India’s Next Decade: Some Predictions, Some Speculations

Reading Time: 17 minutes

Most of our debates focus on the here and now: issues such as the Covid-19 challenges, border disputes with China, the Agriculture Bills, phone hacking by Pegasus, or the banking sector’s continued bad debt crisis. However, the most important challenges – as well as the most promising opportunities – are what economists call “beyond the horizon” problems. Thanks to our evolution from the reptilian brain and our hardwired survival instinct, we systematically overestimate the magnitude of current challenges and underestimate the challenges that are far away.

This year is the thirtieth anniversary of India’s much vaunted economic reforms. Much has changed since then. In the early decades of independence, India had internalised poverty. In debates whether subsidies or infrastructure should be government priority, because of resource constraints and the zero sum nature of the expenditures, often-times subsidies got priority and long term investments lagged. The “Hindu rate of growth”, which translated to 1.3% per capita growth came to define India’s post-independence performance in early decades, (see Virmani, (2004))[1]. Today’s India – in its reality and in its aspirations – is dramatically different. Ralph Waldo Emerson famously said: “The years teach much which the days never know.” My corollary: the years hide stories that only decades can tell.

This essay will attempt to look a decade ahead. I will cover a broad range of issues that I believe can be game changers for our country. Navigating these will require not just sound rational analysis, but also political will. And even more, it will require a preparation of society’s diverse constituents. Taken together, these will propel us forward. As we dwell on the decade ahead, it will be useful to recall Abraham Lincoln’s prophetic insight: “The best way to predict your future is to create it.”

While there will be inevitable swings in economic conditions, there is a strong unidirectional tailwind that is extremely favourable. I call it the operating leverage of the Indian consumer. For a majority of Indians, out of every Rs 100 of annual income, Rs 80 gets spent on day to day expenses. Only the remaining Rs 20 is discretionary income. If Indian nominal wage growth is 9%[2], which is what the average has been, and if one deducts 4% inflation from this, the real wage growth would be 5%. In real terms, median income increases to Rs 105 annually. However, the median discretionary income goes from Rs 20 to Rs 25; that’s an increase of 25%. We have millions of Indians crossing this threshold, where they have nominal wage growth in the 8-10% range, but in real terms, their discretionary income is growing at 20%.

