Climate Shocks, Food, and Inflation: Time to Rethink Macroeconomic Policies?

Reading Time: 8 minutesIndia’s recent experience offers a striking lesson in how climate extremes are impacting its macroeconomic landscape. Between 2022 and 2024, the country endured consecutive years of record heat, erratic monsoons, and persistent food-price pressures. Wheat yields shrank, the rice harvest faltered, public grain reserves dropped, and food inflation refused to recede.

Food price spikes were long considered temporary, induced by adverse monsoon or other supply shocks, and limited to specific crops. That assumption was overturned, raising doubts if the pattern still holds. Climate-driven supply disturbances appear to arrive faster, last longer, and can hit multiple crops simultaneously. The question is no longer recurrent, overlapping shocks that hit both crops and prices in tandem but whether macroeconomic policies must adapt to a hotter and more volatile world that climate change is now creating.

The climate signal is unmistakable

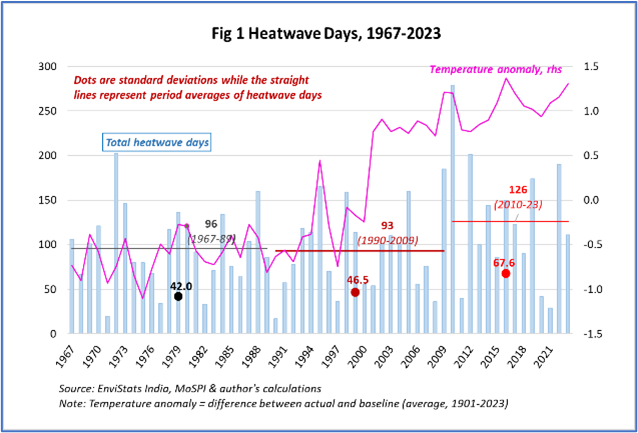

India’s mean temperature has risen about 1.7 °C since 1901, but most of the increase has occurred in the past fifteen years (Fig 1). The number of heatwave days jumped roughly 35 per cent since 2010 with greater volatility and the heat now arrives earlier – sometimes in February – directly affecting the wheat crop during flowering and grain-filling.

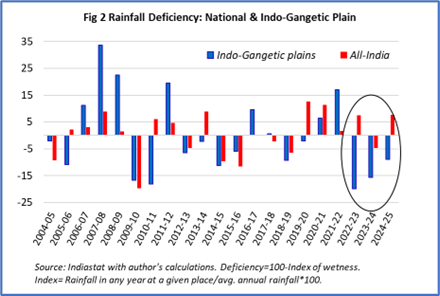

Rainfall too has turned erratic. National averages mask deep regional divergence. Even when the all-India monsoon averages near normal, the distribution of rain has changed sharply. The Indo-Gangetic Plain (IGP), India’s key rice-wheat belt, has seen frequent deficits even when the national average looks stable (Fig 2). In 2022 and 2023, rainfall in the IGP was about 20 and 16 per cent below normal, while national totals barely deviated. Statistical distributions have shifted: what used to be rare dry years are now frequent, hotter years increasingly coincide with drier or unusual monsoons, the correlation nearly doubled over the last decade.

Climate disturbances are not isolated or alternating but concurrent and compounding

These back-to-back deficits, coupled with record heat, perhaps point to a turning point. Climate disturbances are not isolated or alternating but concurrent and compounding.

When both wheat and rice fail

Traditionally, India’s two cereal cycles – wheat in winter, rice in summer – provided a natural hedge against weather shocks. Recent years have broken that pattern. Heatwaves cut short wheat maturation in 2022 and 2023, while erratic monsoons depressed rice yields, especially in eastern Uttar Pradesh, Bihar, and West Bengal.

