Breaking Down the Gap in DisCom Finances: Explaining the Causes of Missing Money

Reading Time: 7 minutesEditor's Note

This Impact Paper is a part of the twin studies by CSEP on DISCOMs financial gaps.

Read the second paper "Getting India's Electricity Prices "Right": It’s More Than Just Violations of the 20% Cross-Subsidy Limit"

Articles in the Media:

Power Sector Needs a Regulatory Overhaul - Hindustan Times

Discom Gaps Need Urgent Systemic Fixes - Hindustan Times

DOWNLOADS

Executive Summary

1.1. DisComs are Regulated Entities who Shouldn’t be Loss-making, if they Perform

Electricity distribution companies (DisComs) are the last leg in the vertically integrated chain of electricity sector that starts with generation. In India, they are also responsible for retailing power to consumers. Independent State Electricity Regulatory Commissions (SERCs) set retail tariffs (prices) meant to balance DisCom viability with consumer interest. Unfortunately, DisComs have sustained substantial financial and electricity losses for many years.

Barring Mumbai, which has retail competition, electricity distribution in India is a regulated, geographic monopoly; and DisComs operate on a costs-plus regulation model that is based on performance norms. If they perform, in theory, they should make the specified statutory rate of return. So, are their financial losses thus just a failure of performance? (Tyagi & Tongia, 2023) (in press)

In this paper, we comprehensively analyse DisCom finances using a long time series that aims to examine and answer the following questions using disaggregated and bottom-up numbers:

1. What are the operational losses of DisComs and what are their causes?

2. How much of the gap between costs and revenues is apportionable to different stakeholders (DisCom, regulator, and state government) or not apportionable?

3. How do the operational (annual) losses link to the DisCom balance sheets?

4. What are the steps needed to fix the financial health of the DisComs, especially for a turnaround (on the basis of operational basis viability)?

This paper builds on a complementary analysis by Tyagi and Tongia (2023) (in press) that compares the planned costs and revenues as per ex-ante tariff orders versus the actual realisations ex-post. They found that ex-ante retail tariffs (consumer prices) are set with virtually no gap between costs and revenues. However, in practice (after the year goes by when the tariffs are in force), an enormous gap appears, of around Rs 1.64 per kWh for FY2018-19 (prior to the provisioning of any grants or other income not planned by regulators).

We extend this analysis across 15 years, covering virtually all of India’s public DisComs, integrated utilities, and power departments.[1] By examining financial details over time, we automatically capture true-up adjustments, which are the formal process for reconciling allowed changes from tariff order plans through subsequent tariff revisions. Failure to perform, such as lower-than-notified operating efficiency, is not meant to be adjusted in trueup tariff orders.

