Oil Shock Bringing India’s EV Transition to a Crossroads

Reading Time: 5 minutesIndia’s electric mobility transition is no longer a linear story of climate ambition and technological progress. It now sits at the intersection of geopolitical oil disruptions, fiscal trade-offs, tax policy evolution, and electoral strategy.

India’s electric mobility transition is no longer a linear story of climate ambition and technological progress. It now sits at the intersection of geopolitical oil disruptions, fiscal trade-offs, tax policy evolution, and electoral strategy. The recent oil supply shock through the Strait of Hormuz has exposed structural vulnerabilities in India’s petroleum import dependence, while recent research published by CSEP on electric vehicle (EV) cost-competitiveness reveals a more nuanced reality: India’s EV transition is close to becoming organically competitive, subject to some ifs and buts.

Understanding this interplay is critical to assessing whether India’s road transport is on a durable path toward electrification, particularly in view of the ongoing oil crisis.

Is the Oil Crisis a Structural Turning Point for India?

The sharp decline in crude oil shipments through the Strait of Hormuz has triggered a supply shock that extends beyond short-term price volatility. For India—one of the world’s largest oil importers—this disruption directly affects energy security, import bills, inflation dynamics, and fiscal balances.

The crisis has forced India to scramble for oil from wherever available. Temporary relaxation of the US-imposed embargo on Russian and Iranian crude may have helped cushion some immediate supply shocks, but has not eliminated underlying vulnerabilities. Depreciation of the rupee by nearly 10% this financial year (FY2025–26) has not helped India’s cause either as far as procuring oil is concerned.

Crucially, this episode reinforces a long-standing strategic concern: India’s mobility system is heavily exposed to external shocks.

Despite Supply Drop, Fuel Prices Remain Stable

India imports nearly 85% of its crude oil demand. Crude is also the major cost component for Oil Marketing Companies (OMCs) such as Indian Oil Corporation Limited (IOCL), Bharat Petroleum Corporation Limited (BPCL), and Hindustan Petroleum Corporation Limited (HPCL), which together control about 90% of the country’s fuel retail market. These companies are publicly listed, although the Government of India holds over 50% equity in IOCL and BPCL, whereas Oil and Natural Gas Corporation, with 59% government holding, is the largest shareholder in HPCL.

Officially, petrol and diesel prices are fully deregulated in India (petrol was deregulated in June 2010, while diesel was deregulated in October 2014). This gives OMCs a free hand to make the retail prices of petrol and diesel cost-reflective, meaning that with the rise in crude oil import price, OMCs can hike the retail oil price to prevent their outright losses. However, the current surge in import prices has not yet translated into higher retail prices.