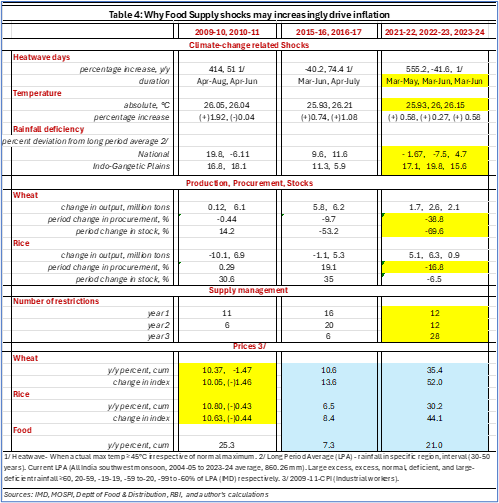

For the first time in decades, all three major cereal crops – kharif rice, rabi rice, and rabi wheat – fell short of targets in consecutive years. Wheat output growth slowed to barely 1 per cent a year after 2020, compared with 4–5 per cent annual growth before. In 2023, rice output too undershot official estimates by nearly one-fifth.

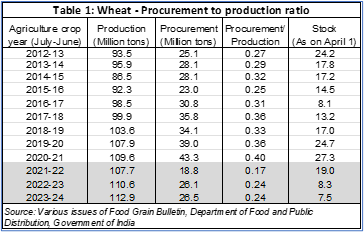

Public procurement, the backbone of India’s food-security system, dropped precipitously (Table 1). Government wheat purchases fell from 40 per cent of production in 2020-21 to just 17 per cent the next year, while buffer stocks slid to their lowest in fifteen years. Madhya Pradesh, which rose to match Punjab in wheat production, saw its procurement ratio collapse from about 70 per cent to 20 per cent.

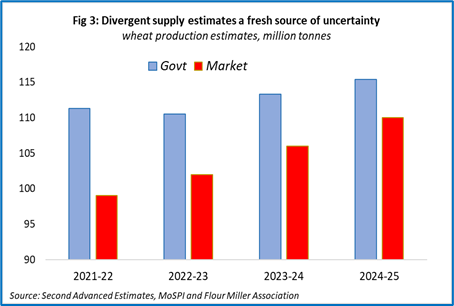

However, output did not drop correspondingly, indicating weaknesses in data and estimation methods. The gap between government and market yield assessments, for example, widened dramatically (Figure 3) and has maintained since, aggravating uncertainty that fed into price expectations and undermined credibility.

Managing scarcity through interventions and controls

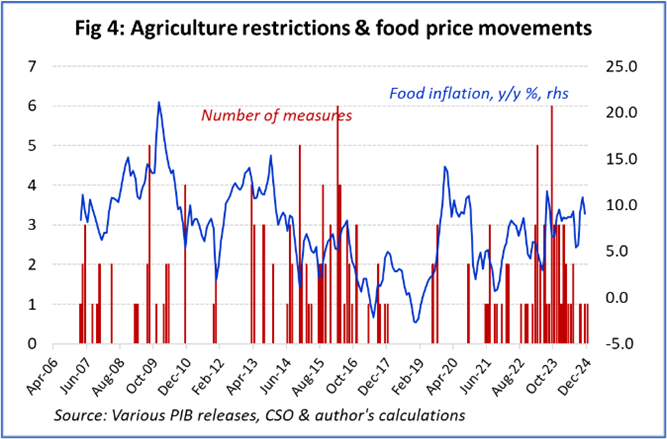

With steep food-price pressures in years, the government responded firmly with a range of supply-side actions, e.g., export bans, successive stock limits, import duties, and open-market sales. The number of such interventions steadily climbed, doubling between 2021 and 2024 with at least one new restriction almost every month, twice as many as during previous food-price episodes (Figure 4). By 2023-24, 28 separate measures were imposed in a single year. This represents a step shift in the frequency and intensity of supply management compared to the past.

