Getting India’s Electricity Prices “Right”: It’s More Than Just Violations of the 20% Cross-Subsidy Limit

Reading Time: 8 minutesEditor's Note

This Impact Paper is a part of the twin studies by CSEP on DISCOMs financial gaps.

Read the second paper "Breaking Down the Gap in DisCom Finances: Explaining the Causes of Missing Money"

Articles in the Media:

Power Sector Needs a Regulatory Overhaul - Hindustan Times

Discom Gaps Need Urgent Systemic Fixes - Hindustan Times

DOWNLOADS

Executive Summary

Retail Electricity Pricing is a Delicate Balancing Act for Regulators

Electricity is one of the most important forms of energy in India, and is growing in share of total energy, especially as India strives to decarbonise. Until the late 1990s, integrated State Electricity Boards (SEBs) ran the entire electricity value chain. Over about 15 years, these were corporatised and mostly unbundled, creating separate public companies down the supply chain of electricity generation, transmission, and distribution (including consumer retailing). Almost all Distribution Companies (DisComs) remain State-owned, except for the few regions or cities that were historically private, or two States that privatised their State DisComs. Unfortunately, most DisComs, especially public ones, perennially suffer heavy losses, both of energy and of money. As DisComs are the last leg in the chain of electricity supply, their viability impacts the viability of the entire chain, and struggling DisComs are also a risk for India’s climate change ambitions.

Distribution of electricity to consumers in India is a regulated service, with DisComs being offered a geographic monopoly over a region with regulated rate of return.[1] State Electricity Regulatory Commissions (SERCs) set consumer prices (aka tariffs) with two criteria in mind—to cover DisCom costs and to offer social welfare redistribution to protect the poor. The latter is through a system of cross-subsidies, where some consumer groups pay less and others overpay. This is distinct from any subsidies a State government may wish to offer, but such subsidies are meant to be outside the purview of regulators.

In this paper, we examine the processes and outcomes of regulatory tariff-setting, to see how well the criteria are met. In theory, as long as DisComs perform as per the operational targets set by SERCs, they should not be loss-making.

The SERCs are solely responsible for the process of retail tariffs, guided by the National Tariff Policy (which is enshrined in the Electricity Act 2003). The National Tariff Policy limits the cross-subsidy

price variation for almost all consumer categories like households, industrial, commercial, etc. to ±20% of the Average Cost of Supply (ACoS). However, many regulator-set tariffs do not comply with the policy. In this paper, we quantify the non-compliance and examine possible causes and implications of the violations.

The process of setting tariffs spans several years and is broadly divided into two parts—ex-ante and ex-post. When setting initial tariffs ex-ante through the initial Tariff Order, the regulator must make a range of assumptions on power procurement costs, consumer mix, volumes of sale, etc. Ex-post, there are inevitably deviations from plans, which are meant to be reconciled through a subsequent tariff True-Up process[2] that reconciles and compensates the Discom for legitimate gaps. We show that this is an important element of DisComs’ financial performance.

Bottom-up Cash-basis Analysis of Revenues and Costs Shows a Worse Picture than Conventional Wisdom

This paper studies the entire chain and focuses on cash-basis accounting, which is distinct from the typical accrual-basis accounting followed in most official power sector documents and mandatory for corporate audited reports. Accrual accounting is based on booked values, which reflects the money that is promised or due, but the actual cash received is often much lower. Thus, our analysis shows a graver picture of DisCom finances.

We compare compiled governmental data sources with 60 DisCom Tariff Orders across India to quantify the costs and consumer-wise segment revenues. We calculate the cross-subsidies per segment after factoring in revenues from State government tariff subsidies. We also compare the ex-ante costs and revenues with ex-post, and apportion the changes across the respective stakeholders (DisComs, State governments, consumers, and regulators). We extensively use financial year 2019 (FY19) data as it was the latest available year for which audited annual reports data were available in the public domain at the time of analysis. This is also the last period not impacted by COVID-19, which has since, not only impacted sales but also consumer collection.[3]

Examining the regulatory process and finances, we find Tariff Orders (ex-ante) have virtually no losses, i.e., the expected revenues match the costs, but ex-post, there are significant changes, ones that are mostly one-sided and lead to a financial loss.