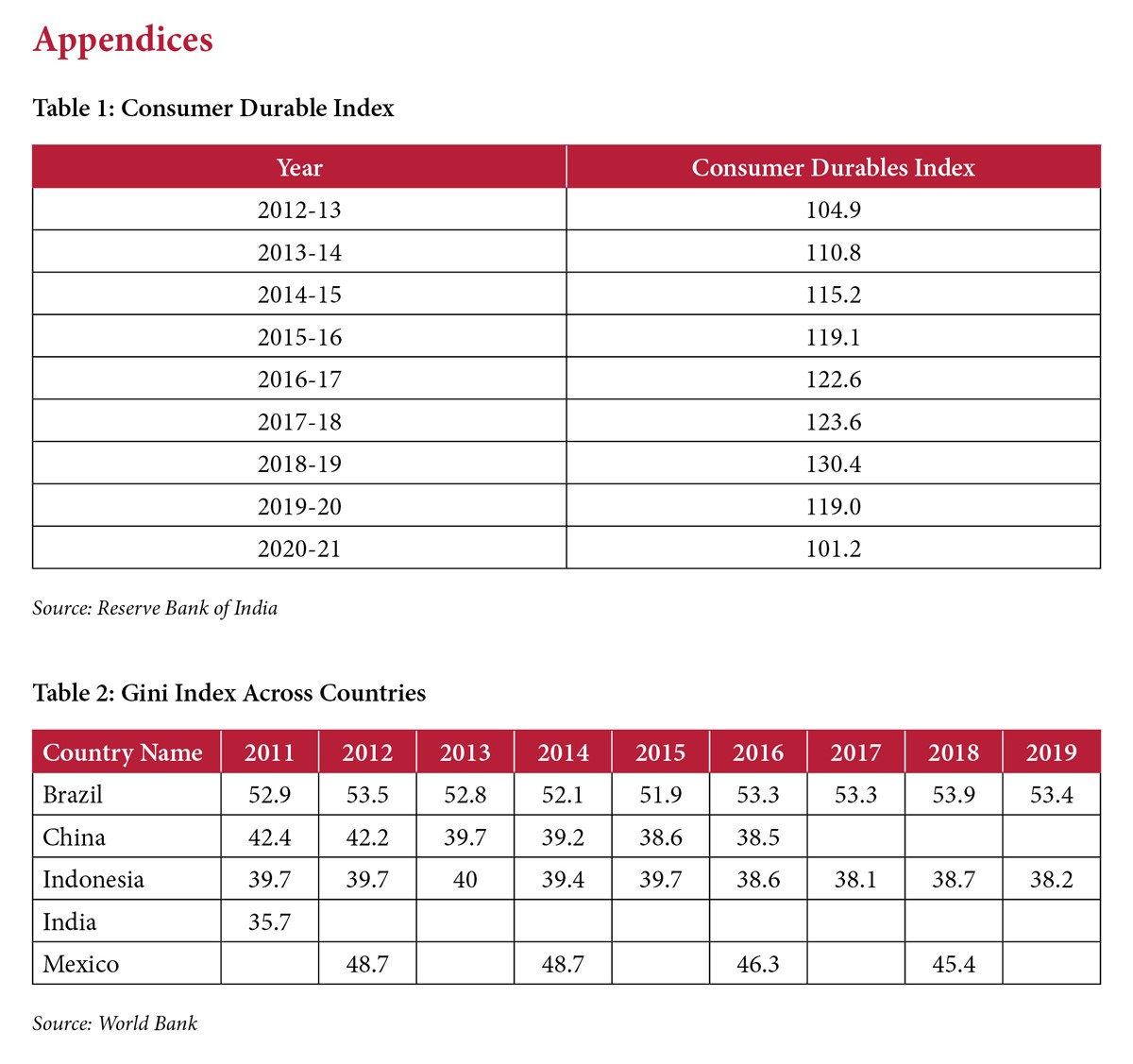

Business cycles can subdue this trend only somewhat over the short term. Over the medium term, and certainly over the long term, this trend will stay on course. The results of this are quite profound. Here’s a sample: Private general insurers have grown 18.5% and health insurers 21.2% in the decade of 2010-2020[3], on the back of increasing market penetration and shift of market share from public sector companies to private insurers because of better quality of their services. Barring the Covid-19 disruption, advertising growth—a direct consumer proxy—has tracked 12% annualised growth over the past decade[4]. Consumer durables have witnessed a 20% growth from 2012-2020. Company-specific numbers show similar trends: Telecom company Jio has grown its wireless subscribers from 186.6 million in end 2017-2018 to 387.5 million at the end of 2019-2020[5] and its aggressive pricing has made India’s data consumption 11.96GB per subscriber per month on average in 2020 (TRAI, 2020), not just the highest in the world but more than 2x that of the US levels. In the past 20 years, electrical goods company Havells has increased its revenues almost 100x and its profits more than 300x, and as investors have come to realise its potential, its market cap has jumped 6,000x since its listing in 1994. (Just as a fun comparison, since Amazon’s IPO in 1997, its market cap is up 4,000x till date, making Jeff Bezos the richest man in the world.) All of this has one common theme: the Indian consumer. While there is some criticism that Indian purchasing power is limited, effectively, consumer markets are smaller than what top-down analysis shows, and market segments are saturating fast, and my own sense is that there is plenty of headroom. 2030 will see more of the above.

In the top ten industries producing India’s billionaires, the two largest contributors are information technology and pharmaceuticals, both of which are primarily global-contracting sectors.

The mix of India’s billionaires points to the consumer boom. Historically, as domestic markets have been small, exporters have been the darlings of industry. In the top ten industries producing India’s billionaires, the two largest contributors are information technology and pharmaceuticals, both of which are primarily global-contracting sectors. Most of the rest are consumer goods and related sectors: fast moving consumer goods, automotive, food and beverages, textiles and apparel. And in a divergence from its Asian peers, in India, real estate ranks 10th and infrastructure does not feature on the list at all.

