The Cost Conundrum: How CBAM Could Affect the Competitiveness of EU Manufacturers

Reading Time: 6 minutesEditor's Note

The author sincerely thanks Amita Batra, Senior Fellow, and Rajat Verma, Associate Fellow, CSEP, for their insightful comments.

In the global fight against climate change, nations are stepping up their efforts with commitments like net-zero targets and Nationally Determined Contributions (NDCs). The European Union (EU) has been at the forefront of the fight against climate change. In 2005, it launched the Emissions Trading System (EU ETS) to reduce emissions of greenhouse gases in the territory, which is believed to have resulted in carbon leakage and hampered the competitiveness of EU manufacturers. As a part of the EU’s green deal, in 2023 Carbon Border Adjustment Mechanism (CBAM) in its transitional phase has already been implemented, and starting January 2026, imports of targeted sectors i.e. aluminium, cement, iron and steel, fertilisers, electricity and hydrogen, would be subject to the carbon price on their embedded emissions. It has been touted as a solution to carbon leakage and level the playing field for EU manufacturers, who contend that their competitiveness is adversely impacted by foreign counterparts operating in less stringent regulatory environments.

Full implementation of CBAM would be coupled with the gradual phasing out of free allowances allocated to the EU manufacturers under EU ETS to ensure it complies with the World Trade Organization (WTO) rules.

With regard to the potential impacts of CBAM, concerns have been raised that it may further strain international trade. Numerous studies in the literature indicate that CBAM might hurt exporters of CBAM-targeted sectors to the EU, especially from countries like China and India, which have relatively higher carbon intensity in their production processes. In addition to that, CBAM which has been imposed with the intent of boosting the competitiveness of domestic manufacturers might not yield the anticipated benefits, especially in the case of manufacturers of downstream products. This is because, the imposition of carbon price on imports of select sectors by the EU and phasing out of free allowances may lead to an increase in the cost of production of downstream sectors, as these targeted sectors are not only consumed as a final product, but are also absorbed as intermediate products. As a result, carbon price might emerge as a significant factor for the increase in cost of production and may thus affect the international trade of the EU itself. Considering the potential implications of CBAM on prices of EU’s own manufactured products too, its closer scrutiny becomes imperative.