These were supplemented with substitution of rice for wheat, the second policy response. Rice allocations in the public distribution system were doubled, shifting welfare beneficiaries from wheat to rice. This contained immediate shortages but added fiscal pressure and, ironically, boosted rice demand and prices.

These responses restrained domestic prices temporarily but at visible cost. Supply management as the sole stabilisation instrument crowded out market mechanisms, reduced private incentives to store or import grain, and blocking international trade denied domestic markets a key shock absorber, worsening future volatility while disrupting global markets.

The inflation story: When food prices stop being transitory

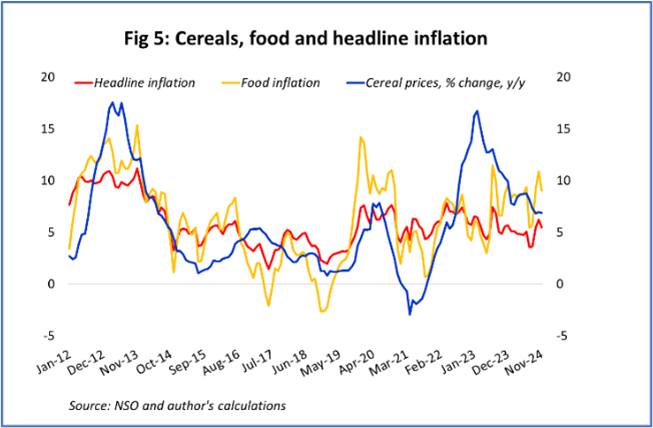

Headline CPI inflation remained well above the 4 ± 2 per cent target band for five years with increased volatility than before (Figure 5). Food inflation, which usually ebbed within a few months, persisted for years and adding twice as much on average each month to headline CPI inflation after 2019 than the average 1.5 percentage points contributed before. Since 2021, food inflation accounted for over 70 per cent of total inflation in some quarters. Cereals alone contributed about one-fifth of total price rise after 2022.

The usual mean-reverting pattern of food-price shocks did not play out; the price level ratcheted upwards, and persistent expectations further entrenched the price rise, embedding inflation inertia

Food’s weight in India’s CPI (46 per cent) ensures macroeconomic impact. The usual mean-reverting pattern of food-price shocks did not play out, the price level ratcheted upwards, and persistent expectations further entrenched the price rise, embedding inflation inertia. It is noteworthy that the strict and extensive supply measures did not cool retail prices sufficiently or long enough to prevent these effects. This possibly indicates diminishing returns from prolonged use. Preventing global arbitrage that might have relieved domestic supply was possibly mistaken; while, some overlapping interventions, though well-intentioned, arguably created a feedback loop of uncertainty and expectations that kept inflation elevated.

Is it different this time?

How do these developments compare with earlier food-price surges, e.g., 2009-11 and 2015-16? Table 2 summarises these. A comparison reveals significant differences.

Despite far more intense interventions, inflation remains stubborn, hinting at declining efficacy of traditional tools.

Three features stand out. First, the clustering of shocks: consecutive years of heat and drought are hitting both cropping seasons. Second, the correlation between temperature and rainfall anomalies – hotter years now coincide with drier monsoons. Third, the policy fatigue – despite far more intense interventions, inflation remains stubborn, hinting at declining efficacy of traditional tools. Together these suggest climate-driven shift in weather patterns, food supply and price dynamics, suggesting climate volatility may no longer be a negligible or background risk.

India’s macroeconomic policy framework, built for short-lived supply shocks, must evolve for a future where climate disruptions are frequent, correlated, and persistent.

Policy lessons: re-engineering macro management for a hotter era

The paper’s central argument is that India’s macroeconomic policy framework, built for short-lived supply shocks, must evolve for a future where climate disruptions are frequent, correlated, and persistent. The inferences span agriculture, trade, fiscal and monetary policy.

