Climate Finance Needs of Nine G20 EMEs: Well Within Reach – Macroeconomic Consistency

Reading Time: 6 minutesIntroduction

The transition towards a low-carbon global economy has made climate finance one of the most critical challenges facing emerging market and developing economies (EMDEs). The report of the Independent High-Level Expert Group on Climate Finance (2022) estimated that EMDEs (other than China) would need to mobilise $1 trillion per year up to 2030, which was later revised to $2.3-$2.5 trillion annually in its November 2024 update. This underscores the serious challenges that lie ahead.

Our study ‘Climate Finance Needs of Nine G20 EMEs: Well Within Reach’ assesses climate finance requirements of nine G20 economies (Argentina, Brazil, China, India, Indonesia, Mexico, the Russian Federation, South Africa, and Turkiye) for four sectors – power, road transport, cement and steel. The period covered for the study is up to 2030.

Our study ‘Climate Finance Needs of Nine G20 EMEs: Well Within Reach’[1] assesses climate finance requirements of nine G20 economies (Argentina, Brazil, China, India, Indonesia, Mexico, the Russian Federation, South Africa, and Turkiye) for four sectors – power, road transport, cement and steel. The period covered for the study is up to 2030. This study, unlike most other studies, follows a bottom-up approach for assessing climate finance requirements. Furthermore, the study estimates climate finance or additional capital expenditure (capex) requirement purely on account of transition to a low carbon economy over and above the business-as-usual (BAU) investment.

It is estimated that the nine EMEs would need climate finance of $2.2 trillion ($255 billion or 0.6 per cent of combined GDP annually) to decarbonise all the four sectors for the period 2022-2030

It is estimated that the nine EMEs would need climate finance of $2.2 trillion ($255 billion or 0.6 per cent of combined GDP annually) to decarbonise all the four sectors for the period 2022-2030[2]. Almost two-thirds of additional capital expenditure estimated are for China ($1,341 billion or about 0.7 per cent of China’s GDP, annually). Excluding China, the additional capital expenditure requirement amounts to $854 billion ($100 billion or 0.5 per cent of GDP, annually). The sectoral break-up reveals that the climate finance requirement is driven largely by the steel sector ($733 billion or 55 per cent of total estimated total climate finance requirement), followed by road transport ($336 billion or 25 per cent), cement ($217 billion or 16 per cent) and power ($55 billion or 4 per cent).

At this stage, it is not clear as to how much of climate finance requirement of EMDEs will be met from external sources. The available data suggest that total official external climate financial flows to emerging market economies have been small, at less than $300 billion in 2023. Nevertheless, it is important to be cognisant of the challenges such external financial flows, should they occur on a larger scale, could pose and be prepared to address them effectively.

Challenges in Managing Capital Flows

Capital flows into an economy can be absorbed easily to the extent of a country’s current account deficit (CAD), which, in fact, finances the gap between domestic savings and investment. Capital inflows that exceed the current account deficit are not absorbed into the domestic economy. Hence, they could have significant implications for the economy if not deftly managed. In any case, they would not help in financing climate change. This also applies to a country with a current account surplus. In both the cases (capital flows greater than the CAD, and countries with current account surplus), additional capital flows could impinge on the exchange rate with an adverse impact on export competitiveness if a country decides not to intervene in the forex market. On the other hand, if a country decides to intervene in the forex market to avoid its adverse implications on the exchange rate, it will result in an increase in net foreign assets (NFAs) and expansion in monetary base. If this is not consistent with monetary base requirement of a growing economy, other measures may be needed, such as sterilisation, and could complicate monetary and macroeconomic management.

In practice, most central banks in emerging economies tend to follow an eclectic approach to manage capital flows. They might allow some impact on the exchange rate if consistent with their productivity growth, while absorbing a part of such flows into reserves leading to an expansion in NFAs and corresponding domestic liquidity, as may be consistent with the growth requirements of the economy. However, for the purpose of analysis, we ignore capital flows which can be managed by allowing appreciation of the exchange rate as this will depend on exchange rate policy of each central bank and several other factors, which are not easy to predict.

As we examine the specific context of climate finance flows, it becomes evident that the management of these inflows must be both strategic and tailored to the specific economic conditions of each country.