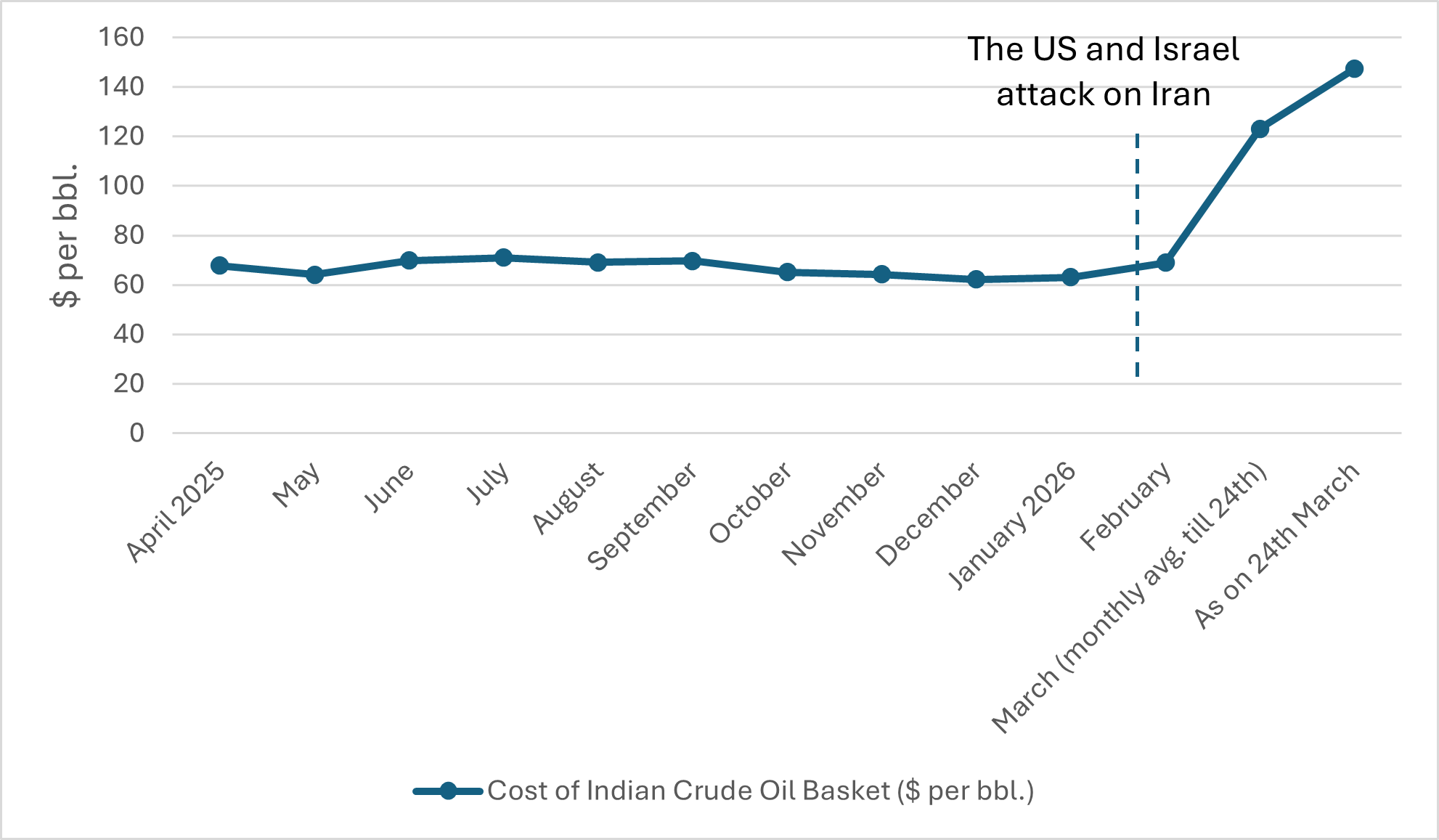

As shown in Figure 1, compared to January levels, the cost of the Indian Crude Oil Basket, which reflects the fuel cost for the OMCs, has gone up by about 133% (as of March 2026). Despite this surge in the crude procurement cost in the past weeks, retail petrol and diesel prices have remained unchanged, with OMCs hiking prices of only premium petrol and bulk diesel by ₹2 per litre and ₹22 per litre, respectively.

Figure 1: Cost of Indian Crude Oil Basket (US$ per barrel) since April 2025

Source: Petroleum Planning & Analysis Cell, Ministry of Petroleum and Natural Gas of India.

Note: Monthly crude oil price is the average of daily prices of the respective month. Average for the current month is till date (i.e., 24th March 2026).

According to ICICI Securities, OMCs are now facing a loss of about ₹13.50 per litre on the retail sale of diesel and ₹1 per litre on petrol. While public sector enterprises have maintained the status quo for petrol and diesel prices at their fuel refilling stations, a major private fuel retailer, Nayara Energy, has hiked normal-grade petrol and diesel prices by up to ₹5 per litre effective from March 26, 2026.

This raises an important question: Is this an economic anomaly or a political choice? Fuel price stability serves as an anti-inflationary lever. A rise in petrol and diesel prices is usually not politically palatable, especially when elections are on the horizon. Whether the upcoming State Assembly elections have a role to play in the current fuel price status quo is a million-dollar question. That said, OMCs have earned a combined net profit of over ₹34,000 crore in the first half of the FY2025–26, primarily due to subdued international crude oil prices until the West Asia crisis erupted. This profit has helped absorb the recent crude price shock to an extent.

Does Oil Shock Impact India’s EV Transition?

EVs continue to have higher price tags compared to internal combustion engine (ICE) vehicles. This gap has historically been bridged, in part, through lower GST rates (5% for EVs), Motor Vehicle (MV) tax exemptions (depending on the states), and purchase subsidies (subject to eligibility to central and/or state schemes).

Skyrocketing oil prices raise the operating costs of ICE vehicles, which should significantly improve EV competitiveness. However, the transition does not seem automatic. With retail petrol and diesel prices maintained at the pre-crisis level despite elevated global oil prices, the operating cost advantage of EVs remains muted.

However, GST rationalisation in September 2025 reduced taxes on ICE vehicles. The aforementioned study shows that this reduction has widened the EV price gap by ₹1.1 lakh to ₹1.5 lakh for electric passenger cars and about ₹7,000 for electric two-wheeled vehicles. Despite this disadvantage, the study projects EVs nearing cost parity around 2030 (in some passenger vehicle segments), driven by inherently lower running costs of these vehicles and the expected decline in international lithium-ion battery prices. However, this assessment has not taken into account possible elevated domestic oil prices, which could soon be a reality in India if the international oil market continues to roil.

In today’s uncertain and unsettling world, things can change rapidly. The West Asia conflict-induced oil shock could well become an inflection point for India’s auto sector. Skyrocketing oil prices raise the operating costs of ICE vehicles, which should significantly improve EV competitiveness. However, the transition does not seem automatic. With retail petrol and diesel prices maintained at the pre-crisis level despite elevated global oil prices, the operating cost advantage of EVs remains muted.

Fuel price controls have suppressed the true cost of oil consumption, thereby weakening the immediate economic trigger that would otherwise favour vehicle electrification. Barring a few incidents of panic buying at fuel stations, there are no signs suggesting that Indian vehicle users are feeling the heat of today’s global energy reality, at least for the time being. In effect, this delays the possible behavioural shift towards alternatives like EVs, even during an oil shock.

Oil-consuming conventional vehicles expose consumers to uncertain future fuel prices, whereas EVs assure more predictable usage expenses. The current cost metrics do not fully capture this risk-adjusted perspective, which is increasingly relevant in a geopolitically unstable environment.

In contrast, mainland Europe is witnessing increased interest in EVs. Customer enquiries have reportedly soared across marketplaces like France (50%), Romania (40%), Portugal (54%), and Poland (39%). The trend is becoming more pronounced with each passing week as auto fuel prices stay high.

Crux of the Matter

Volatility and associated risks have national implications and should be treated as a strategic variable. Notwithstanding the controlled domestic fuel price, the current upheaval in the global oil market reveals the vulnerability of India’s petroleum security and throws its fiscal math. Oil-consuming conventional vehicles expose consumers to uncertain future fuel prices, whereas EVs assure more predictable usage expenses. The current cost metrics do not fully capture this risk-adjusted perspective, which is increasingly relevant in a geopolitically unstable environment. As the saying goes, never let a good crisis go to waste. Probably, there has never been a better time for India than now to pivot away from the age-old petroleum dependence toward alternatives like EVs—whose true lifetime costs may already be more attractive than their conventional peers in today’s circumstances.

Shyamasis Das

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.