1.2. Despite Relative Improvements, Large Financial Gap Remains

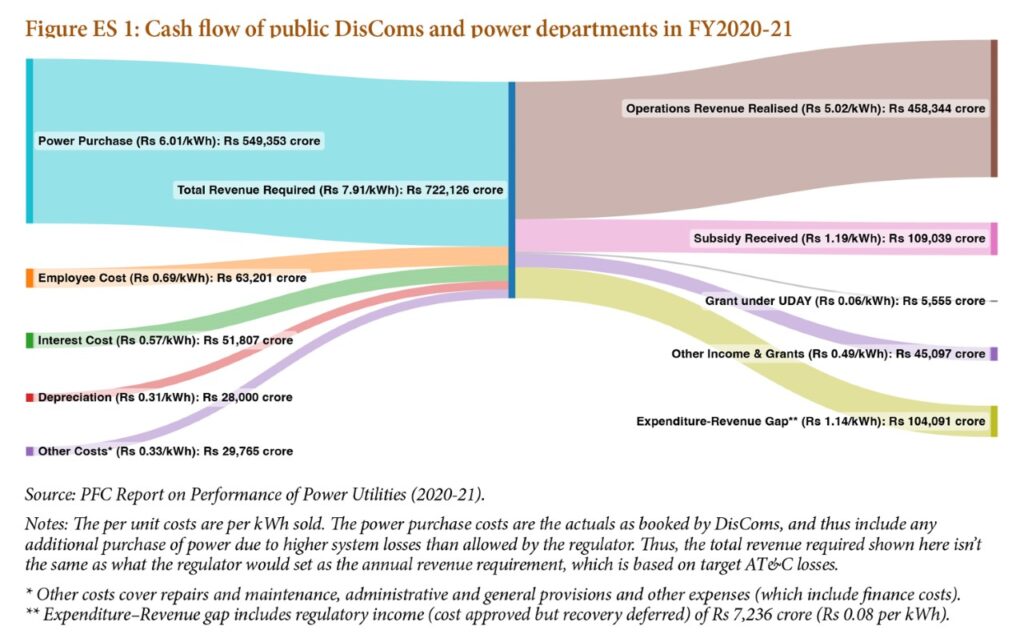

Over a 15-year period, with few exceptions, all DisComs have had revenues lower than costs. Consumers don’t pay all the costs directly, and state governments routinely offer tariff subsidies on top of the regulator-set prices (tariffs). Outside these combined revenues, DisComs also rely on significant Other Income and Grants, but this still left a cash-basis gap of Rs 1,04,091 crore in FY2020-21, or Rs 1.14 per kWh sold (Figure ES 1).[2]

Our focus is on understanding the breakdown of this financial gap. Explanatory factors include DisCom performance lapses, non-payment of subsidies, and regulators explicitly not setting a high enough tariff (instead, creating an IOU called a ‘Regulatory Asset’).

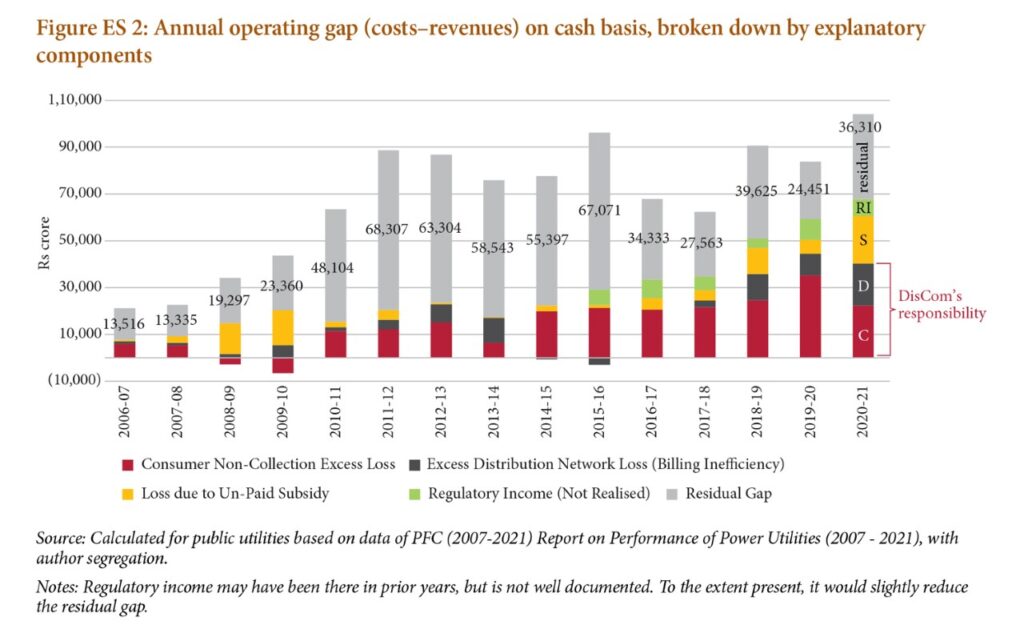

Conventional wisdom is that losses are overwhelmingly due to DisCom non-performance. We find this to be incorrect. While they have failed to meet performance targets, both in terms of billing and collection efficiencies, this amounts to only about 30% of the cumulative gap over 15 years. Unfortunately, DisCom non-performance has grown in recent years. Even within noncollection from consumers, a substantial fraction (estimated at over a third and perhaps closer to one-half) is from governmental entities/consumers. We segregate non-payment of subsidies from the widely cited measure AT&C (aggregate technical and commercial) losses since this is not the fault of the DisCom. Subsidy nonpayment and the creation of regulatory assets together explain 13% of the cumulative gap, but this still leaves a “residual gap” of about 59% which is not attributable to any of these causes. Figure ES 2 shows the split of the financial gap’s components over time.