Macro-Consistency of Estimated Climate Finance Requirements

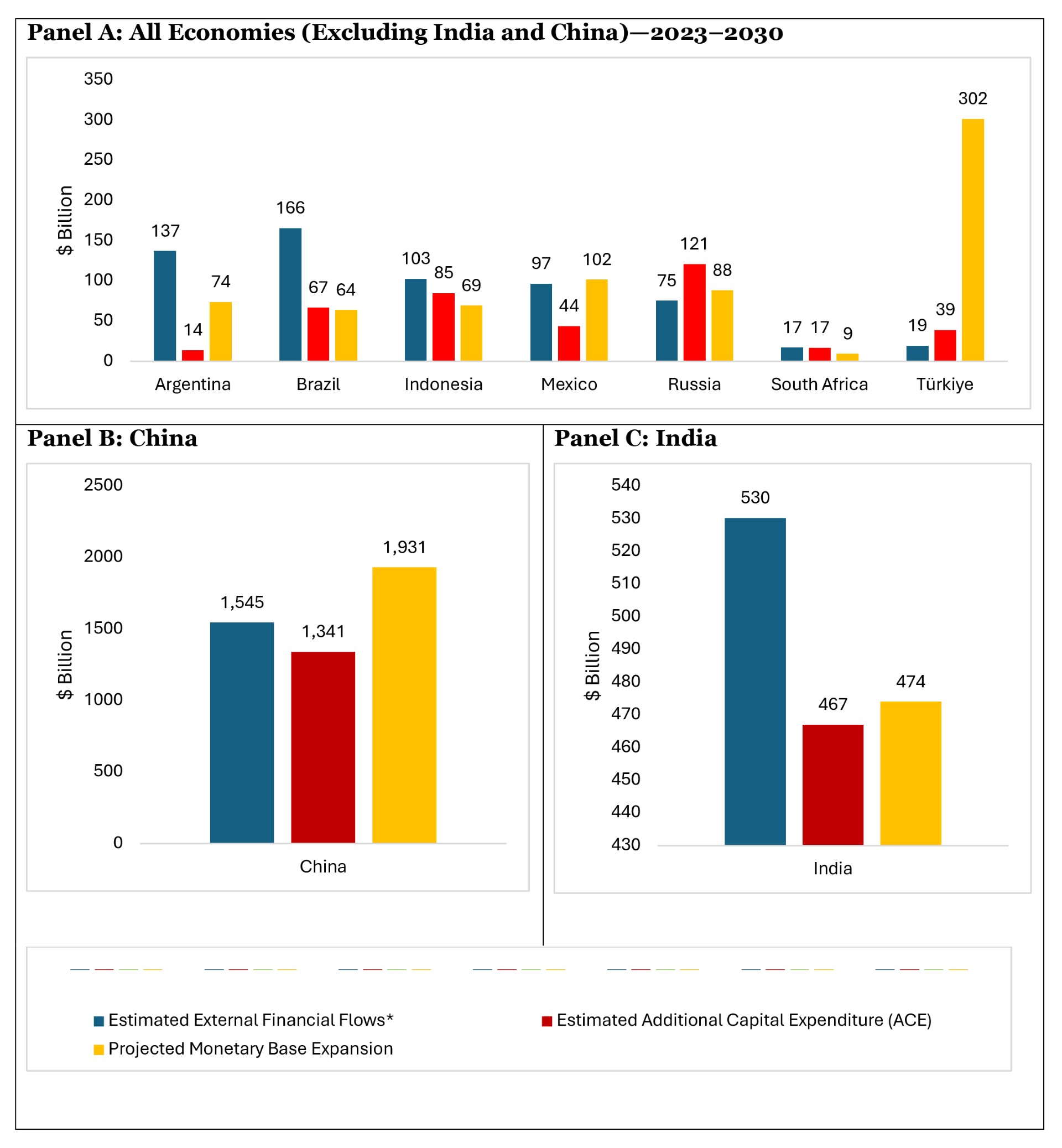

External financial flows (capital and financial flows net of current account balance) for the nine economies in the BAU scenario for the period from 2023-2030 are estimated at $2,690 billion. Excluding China, such flows are estimated at $1,145 billion. At a disaggregated level, external financial flows up to 2030 are assessed in the range of $17 billion (South Africa) and $1,545 billion (China) – Figure 1. It is significant that the external financial flows estimated are broadly in line with those projected by the International Monetary Fund.