This consumer-centric gravitational pull that one sees in legacy businesses also holds true in the world of disruption. Low penetration levels in most market segments have opened the opportunity for entrepreneurs to launch new products and brands, in online, offline and omni-channel modes. India today has 100 unicorns[6], and added 3 a month in 2021[7]. A report by Praxis Global Alliance(2021) is optimistic that India currently has 190 “Soonicorns” which are likely to graduate to Unicorn status by 2025. Fintech happens to be the largest generator of unicorns, followed by retail, online classifieds and travel, education and food, content and gaming. The time taken to reach unicorn-status has shrunk from an average of 7.4 years in 2010 to 2.4 years now, and based on the current trend lines, one can expect 250 unicorns by 2030. My prediction: powered by the domestic consumption boom, the most sought after jobs in 2030 will not be Unilever or Goldman Sachs, which have traditionally ruled Day 1 in top-tier campus recruitments, but in yet to be born, bootstrapped, adrenaline-driven, Unicorn-aspirant startups.

In the consumer sphere, two contra-trends are simultaneously true. New, but traditionally-driven consumer brands continue to create extraordinary wealth. Just look at Vini Cosmetics which makes the Fogg brand of deodorant. Or Pulse in the candy business, started by a true-blooded traditional paan masala company. Or Biba in women’s apparel, Fab India in handwoven garments and home furnishings, Forest Essentials in Ayurveda based skin care, MDH in spices, Veeba in sauces. The list is endless. At the same time, in category after category, digitally native brands are making their mark. Boat’s headphones are a rage with the 20-something crowd. Mama Earth’s skincare products have caught the imagination of young women. Licious found a white space in the meat industry and is attempting to create a direct-to-consumer brand in an otherwise disorganised sector. Country Delight, with its deep supply chains, is disrupting the dairy industry. Pharmeasy, a company we are shareholders in, has built India’s largest online pharmacy, became a Unicorn last year, and is planning an IPO pegged at a $5-6 billion valuation.

India’s disposable income led consumer boom is going to have profound changes in the financial markets as well. Currently as on 30th Sep 2021, the top seven sectors constituting the Nifty 50 stock market index are financial services (37.23% weightage), information technology (17.41%), oil and gas (12.30%), consumer goods (11.11%), automobile (4.71%), pharma (3.39%), and construction (2.69%)[8]. By 2030, there will be large changes in this composition as the Indian economy evolves. Financial services and oil and gas will reduce their weightage, and consumer goods will clearly gain. A few months ago, Tata Consumer Products replaced Gas Authority of India Limited in the index. And there’s talk that retailer DMart and consumer internet behemoth InfoEdge will soon be included in the index as well. Such changes will affect how India’s savings are eventually invested, creating a positive feedback loop. In more ways than one, this will be the decade of the Indian consumer!

Offsetting the secular trend of disproportionate increase in disposable income driving consumption-led-growth, there are several challenges that we cannot wish away as a society. We cannot expect government leaders to solve them in the course of the next decade, though we can expect they can be moderated to some degree.

India’s growth will be distorted by the differentials in economic activity in the West and the South as compared to the North and the East.

India’s growth will be distorted by the differentials in economic activity in the West and the South as compared to the North and the East. Already, on average, India’s southern and western states have been growing materially faster than their northern and eastern peers. By 2019, the three richest states in India on an absolute GDP basis were Maharashtra, Tamil Nadu and Gujarat. Then came Uttar Pradesh. When one considers that Uttar Pradesh’s population is 3x that of Gujarat and its economy is similar in size to Gujarat, the story becomes shocking[9]. Per capita income of Gujarat, on the basis of Net State Domestic Product is 3x more than that of UP. Here are some more counter-intuitive statistics: Goa, India’s richest state on a per capita basis is more than 10x richer than Bihar, India’s poorest. Punjab, long considered India’s rich state, currently has a smaller GDP than the split-up states of Andhra Pradesh and Telangana individually; even on a per capita basis, it ranks much below Telangana and is neck-to-neck with Andhra Pradesh. Indeed, the future comes slowly, and then suddenly.