This residual gap effectively means that we have a tariff that is too low to cover costs even after accounting for the factors above, but why this happens is not conclusive. Questions that need to be considered include: Is it because DisComs are not asking for the right tariffs, including in the true-up (reconciliation) process? Are they being denied by the regulator? Or are there deeper issues in the process? We identify additional partial causes, such as the two-year delay for true-ups, which creates a pipeline problem and carrying costs for the DisComs. However, it would be wrong to place primary responsibility on the DisComs for this residual gap.

1.3. Operating Financial Gaps Accumulate in the Balance Sheet

Not only are direct DisCom failures only a fraction of the operating gap, a much larger share of the lapse comes from consumer non-collection, which, unfortunately, is growing (even after the leeway given for FY 2020-21 due to the effects of COVID-19). The “good” news is such a gap isn’t lost forever; consumer non-collection is theoretically recoverable and remains on the balance sheet as a trade receivable. Balance sheets also show “regulatory assets,” but, surprisingly, don’t visibly separate subsidy non-payment!

As we break down the numbers, the true financial picture is better seen in cash flow accounting, since accrual-based accounting, like what the Power Finance Corporation (PFC) compiles annually, (PFC FY21 report indicates a few cash based statements for recent years) understates the problem. These show revenues as-booked, but much of the cash doesn’t come into DisCom coffers, showing up as an asset like a receivable instead.

Because DisComs are cash-strapped, they are forced to resort to various coping mechanisms. First, they delay payments to suppliers, both generators (Rs 2,52,736 crore on the balance sheet[3]) and other short-term dues to vendors (Rs 2,53,040 crore), some of which entail penalties. They also are forced to take on more debt, and we find that States have pumped in significant equity. Unfortunately, much of this isn’t for asset creation, but simply as a fill-up. Regulators have routinely disallowed returns on the full equity base, and the booked return on equity (RoE) has fallen to 3.28%.[4] Even worse, in a few cases, DisComs are waiving RoE, ostensibly to keep tariffs low. This is a poor and non-scalable means of lowering consumer tariffs. This is nowhere near the hurdle rate of 10% notified by the Ministry of Finance for calculating financial internal rate of return in respect of projects which have identifiable stream of financial returns. Accumulated deficits are enormous, in lakhs of crores of rupees, and visible on the balance sheet as a part of the total equity. These have, by far, eroded the (book) equity. These deficits closely track the annual “residual” operating gap we identified plus the unpaid subsidy—other components of the operating gap[5] show up elsewhere on the balance sheet (as trade receivables and regulatory assets of Rs 2,34,072 crore and Rs 45,907 crore, respectively, for the public DisComs covered). Billing efficiency losses were worse than targets, by 3.53% in FY2020-21, and are a permanent loss that doesn’t remain in the books.[6]

1.4. Fixing the Problem: Without an Operational Turnaround, a Balance Sheet Clean-up won’t Last

There has been a range of instruments used to bail out or prop up DisComs over the decades. While some have focused on fixing the balance sheet, many were conditional on achieving lower losses, requiring a reduction in the AT&C losses or even eliminating the ACS-ARR gap (‘average cost of supply’ minus ‘aggregate revenue realised’). However, as Tyagi and Tongia (2023) (in press) first showed, the ACS-ARR gap at the time of tariff order setting is virtually non-existent. Much of

the problem happens ex-post, and the subsequent true-up processes are not effective.