Our analysis is per DisCom, which is important given the wide heterogeneity across India.

Even before considering changes in revenues and costs ex-post, the ex-ante Tariff Orders for FY19

set by regulators have more than 50% of electricity units with tariffs exceeding the ±20% crosssubsidy limit. To bring tariffs within compliance of the ±20% limit, a combination approach would be needed—lowering tariffs for some overpayers, and raising tariffs for some underpayers. For those paying below 80% of the ACoS, tariffs would need to rise by an average of Rs 1.17/kWh, which corresponds to a 30% increase from the prevalent tariffs. Such a rise is not easy when compared to the historical average tariff rise trend, which had a 5% compound annual growth rate (CAGR) over the prior five years (FY14-19), roughly in the range of inflation.

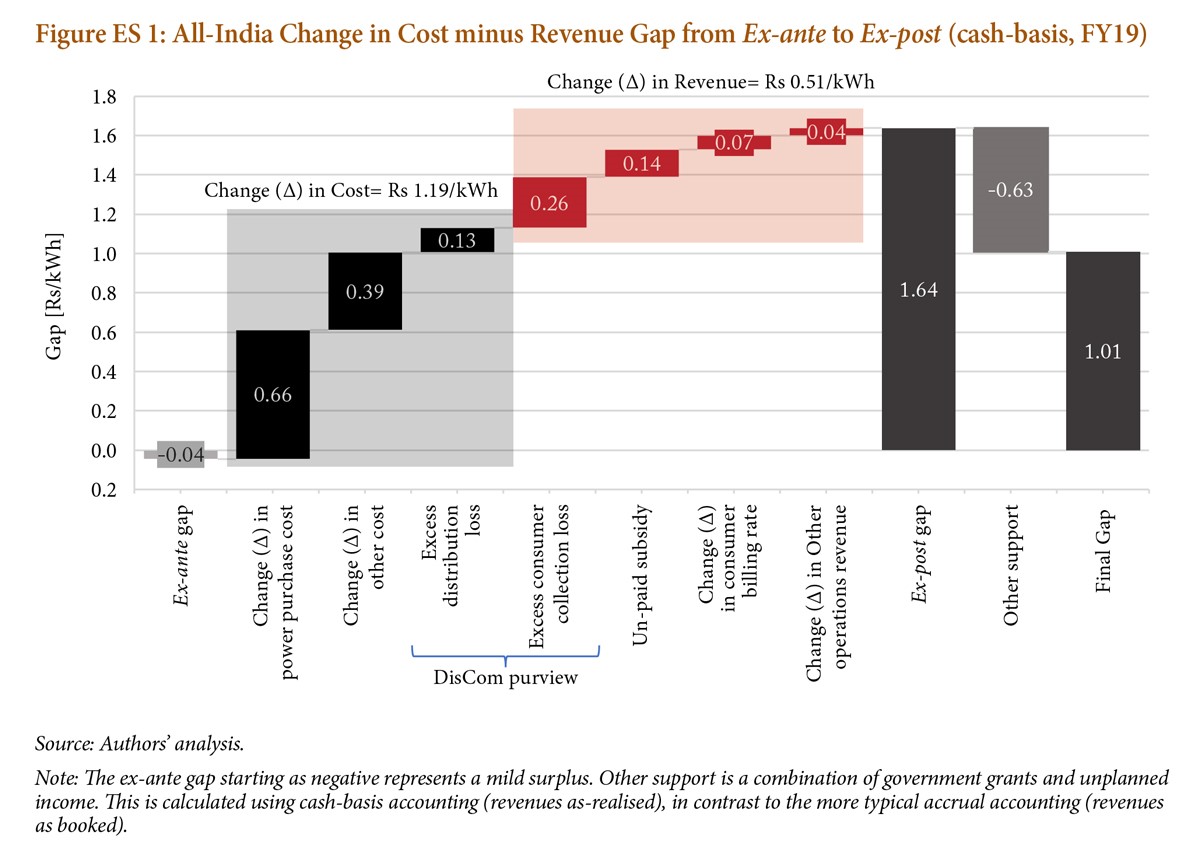

Ex-post, costs rise across most DisComs compared to ex-ante projections, by 19% on average. This rise in costs is paired with a fall in average billing rate (ABR, or revenues)—varying by DisCom. Put together, these change the finances from no losses ex-ante (actually, an average 0.5% profit, or 0.04 Rs/kWh) to a 22% gross financial gap for FY19 ex-post, or Rs 1.64/kWh financial loss. This gap is only partially offset by unplanned income and government grants (including Ujwal DisCom Assurance Yojana [UDAY] grants) of Rs 0.63/ kWh, which lowered the net financial gap to 14%, or Rs 1.01/kWh. This shift in costs and revenues means the true cross-subsidy is even higher than as per Tariff Orders.

The ex-ante to ex-post change is substantial. There are multiple factors at play and stakeholders who are respectively accountable. These are broken down in Figure ES 1.

On the cost side, the largest change in absolute terms comes from an increase in power purchase costs, followed by a rise in “other costs” that are primarily financial and operational. Higher distribution network losses than the normative level as per Tariff Orders, also raise costs. Because of such distribution losses, which are a subset of the aggregate technical and commercial losses (AT&C), the DisCom needs to procure more power than planned to supply a given load. In aggregate, costs rose by Rs. 1.19/kWh.