This would have at least three implications: Given the vastly different levels of prosperity, it would be difficult to get India’s 4817 legislators – the total number of members of parliament and of the various legislative assemblies – to reach common ground on the way forward for India. Moreover, if one adds the cultural and language differences between the rich and the poor states, the electorate would likely turn inward. The prosperous middle class in, say Tamil Nadu, would wonder why their tax monies are being spent to subsidise the inefficiencies of the masses of Uttar Pradesh. The urban crowds of Bangalore or Pune—fearing risks of squalor and crime—may not take too kindly to the rush of poor migrants from Bihar. Such fault lines have been seen in China and Korea, though these countries created high quality jobs in manufacturing, which is less true in India, and given the linguistic differences, managing these will be a fine art at all levels of the administration.

In the run up to 2030, India’s leaders will have to address the skewed nature of India’s development and will have to counter two fundamental questions, both of which have no correct answer.

India has lifted 271 million people out of poverty in the last decade (between 2006 and 2016)[10], as per the United Nations Development Programme’s 2019 Multidimensional Poverty Index. This number is sometimes contested because of inaccuracies and lags in Indian economic data. Nonetheless, India’s extraordinary feat in tackling poverty hides many inconsistencies, as has been pointed out by Nobel laureate Amartya Sen and economist Jean Dreze in their earlier book “An Uncertain Glory”. Gender, caste and geographical disparities haunt India’s poor. Like elsewhere in the world, rising inequality is an issue in India. India’s Gini Coefficient – a standard measure of income inequality – is already worrying, especially given our stage of development. However, this picture of inequality is very different from western experience in the past decade, where standards of living for large sections of society have declined as compared to that of their parents. In India and in most developing countries, absolute gains have been across the board, even though uneven.

In the run up to 2030, India’s leaders will have to address the skewed nature of India’s development and will have to counter two fundamental questions, both of which have no correct answer. One is philosophical. The contradiction between liberty and equality – highlighted in Will Durant’s remarkable book “The Lessons of History” – will need to be addressed. The other is political. In a famous interaction between former Prime Minister Manmohan Singh and an un-named Chinese minister on the Chinese reform programme, when asked whether it would lead to greater inequality in China, the Chinese minister replied “We would certainly hope so.” Ideologically, I consider myself the right fringe of the left-movement, and would suggest that each one of us, not just political leaders or policy wonks, take a hard, holistic and pragmatic look at this question. 2030 is waiting for our answer.

My generation has been fortunate that we started our work life in the aftermath of the 1991 reforms. India’s growth rate quickly got reset to an upward trajectory. As India shed its socialist leanings and internalised the dynamism of free markets, the very definition of the ideological centre in the left-right economic dialogues moved decidedly towards the right. This trajectory has continued under governments of all hues and has been accelerated in the recent policy announcements. Indeed, the debates from thirty years ago seem archaic.

As India shed its socialist leanings and internalised the dynamism of free markets, the very definition of the ideological centre in the left-right economic dialogues moved decidedly towards the right.