Fixing operating problems is the first step, and seven utilities are already operationally cash positive (based on FY2019-20 data). We find that 18 out of the 43 public distribution utilities studied for clean-up[7] can resolve the gap by “merely” addressing the known components of the gap (excess billing losses aka excess distribution losses, consumer non-collection, subsidy non-payment, and creation of regulatory assets). We recognise that this is easier said than done. The harder challenge is figuring out how to fix the remaining 18 DisComs that have a residual gap and need more fundamental changes. Addressing regulatory assets requires a tariff rise, while other known components require increased compliance. However, addressing the residual gap will also require a tariff increase. For most DisComs, this should be manageable, but in a few cases, the required rise will be unreasonably high (when benchmarked to average annual tariff rises, which are typically

up to 5% or near about inflation).

Operational improvements can improve the balance sheet (or at least prevent further deterioration). The central government has already initiated a range of steps to reduce operational losses and improve cash flows, many of them after COVID struck, ranging from liquidity support, schemes for paying off generators, installation of smart meters, and oversight of timeliness for statutory regulatory and discom filings of tariff petitions, orders, and accounts. However, these do not address the issue of the residual gap in tariffs.

This study also investigates the other direction, i.e., the balance sheet clean-ups that can help fix the operational gap. We focus on unpaid subsidies and regulatory assets since addressing trade receivables from lakhs or perhaps millions of consumers is a diffuse problem that cannot be fixed by policy (except dues from governmental consumers, both state and local). These components are also ostensibly not the fault of the DisCom. With this cash in hand, it could be used to repay generating companies (GenCos) or other liabilities, which would lower carrying costs and improve operations. Unfortunately, adding this step doesn’t help too many more DisComs cross over into profitability as the residual losses are too high.

We conclude with an analysis of both high level and specific suggestions in order to move the needle towards closing the gap componentwise. The first step is to improve accounting and nomenclature, and introduce greater standardisation in processes (including the segregation of AT&C losses into its components). This applies not just to annual statements but also to balance sheets. We also need to revamp the tariff-setting process, especially the true-up process, to close the residual gap. Lastly, we examine a range of additional issues outside the direct issues of tariffs and tariff setting that need to be addressed to achieve operational viability. These include improvements in planning (especially for power procurement but also in terms of expected consumer mix over time), and in DisCom management. Planning will be especially important in a future with increasing decarbonisation and market-structure redesign. For example, consumer-owned solar (rooftop solar) not only changes the net demand pattern seen by the utility (with an additional time-of-day implication), but it also changes their ability to rely on cross-subsidies from premium customers.

Ultimately, several improvements will rely not only on managerial efficiency but also on addressing issues of political economy and politics. This isn’t just for raising tariffs, but even for enforcing existing norms and regulations. The good news is that the problems aren’t universal or equal. By focusing on relevant components of the gap more intensely, the problem can be addressed in about half the DisComs, more so without significant tariff rises. However, for several DisComs, we may need external support and new or more innovative instruments. The residual gap identified and quantified in this paper is a serious challenge, not merely because of its vast scale, but also because fixing the known causes of the financial gap is “not enough”. The sector needs—and deserves—new kinds of regulatory principles and processes.

FOOTNOTES

[1] The basis for the a priori (tariff order) benchmarks was manual compilation across the DisComs, while post facto results can be found in Power Finance Corporation (PFC)’s report on DisComs performance, DisCom filings with Ministry of Corporate Affairs, and Audited Annual Reports.

[2] This figure differs from some official publications because we correct for “regulatory income”—that which isn’t received but leads to Regulatory Assets. We also base the kWh calculations on the units sold, instead of units received by the DisCom.

[3] By the end of FY2020–21 in public DisComs.

[4] Aggregate FY2018-19 value for 39 key public DisComs for which we have consistent time series data.

[5] With respect to public DisComs, integrated utilities, and power departments (excluding private DisComs) by the end of FY2020-21.

[6] From a DisCom financial perspective, what matters is the relative performance compared to billing efficiency targets and not the absolute billed energy losses. We have manually compiled the targets across DisComs over the years to determine the performance gap.

[7] Clean-up analysis focused on 42 public DisComs and integrated utilities plus one power department (totalling 43), which collectively sold 89.1% of the units sold in FY2020-21.

Rahul Tongia

Rajasekhar Devaguptapu

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.