- Agriculture: from self-sufficiency to resilience

Policies must focus on mitigating climate risks through investments in climate-resilient seed varieties, real-time crop monitoring/data systems for yield assessment and capturing localised variability. Two, a wide deployment of digital agrimetrics and satellite imagery to address data blind spots is essential to minimise the risk of policy errors. Three, the proposed stabilisation and diversification of wheat and rice cultivation in states facing soil damages (e.g., Punjab) may need re-visiting or slowing down if MP is more vulnerable to climate shocks – a feature that needs deeper scientific investigation. Last, open agriculture markets are needed to increase competition, efficiency and flexibility, to motivate private investments along the food supply chain for smoother navigation of disturbances.

- b) Trade: from discretion to rules

Ad-hoc export bans and import duties undermine producers’ incentives and market stability. Such interventions can be made more predictable and less distortionary by transparent and automatic mechanisms based upon domestic prices/grain stock thresholds. Strategic use of global markets instead of insulation can buffer domestic volatility – selective openness to imports is a useful safety valve during severe shortfalls without risking food security.

- c) Monetary policy: integrating climate persistence

Persistent food inflation complicates forecasting and inflation-targeting credibility of the central bank. Increased frequency and volatility of food supply shocks means that ‘seeing through’ may be difficult with mounting climate risks – monetary tightening may, therefore, must be frontloaded to keep inflation expectations anchored and ensure that relative price shifts do not turn into an enduring inflation problem. To help anchor expectations without over-tightening policy, a balance can also struck with structural changes in trade and agriculture policies.

- d) Fiscal policy: cushioning without crowding out

Longer-lasting food shocks will undoubtedly raise fiscal demands through welfare transfers, food subsidies, and direct income support to the poor, as well as for essential public investments in climate adaptation, research and development. Public finances could, therefore, be burdened with recurring outlays. This would require adjustments in the budgetary frameworks to balance welfare and growth. Revenue mobilisation efforts must be strengthened to maintain public capital spending, therefore.

- e) Coordination: breaking silos

Climate shocks blur the boundary lines between agriculture, trade, finance, and the central bank. Although coordinated towards food security and price stabilisation goals, yet different policies perceive similar problems from different perspectives and mandates. A joint macro-climate coordination mechanism, integrating real-time climate intelligence with policy design, could enhance response speed and coherence while reducing uncertainties.

Monetary policy cannot offset crop failures; fiscal policy cannot permanently subsidise food; and trade protectionism amplifies global scarcity.

Monetary policy cannot offset crop failures; fiscal policy cannot permanently subsidise food; and trade protectionism amplifies global scarcity.

The broader stakes: Beyond India

What India experienced between 2021 and 2024 holds lessons beyond its borders. As climate variability intensifies globally, food-price shocks are likely to be a recurring source of macroeconomic volatility, especially for emerging economies where food constitutes major part of the consumption basket and much of political stability. If climate volatility turns food inflation from a transitory to a structural feature, conventional macro frameworks could be weakened everywhere. Monetary policy cannot offset crop failures, fiscal policy cannot permanently subsidise food, and trade protectionism amplifies global scarcity. Ignoring this reality risks a new equilibrium of chronically high food prices, compressing real incomes and increasing inequality. In this light, a reorientation of macroeconomic policy design – towards climate risk recognition and backed by investments in climate adaptation is important.

Conclusion: towards climate-compatible macroeconomics

The lessons from the past few years’ combination of exceptional heat, erratic rains, procurement drops, and persistent inflation signify fundamental departures from similar past episodes. Traditional buffers like public reserves, export controls, and monetary tightening are proving insufficient and unsustainable. It is important to incorporate climate sensitivity into fiscal planning and inflation analysis therefore, reform trade and food supply shock management to counter declining policy effectiveness, and advance adaptation with data and technology investments for early warnings.

(Adapted from Renu Kohli “Climate Shocks, Food Supply, and Prices: Do We Need to Rethink Macroeconomic Policies?” CSEP Working paper, October 3, 2025.)

Renu Kohli

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.