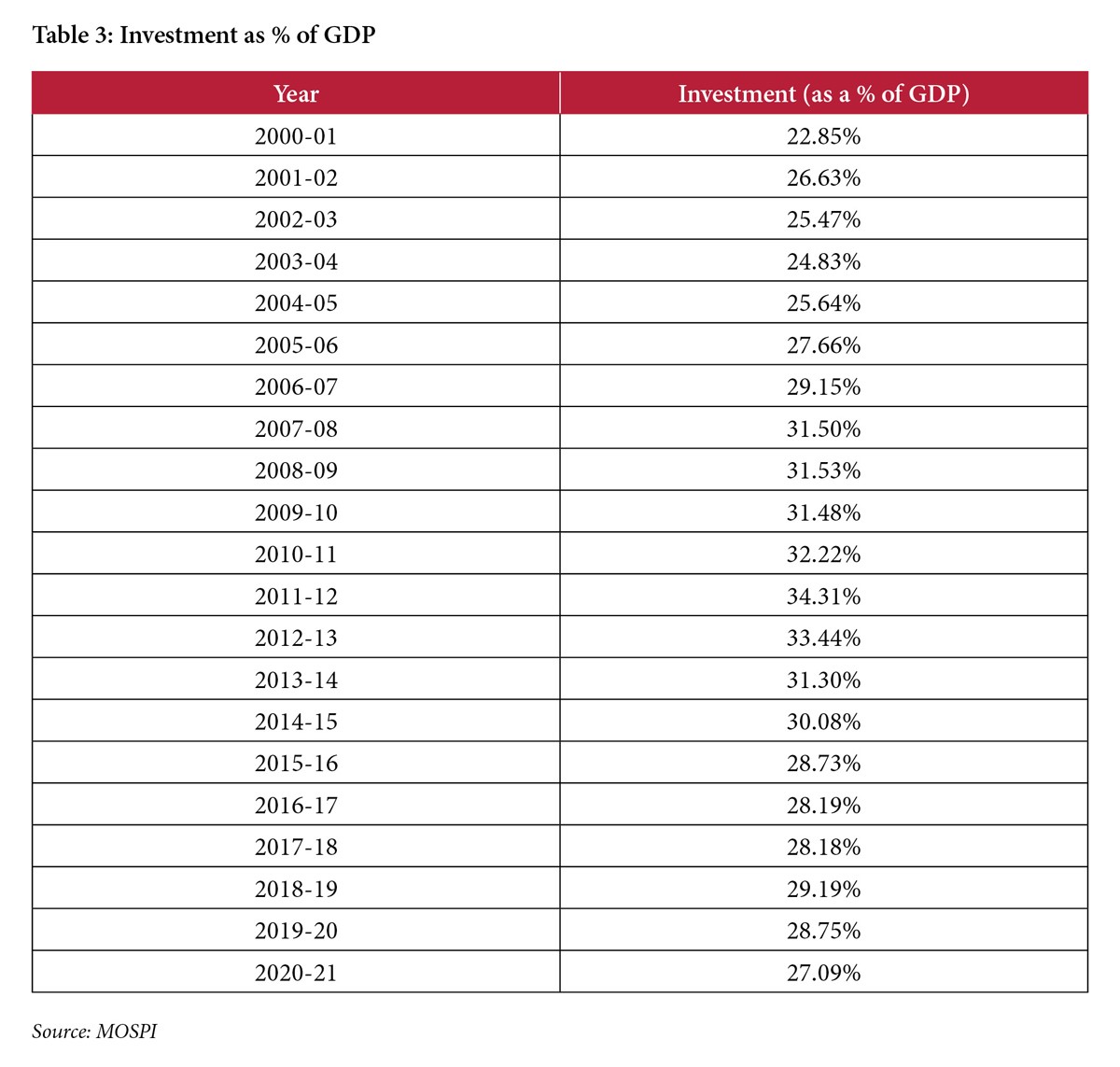

As businessmen, we need to benchmark what our economic expectations are. First, we need to anchor it to the reality of the country. Economic theory tells us that growth is investment rate divided by incremental capital output ratio. Both are sticky numbers. India’s investment rate for long stretches has hovered around 30%[11]. The investment rate is strongly correlated to India’s savings rate, which in turn is partly cultural and partly determined by the dependency ratio. Because of our high dependency ratio, our savings rate in the 1960s was almost half of what it is currently. As our savings rate doubled, so did our growth. India’s incremental capital output ratio is about 4 and is inching upwards. Therefore, India’s fighting weight in terms of economic growth is in the range of 7-7.5% and this is what it should strive for.

Second, we have to think probabilistically. We have to imagine scenarios and work with possibilities rather than a deterministic path. India’s growth will fluctuate around this number, and we should not get ecstatic if it goes to 9% briefly or collapses to 4.5% periodically. Both have happened and have invited extreme views. As India’s investment rate has circumstantially fluctuated, we have seen its effect on the GDP figures, most of which is short-lived. To borrow from Rudyard Kipling, we have to learn to meet with Triumph and Disaster, and treat those two impostors just the same!