EU’s Relevance in International Trade

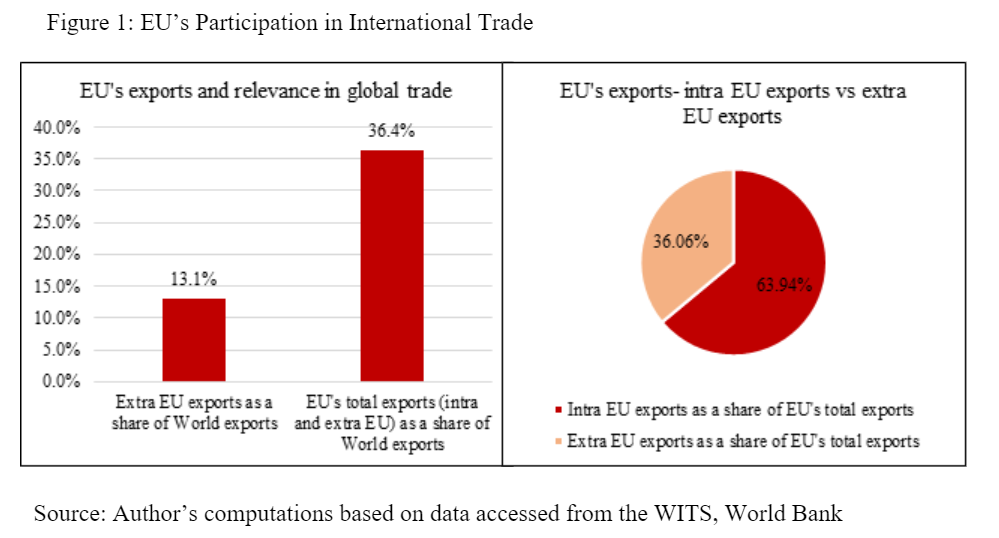

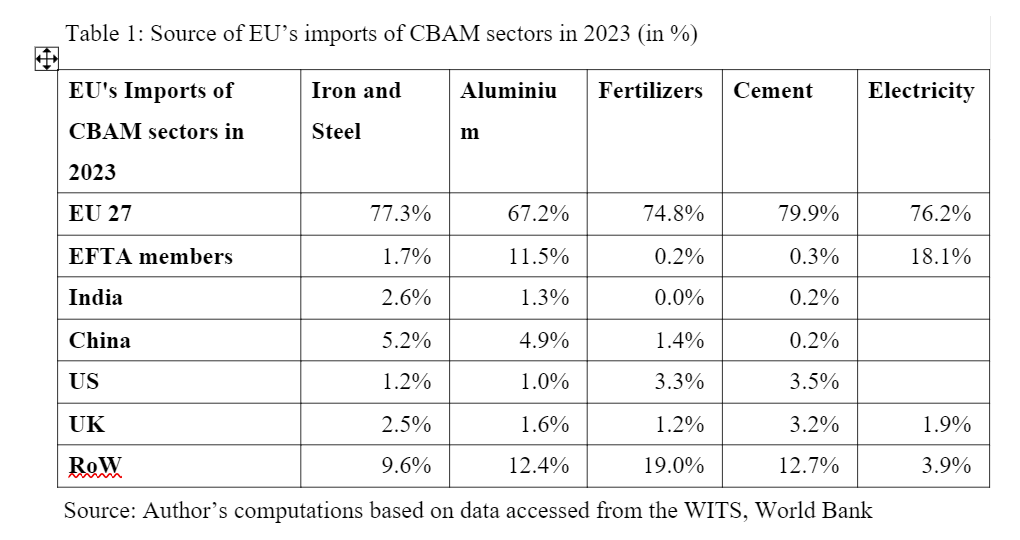

EU is a major player in international trade and ranks among the top three globally when it comes to the value of global exports and imports. In 2023, its share of world exports accounted for around 13.1% (Figure 1) which is the second largest in the world, next to China. To get a better understanding of the EU’s contribution to international trade, one may also look at the EU’s total exports i.e. the sum of intra-EU[1] exports and extra-EU exports, which account for around 36% of total exports globally. Figure 1 also shows that a significant portion of exports by EU member countries (64% of EU’s total exports) head to other EU members. This trend is more evident in case of CBAM sectors, as EU-27 imports most of these products from its member nations only (Table 1).

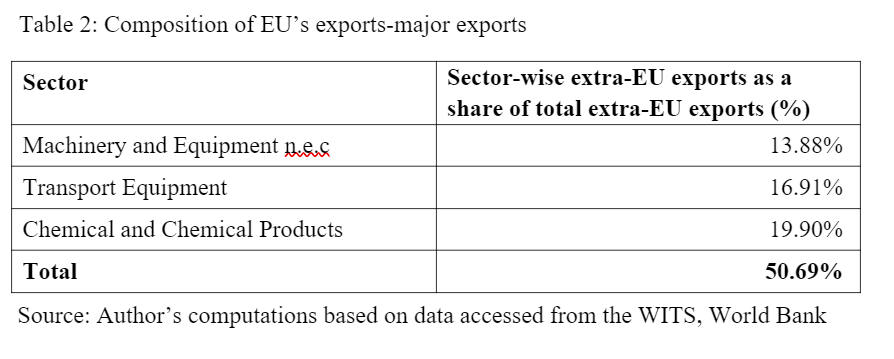

The top three sectors contributing most to the EU’s exports to the rest of the world include machinery and equipment, transport equipment, and chemical and chemical products, which in aggregate account for about 50% of the EU’s total exports to the rest of the world (Table 2). These are also the sectors which have huge dependence in terms of intermediate inputs on CBAM sectors such as Iron and Steel, Aluminium, Electricity, etc. for their production. The next section further examines the possible impacts of CBAM.

CBAM and its Unanticipated Impacts on EU Manufacturers’ Competitiveness

The implementation of CBAM will make it mandatory to pay the carbon price on emissions embedded in imports of targeted sectors while allowing a rebate for any carbon price paid domestically. The implementation and extension of CBAM to other sectors will be coupled with the gradual phasing out of free allowances given to certain domestic producers within the EU. In the case of Iron and Steel, Fertilizers, Cement and Electricity, almost 3/4th of imports of these targeted sectors by the EU come from its member states only (Table 1), suggesting that gradual removal of free allocation of allowances from these sectors might result into an increase in their production cost. Imports of these CBAM products from other trading partners like the UK, USA, China, India, etc. would experience imposition of carbon price under CBAM as scope and carbon prices under existing carbon pricing policies of UK, China or USA are not comparable with the EU’s carbon pricing policies.

