Building India’s Electric Vehicle Supply Chains: A Case for Indo-German Cooperation

DOWNLOADS

Executive Summary

Overview of Electric Vehicle Supply Chains and India’s Need to Decarbonise

India is undergoing a structural transformation to address its climate vulnerabilities. It has committed to reaching 30% electrification of new vehicles by 2030 in the short term and net-zero emissions by 2070 in the long term. A key aspect of meeting these targets is creating resilient manufacturing value chains for the technologies needed to meet these ambitions. However, the global supply chains required to sustain the green mobility transition are fragile and concentrated—an issue affecting not just India, but many major economies globally. India currently has a 100% import dependency on the key minerals required to manufacture electric vehicle (EV) batteries, in both the ore and processed forms: lithium, cobalt, and nickel. Since much of the midstream processing of these battery minerals takes place in just one country—China—India faces a risk in its EV supply chains. Indian manufacturers have already faced challenges in acquiring requisite technologies, and without a strategy to mitigate these risks, domestic manufacturing will remain vulnerable to global and regional volatilities.

Strengthening India’s EV Manufacturing Ecosystem

So far, India’s domestic EV policy landscape has been driven by demand-side purchase subsidies (e.g., the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme) and downstream assembly incentives, through the Production-Linked Incentive (PLI) Scheme for Advanced Chemistry Cells (ACC). However, these schemes have not been able to address the supply risks in upstream mineral procurement and midstream processing, despite having domestic value-addition requirements, due to a lack of suitable local options. Furthermore, India’s EV market is significantly different to those in the West; a large share of mobility electrification in India stems from two-wheelers (2Ws), three-wheelers (3Ws), and public transport, rather than passenger four-wheelers (4Ws). A resilient EV manufacturing strategy for India rests on improving mineral efficiency by minimising imported mineral needs per passenger-kilometre, and maximising local value addition in the midstream chemical processing and cell manufacturing.

The Need for International Strategic Cooperation

India cannot single-handedly overcome all the challenges it faces in the upstream and midstream segments of the value chain. State-backed enterprises like Khanij Bidesh India Ltd. (KABIL) have acquired mineral blocks abroad, though this alone is not enough if the raw ore needs to be sent to a different country for refining. India will need to develop capacities to mine critical minerals domestically and abroad, scale up processing capabilities, and begin manufacturing specialised components for EVs. However, there exist geological, technical, and financial challenges for India to resolve these alone domestically. Strategic alliances with like-minded partners can help de-risk investments, provide advanced technologies, and co-develop alternate supply chains.

Germany as a Complementary Partner

India needs to find partners for collaboration in developing resilient EV manufacturing capacities. While China currently leads in almost all aspects of these supply chains, equal-footing partnerships might be challenging given its use of critical mineral and technology exports as leverage. Other major battery manufacturers, like those in South Korea and the US, tend to prefer keeping the processing of intellectual property (IP) to themselves, particularly if there are vertically integrated plants. In contrast, Germany, projected to become the thirdlargest battery manufacturer by 2030, serves as a viable strategic partner. While it has a world-class automotive industry, it lacks the geological potential for battery minerals. Germany also faces higher energy and labour costs domestically, which provides an avenue for alignment with India’s goals: Germany can provide its advanced technology IP and state financing for acquiring raw materials as well as processing and recycling plants, while India can provide lower operating costs, access to a vast pool of engineers, domestic market scale, and a stepping stone for German EV manufacturers to export from India.