Third, superficial comparisons with other countries are misleading. For instance, an oft-asked question in business circles is how China managed a spectacular growth rate of 10% for almost two decades. Here’s the answer: In most of that period, China’s savings rate was 45% and its incremental capital output ratio was about 5. The math was simple. Years of sub-par investments fuelled by a debt binge increased the incremental capital output ratio to 7 or more[12]. Growth fell at 6.5%. The magic ended. One should not consider this a failure, but a somewhat natural outcome of the economy maturing.

Fourth, India’s favourable demographic window will create what Charlie Munger calls the “Lollapalooza” effect. Berkshire Hathaway Vice Chairman Charlie Munger coined the term to outline how multiple different tendencies and mental models combine to act in the same direction. Low dependency ratios will fuel a self-reinforcing cycle of savings, investments and growth. A bulge in working age population, which started in 2018 and is expected to last till 2050[13], can help turbocharge growth, as happened with many Asian countries in the late 20th century, which saw near-double digit economic growth for decades. To borrow from astrology, India’s stars are rightly aligned.

If one stays with India’s natural fighting weight in terms of economic growth, in the short to medium term, good governance can change the number by 1%.

Governments matter. In some ways, more than we think. In other ways, less than we think. In the early 1990s, 40.85%[14] of Uttar Pradesh’s population and 22.19% of the combined Andhra Pradesh was below the poverty line. Both were near the bottom of the league tables. Twenty years later in 2011-12, Uttar Pradesh’s poverty rate was 29.43%[15], while Andhra Pradesh had managed to reduce it to 9.20%. Political entrepreneurship clearly works. On the other hand, in the near term global macro and economic cycles matter more than governance. If one stays with India’s natural fighting weight in terms of economic growth, in the short to medium term, good governance can change the number by 1%. Global conditions—trade barriers, commodity prices, interest rates—can change this by a larger factor. In the long term, as macro-forces cancel each other, global macro goes into the background. What’s left is governance. People often tend to misattribute credit and blame. Political and election cycles, the recurring hum of central government or some state government elections, amplify this trend. So, one request, my friends: don’t focus on 2022 or even 2025, but on 2030!

Optimism is warranted. Here’s a surprising fact from the World Bank: Their “Lived Change Index” uses lifetime per capita GDP to track how much economic change a population has experienced[16]. Over the past three decades, China is an outlier, having delivered 31x, with runner up Poland at 9x, and India comes in 6th at 5x, ahead of Singapore, Malaysia and Brazil. India needs to continue to play the long game well.

An ascending India of 2030 will act in a versatile manner, have foresight and will shape the global agenda.

At the same time, speed will be of essence. Consider the following world events: coup in Myanmar, power crisis in Texas, Australia vs Facebook, Bitcoin hit $50,000, China banned BBC, NASA landed on Mars, India sent vaccines to many countries, global drop in Covid cases, first US airstrike under Biden. As data researcher Norbert Elekes pointed out, all of these happened in the single month of February 2021. Given this accelerating pace of world events, an ascending India of 2030 will act in a versatile manner, have foresight and will shape the global agenda.

The adage “The economy is too important to be left to economists” is often attributed to Winston Churchill but here I am referring to the seminal book by Robert Reich, well known UC Berkeley academic and former Labour Secretary in the Clinton Administration. He wrote passionately about the role of government in the era of late stage capitalism that we are in. South Korea’s “Miracle on the Han River”, from the early 1960s to the late 1980s, is considered unprecedented in the history of the world, and was led by its outward looking government. China’s transformation was anchored by Deng Xiaoping’s “To be rich is glorious” moment in the late 1970s. Germany, Mexico, Czech Republic, all had similar political champions.

In India, as political power devolves from the centre to the states, governance will become a deeper determinant of success.

In India, as political power devolves from the centre to the states, governance will become a deeper determinant of success. Whether it is managing the government’s precarious finances or streamlining the maze of direct and indirect taxation, whether it is solving the accumulated problems of bad loans on the books of India’s banks or bringing real long-term interest rates down from the high 5% that has haunted Indian business, whether it is navigating the world of trade agreements or strategising as multinationals ponder over their China+1 plans, whether it is tackling head on India’s poor social indicators or upgrading India’s state capacity, whether it is advancing India’s geopolitical standing or optimising India’s privatisation programme, whether it is tech-sector regulation or accelerating action on India’s legal backlog of 45 million cases[17], whether it is catching up on India’s infrastructure needs or solving India’s agricultural inefficiencies, the winning formula will reside at the intersection of politics and economics. Economics will provide the logic, politics will provide the leeway.