On the revenue side, a substantial fall in cash revenues comes from DisCom failures to collect money from consumers, combined with non-payment of promised subsidies by State governments. Both of these are also components of AT&C losses. Some money is also not realised because regulators don’t set a sufficient tariff, postponing a tariff rise by creating a “Regulatory Asset” instead where the utility doesn’t get money in the current year’s tariff. In addition, on average DisComs earned less than projected from the sale of power and other network charges (such as wheeling charges, open access charges, etc.). A significant part of this is due to a change in how many units of electricity are sold to which type of consumer. Put together, the average revenues on a cash-basis fell ex-post by Rs 0.51/kWh.

If we attempt to apportion responsibility for the changes, some factors could be considered random, such as changes in consumption patterns, but a counter view is DisComs should do a better job planning and projecting demand. Without proper projections, they are also likely to get power procurement wrong, another cost ultimately borne by consumers.

Conventional wisdom holds the poor performance of DisComs as the cause of their financial losses, specifically high AT&C losses. However, only two components of AT&C losses—excess distribution network losses and consumer non-collection—are directly in the purview of DisComs. These losses were only 25% of the ex-post financial gap in FY19. Non-payment of subsidies—officially part of AT&C losses—was due to the State government and was 8% of the financial gap. Even put together, addressing such causes of the gap will not close the overall financial gap that DisComs face.

Most other components that shifted should, in theory, be reconciled through the True-Up process. Even if such ex-post financial gaps were to be recovered, these would take several years to materialise. More importantly, we found that True-Ups only capture a small fraction of exante to ex-post differentials even focusing just on “allowed” differentials that aren’t based on the fault of the DisCom or other stakeholders like the State government (in case they don’t pay promised subsidies in full). In FY19, Tariff Orders embedded just 0.07 Rs/kWh of historical True-Ups as part of the cost structure, or close to only 1% of costs. A complementary paper by Devaguptapu and Tongia (2023) examines such issues over a 15-year time series.

Fixing the Gap And Cross-subsidy Limits Will Ultimately Require a Tariff Rise

Improved operations (e.g., lower AT&C losses) are welcome and important, but will only address a small portion of the financial gap. Closing the gap will require wide a range of steps, including better planning and a streamlined True-Up process. However, the ultimate need will be for higher tariffs than the present ex-ante tariffs, but higher tariffs are unwelcome across the spectrum of consumers and State governments.