Areas of Collaboration

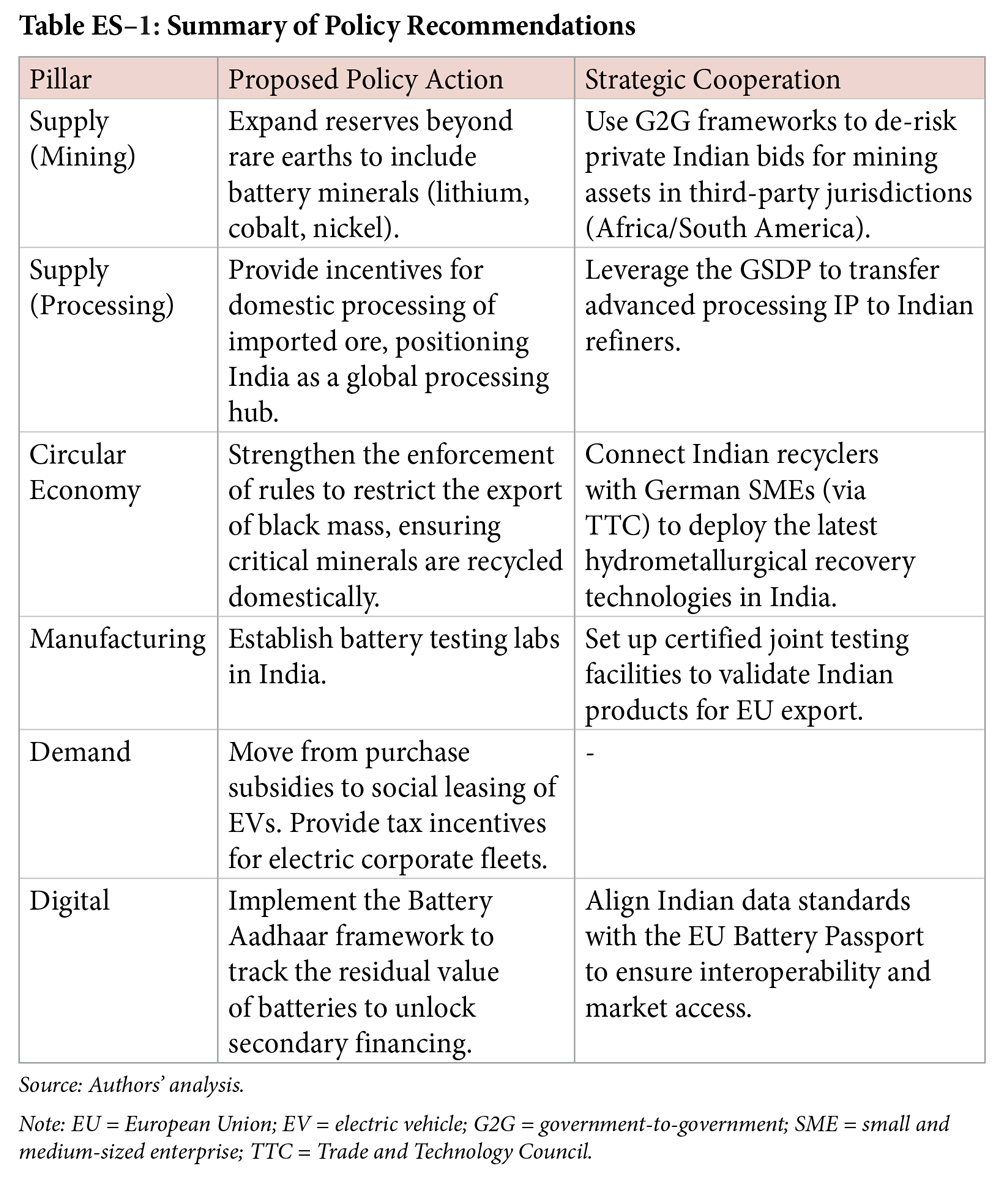

Indo-German cooperation on EV supply chains can be operationalised in three areas. These will help de-risk investments, enhance bilateral market access, and create more resilient EV supply chains:

- Financing: The Indo-German Green and Sustainable Development Partnership (GSDP) and the KfW Raw Materials Fund (a state-backed initiative administered by Germany’s development bank, KfW) must be leveraged for joint investments either in India or with Indian firms in third-party countries to acquire mining assets and set up processing and recycling plants. This de-risked mineral offtake can be used by both Indian and German manufacturers.

- Innovation and Standards: India has several challenges in domestic research and development (R&D), such as the lack of domestic battery testing laboratories. By partnering with German organisations, India can establish more testing infrastructure domestically that meets the local climatic requirements, while also being of a standard suitable to export to the European Union (EU). Additionally, German expertise in metallurgy and refining can be brought to India through joint ventures.

- Infrastructure Interoperability: India should align various EV standards with global good practices, such as charging protocols (Combined Charging System 2 (CCS2)). Additionally, aligning India’s Battery Aadhaar with the EU’s Battery Passport framework would open a larger market for secondary vehicle financing and battery recycling in both regions.

India’s green mobility transition cannot be managed in isolation. By operationalising existing India–Germany partnerships, India can move from the simple assembly of EV components to becoming a resilient player in the global EV value chain.

Keywords: Electric vehicles; green mobility; critical minerals; supply chains; manufacturing; net-zero; Indo-German cooperation

Q&A with authors

What is the core message conveyed in your paper?

Meeting India’s target of 30% electrification of new vehicles by 2030 and Net-zero targets emission by 2030 requires creating resilient manufacturing value chains for green technologies. India currently has a 100% import dependency on key minerals required to manufacture electric vehicle (EV) batteries, in both the ore and processed forms: lithium, cobalt, and nickel. This paper considers both the supply-side imperative of industrial resilience and the demand-side narrative of EV adoption. The paper draws on primary inputs from industry roundtables and bilateral consultations and finds that India’s green mobility transition cannot rely solely on subsidies. It requires a comprehensive industrial strategy that accounts for India’s unique market structure, which is dominated by 2Ws and 3Ws rather than cars and leverages its existing automotive manufacturing strengths to shift from ICE manufacturing to EV resilience. Thus, India needs strong international partnerships with other countries that similarly aim to reduce mineral supply risks and build domestic capacity. Germany emerges as a complementary partner and offers a clear path to de-risk this dependency through existing bilateral mechanisms.

What presents the biggest opportunity?

India cannot de-risk its EV supply chains alone and Germany emerges as a natural partner to help bridge the gap. While Germany possesses world-class automotive manufacturing expertise as well as advanced processing technologies it lacks the geological reserves for battery minerals and is currently witnessing rising energy and labour costs domestically. Conversely, India possesses manufacturing scale, a vast engineering talent pool, provides lower operating costs. Despite having reserves for many of these critical minerals crucial for its green mobility transition, India remains almost entirely import-dependant. This complementarity sets Germany apart from other potential partners who are more likely to guard their IP or leverage their supply chain dominance. The mechanisms to operationalise this partnership already exist, through platforms like the Indo-German Green and Sustainable Development Partnership and the KfW Raw Materials Fund. Hence, the question is less about building new cooperation frameworks and more about operationalising existing bilateral goodwill towards India’s most pressing supply chain vulnerabilities in mineral processing and refining.

What is the biggest challenge?

Domestic EV policies in India like purchase subsidies and production-linked incentives (PLIs) have not been able to address the supply risks in upstream mineral procurement and midstream processing, despite having domestic value-addition requirements, due to a lack of suitable local options. For India, as for the global economy, midstream processing concentration creates a major supply chain risk. Without domestic capability to process raw ores or recycle the black mass from spent batteries, India remains a price-taker in a volatile global market. It will be exposed to the weaponisation of supply chains and trade shocks. India’s import dependency, especially for EV batteries, is particularly concerning, as it has a near-total lack of domestic battery manufacturing. This includes not producing key components like cathode and anode materials, electrolytes, separators, and battery cells. Even with major improvements to its EV infrastructure, India still lags behind lithium-ion battery manufacturers in Germany or the US.

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.