All the nine economies combined are projected to receive external financial flows of $3.1 trillion ($1.2 trillion, excluding China) from 2023 to 2030 in the business as usual which works out $445 billion ($169 billion excluding China) annually, consistent with the expansion in monetary base[3]. This leaves a very small room of $423 billion for managing climate finance from external sources. External financial flows that can be managed consistent with an expansion in monetary base from 2023 to 2030 vary from country to country – $9 billion in the case of South Africa, $64 billion for Brazil, $69 billion for Indonesia, $75 billion for Argentina, $90 billion for Russia, $100 billion for Mexico, $300 billion for Turkey, $475 billion for India and $1,930 billion for China (Figure 1).

Figure 1: Estimated External Financial Flows*, Climate Finance Requirements and Expansion in Monetary Base

*External Financial Flows = Current Account Balance+ Capital Inflows + Financial Inflows

*External Financial Flows = Current Account Balance+ Capital Inflows + Financial Inflows

Türkiye is the only economy which can comfortably manage both external financial flows and estimated climate finance (should it flow from external sources). China, Mexico and Russia can manage climate finance flows from external sources to some extent alongside BAU external financial flows.

The ability to manage both (i) external financial flows in the BAU; and (ii) climate finance from external sources, consistent with an increase in monetary base of most of the EMEs under study is constrained. Türkiye is the only economy which can comfortably manage both external financial flows and estimated climate finance (should it flow from external sources). This is mainly because Türkiye is projected to receive small external financial flows. Expansion in monetary base in some economies such as China, Mexico and Russia is projected to be more than the external financial flows in the BAU. Therefore, these economies can manage climate finance flows from external sources to some extent alongside BAU external financial flows. All other economies would need to skilfully manage both external financial flows in the BAU scenario and climate finance from external sources.

While undertaking the above exercise, it has been assumed that an entire increase in monetary base takes place by an increase in net foreign assets (NFAs). To the extent monetary base expansion takes place by an increase in net domestic assets (NDAs), it will further circumscribe the management of external financial flows, unless the authorities decide to resort to sterilisation of such flows, which creates its own complications.

Conclusion

EMDEs, need climate finance from external sources to some extent to address climate change and build resilience. However, such flows could also pose significant macroeconomic challenges if the external flows are expected to be substantial. Therefore, the authorities in each country would need to prepare to manage large external climate finance flows, balancing the need for climate finance with the overarching goal of maintaining macroeconomic stability. EMDEs must tailor their strategies to their country-specific economic contexts. Some countries may need to examine whether there is a scope to expand their CADs, while others may need to consider whether they could reduce current account surpluses. Increased generation of domestic resources from greater savings would also have to be considered. Skilful management of climate finance flows from external sources will ultimately determine the success of climate finance mobilisation for transitioning to a low-carbon global economy.

Our analysis suggests that the current global discussion and estimation of the need for large external financing of EMDE climate-related investment requirements must be tempered with consideration of macro consistency conditions. If climate finance from external sources by way of grants is not large, then the capacity of EMDEs to absorb/manage external flows will also be limited by their debt sustainability concerns, both domestic and external.

Our estimates of the total climate finance needed by the Nine G20 EMES are much lower than other prevalent estimates, as is the potential need for external savings for such financing. These estimates suggest that they could also be macroeconomic consistent with some additional generation of domestic resources.

This analysis must be done on an individual country basis by the multilateral development banks (MDBs) and the International Monetary Fund (IMF) to arrive at realistic estimates of the magnitudes involved.

FOOTNOTES

[1] President Emeritus and Distinguished Fellow and Senior Fellow, Centre for Social and Economic Progress, New Delhi.

[2]Raj, J., and Mohan, R. (2025). “Climate Finance Needs of Nine G20 EMEs: Well Within Reach” (CSEP Working Paper 106). New Delhi: Centre for Social and Economic Progress.

[3] Brazil, India, Indonesia, Mexico, Russia, South Africa, and Thailand target interest rate. Argentina moved to a regime of monetary base target in 2018. China makes a significant use of quantity-based policy instruments, though interest rates now play a greater role than in the past. In economies where central banks target interest rate, the factors affecting the monetary base are exogenous for the central bank. As such, those central banks may not exert direct influence on the size of the monetary base, which depends on the portfolio decisions of the private sector. Nevertheless, monetary base remains relevant for most economies considered in the study as its unbridled growth may have a significant bearing on nominal interest rates and could also complicate macroeconomic management.

Rakesh Mohan

Janak Raj

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.