The duo of imposition of carbon price on imports of select sectors and removal of free allowances is expected to push up the production cost and prices of targeted sectors in the European market.

Since these targeted products are also absorbed as intermediates for further processing, an increase in the price of these intermediates is expected to increase the cost of production of downstream sectors too, which in turn will have an impact on the cost of production of further downstream sectors.

As long as the scope of CBAM is not being extended to cover emissions embedded in downstream sectors, CBAM in its present form may hamper the competitiveness of EU manufacturers disproportionately. ADB (2024) also suggests that while CBAM may help fight against carbon leakage due to EU-ETS by bringing production back to the EU, downstream producers in the EU however may shift some of their production outside of the EU because of CBAM.

As per the TiVA 2023 database, the value added as a share of total production by the Transport equipment and machinery sectors within the EU was around 28% and 37% in 2020, highlighting the huge dependence of the two sectors on upstream sectors including CBAM sectors. To better understand how CBAM sectors like steel may impact the EU manufacturers in downstream sectors, we may further look into how steel is consumed across various economic activities in their production processes. As per EUROFER (2022), 19% of the finished steel was consumed by the automotive and other transport sectors, and almost 15% went to the mechanical engineering sector. These are also the sectors which contribute to the EU’s total exports the most (around half of the EU’s total merchandise exports to the world outside), suggesting that an increase in the price of steel due to CBAM and phasing out of free allowances is expected to have a significant impact on the cost of production and hence exports of sectors like automotive, mechanical engineering, etc. which in turn may hamper the competitiveness of manufacturers of these sectors. Since, the EU is among the world’s largest producers of Automotive (European Commission, n.d.) and the largest producer and exporter of machinery (European Commission, n.d.), and the two sectors contribute significantly to the EU’s value addition, output, employment, trade and have an important multiplier effect on the economy, an adverse impact of CBAM on manufacturers of these sectors may have huge ramifications.

While CBAM may offer protection to Europe’s green producers of select sectors by bringing their production back to the EU, downstream manufacturers are left vulnerable to the unintended consequences of higher costs, as they might have to face the prospect of soaring production costs, which may threaten their competitiveness. This analysis does not account for potential implication of the increasing efforts taken by the companies globally to decarbonise their production processes, which are expected to reduce emissions and, consequently, may lessen the impact of carbon price on targeted sectors due to CBAM and phase-out of free allowances. This suggests that the true impact of CBAM will also depend on the cost of mitigation. Although the actual effects of CBAM on EU manufacturers remain uncertain and are yet to be fully realised, as CBAM in its definitive regime[2] is going to be implemented, it is crucial to assess if the anticipated economic benefits of levelling the playing field for EU manufacturers will outweigh the potential adverse impacts. With more countries, including the UK, and Australia announcing their intention to implement similar CBAM mechanisms, thoughtful consideration of the potential impacts and trade-offs involved is essential.

References

ADB. (2024). Asian Economic Integration Report 2024: Decarbonizing Global Value Chains. https://www.adb.org/sites/default/files/publication/945596/asian-economic-integration-report-2024.pdf

EUROFER. (2022). EUROFER, 2022, European-Steel-in-Figures-2022-v2. https://www.eurofer.eu/assets/publications/brochures-booklets-and-factsheets/european-steel-in-figures-2022/European-Steel-in-Figures-2022-v2.pdf

European Commission. (n.d.). Mechanical engineering. https://single-market-economy.ec.europa.eu/sectors/mechanical-engineering_en

European Commission. (n.d.). Automotive industry. https://single-market-economy.ec.europa.eu/sectors/automotive-industry_en

FOOTNOTES

[1] Intra-EU refers to all transactions occurring within the EU, whereas Extra-EU refers to transactions with all countries outside of the EU.

[2] CBAM in its definitive regime (starting 2026) will become fully operational, as EU importers will be required to declare the emissions embedded in their imports and surrender corresponding number of CBAM certificates.

Shifali Goyal

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.