Higher tariffs will also be required to keep cross-subsidies within statutory limits. This is a pressing issue not just to comply with the law but also because a system with excessively high prices for so-called “paying customers”—primarily commercial and industrial users—creates several challenges. First, this hampers economic growth and global competitiveness. Second, the growth of such consumers is lower than the growth in sales volume we see from lower-end consumers, putting pressure on the redistribution equilibrium. Lastly, thanks to both technological and regulatory changes, such paying customers are the ones most likely to exit or at least diminish their offtake from DisComs through a combination of self-generation, such as rooftop solar and third-party sales like under Open Access norms.

Fixing the financial gap through improved tariffs is also critical because cash strapped DisComs are forced to rely on a range of coping mechanisms that include delaying payments to their own suppliers, including generators. This propagates upwards all the way to delayed payments for coal, railways, and, ultimately, the banking sector.

If we dig deeper, true cross-subsidies are likely higher than most calculations show. Present norms and our base analysis calculate crosssubsidies based on the ACoS, but the true crosssubsidies are likely even higher if we properly account for differences in cost to serve. Bulk consumers (“high tension” or HT consumers) are cheaper to serve, and so if we re-calculate cross-subsidies with such data (available for a few states), we find an even higher cross-subsidy. We can also estimate differences in costs to serve by using retail electricity pricing data from the United States (US), across consumer categories, where industry has the lowest tariffs, followed by commercial, and with households paying the most. Recalculating cross-subsidies based on such differential costs to serve, would raise the levels of cross-subsidies by tens of percent.

There are a range of steps that should be taken to help the tariff process, distinct from setting more cost-reflective tariffs. DisComs clearly need to lower AT&C losses, but we also need far better operational and financial data, especially on the revenue side. We need more standardisation of consumer categories, slabs, etc., and more granular breakdowns within AT&C losses. This is important because different components of AT&C can only be fixed by different instruments—better management versus investments in the physical network. Even billing today isn’t as scientific as one would expect. It is well known that many irrigation pumpsets are not metered, instead relying on assumptions for measuring agricultural supply. This creates the space for fudging data (and hiding losses) and simultaneously asking for more subsidy, given agricultural supply is often subsidised by the State. What is less understood is how many other consumers don’t have proper monthly billing—many residential consumers only get estimated bills, that too inconsistently. The planned rollout of smart meters should help this process.

Regulators have the ultimate responsibility for setting tariffs right, but DisComs also have a strong role to play. Improved planning would not just help to set prices right (where plans should more closely match actual realisations) but also lower costs by optimising generation procurement and network investments. Proper pricing, which may require increasing tariffs, needs crossstakeholder support, especially from the State government. There is a limit to how much State governments can subsidise consumers, and the interplay between subsidies and cross-subsidies is a hidden barrier to rationalised tariffs. Artificially low regulator-set tariffs for subsidised consumers (like agriculture) may reduce the subsidy burden on the State, but this just means either someone else is paying, or that the DisCom bears the brunt of any leftover gap, more so in the ex-post financial realisation. The present equilibrium of both cross-subsidies and high ex-post losses cannot be sustained and needs prompt rectification.

FOOTNOTES

[1] Only the city of Mumbai has retail competition with multiple DisComs that have overlapping geographic coverage. Throughout India, bulk consumers (above 1 MW in size) are allowed to choose their supplier through Open Access rules as per the Electricity Act 2003. They still need the DisCom’s distribution network for last-mile connectivity.

[2] True-Up is the process of reconciling DisCom expenses based on ex-post audited reports and subsequent tariff petitions/notifications. True-Ups disallow poor performance by DisComs, such as failing to collect dues from consumers, but there are a range of “allowed” ex-post changes for factors like changes in power procurement cost or in consumer patterns that the regulator should allow for recovery through subsequent tariffs. Such shifts are carried forward as part of the aggregate revenue

requirement of the subsequent year.

[3] The March 2020 lockdown impacted consumer collection for bills raised as early as February 2020.

Rahul Tongia

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.