

[1] The Indian fiscal year runs from April to March. So, FY 21 means 1 April 2020 to 31 March 2021, and Q1 FY 2021 runs from April to June 2020.

[2] Current forecasts for Indian GDP growth in FY 2022 include RBI at 10.5% and the IMF at 12.5%.

[3] There is currently an explosive surge in progress since late March 2021, the health and economic implications of which cannot be assessed at present.

[4] Because of reduced revenues due to the economic slowdown, and some legacy issues, the fiscal deficit for FY 21 is estimated to be about 9.5% of GDP, the total government debt-to-GDP ratio is likely to reach 90% in FY22.

[5] CPI inflation in February 2021 was 5.03%.

[6] Its inflation target of 4 +/- 2%, set in 2016, has just been reconfirmed for the next five years.

[7] See https://rbidocs.rbi.org.in/rdocs/PressRelease/PDFs/PR1900EC7E5351A39741EEB4FE8B9203BEA6DB.PDF

[8] About 0.67% of GDP.

[9] A similar episode of negative real rates took place in the early 2010s after the NAFC, consequent to an extended highly accommodative monetary policy stance. There was some evidence of flight to safety of household assets like gold (Mohan and Ray, 2019).

[10] To quote Mario Draghi, then Governor of the European Central Bank, in 2012.

[11] https://rbi.org.in/Scripts/NotificationUser.aspx?Id=12071&Mode=0

[12] The Government of India introduced the “Emergency Credit Line Guarantee Scheme” for lending to MSMEs with a guarantee limit of Rs 3 trillion. The scheme has undergone a number of changes over the year. The tenor of loans under this scheme can be extended for up to six years, including a moratorium period of two years. Starting with the original intention of enhancing credit to MSMSEs, it has now been extended to cover the hospitality, travel and tourism, leisure and sporting sectors, in addition to the 26 stressed sectors (RBI 2020h: 12) identified as eligible for resolution.

Rakesh Mohan

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.