India’s demographics is both a boon and a bane. India’s window of opportunity is perhaps the next decade and a half.

India’s demographics is both a boon and a bane. India’s window of opportunity is perhaps the next decade and a half. The over-65 population is projected to overtake the under-five group between 2025 and 2030. “India Ageing Report 2017” by the United Nations Population Fund says the share of population over the age of 60 would increase from 8% in 2015 to 19% in 2050. All this will reverse the trend of declining dependency ratios, hurt the savings-investment-growth dynamic, and moderate India’s economic growth rates. I read a tweet recently, which reflected the sentiments of Middle America: “The lifestyle you ordered is out of stock,” This would likely play out in India as well. With the build up of aspirations on one side and the weight of demographic reversals on the other side, tensions will surely mount.

Political leaders will have to lead with a singular focus and follow Jim Collins’ management advice regarding leadership in a world of complexity and uncertainty: “Instead of being oppressed by the “Tyranny of the Or”, highly visionary companies liberate themselves with the “Genius of the And”— the ability to embrace both extremes of a number of dimensions at the same time.” For Vision 2030 and beyond, boxes are out, fluidity is in.

Policy adventurism has long tails. For instance, recent news reports[18], though contested[19], show how government finances have been hurt by the oil bonds of the 2005-10 period, which were issued by the government to oil marketing companies to compensate for under-recoveries resulting from rise in crude prices which they were not allowed to pass on to consumers and industry. These, estimated between $10 to $18 billion, is now coming due, starting from late 2021 through to 2026. Such exercises of creative management of the Union Budget have added up to make government finances precarious and are effectively making taxpayers today pay for subsidies handed out to consumers more than a decade ago. In most such cases, politics wins, economics loses. Hard headed economics needs to be brought centre-stage.

In the near term, while the seductive appeal of nationalism, populism and protectionism will prevail, ultimately the pendulum will swing towards global integration, and our own historical experience of being an autarky will probably make us a champion of free markets and globalisation as this decade comes to an end.

Political polarisation would also likely have economic solutions. In a very timely essay in The American Purpose, Steven Feldstein (2021), a Fellow at the Carnegie Endowment, spoke about the risks of technologically driven echo chambers and safe havens: “There is a risk that democracies will fracture even further, into “splinternets,” unable to coordinate norms and standards.” Such risks are even more stark in India because of its multidimensional diversity. A singular focus on tangible prosperity can channelise the narrative. In the near term, while the seductive appeal of nationalism, populism and protectionism will prevail, ultimately the pendulum will swing towards global integration, and our own historical experience of being an autarky will probably make us a champion of free markets and globalisation as this decade comes to an end. And importantly, India has been conditioned to look West. Much of the action now is in the East and as India cracks the East Asian trade networks, the rewards are likely to be disproportionate.

As the world moves from bilateralism to multilateralism, alignments will be more issue based and tactical, giving Middle Powers like India new abilities to shape the world.

The Lowy Asia Power Index (2020) ranks countries based on eight criteria: economic capability, military capability, resilience, future resources, economic relationships, defence networks, diplomatic relations and cultural influence. Directly or indirectly, all of these factors are a confluence of political and economic forces. In the 2020 survey, India ranked 4th, after the United States, China and Japan. By 2030, India could easily come 3rd, if not 2nd. Geopolitically, India will have an opening: As the world moves from bilateralism to multilateralism, alignments will be more issue based and tactical, giving Middle Powers like India new abilities to shape the world. However, capitalising on it, will require an integrated worldview, the core of which will be India’s economic strength, aided and abetted by political craftsmanship, the deep roots of the Indian diaspora, and India’s near-natural status to be a counterweight to China.

The shortest poem in the world – Me, We – was recited by heavyweight boxing champ Muhammad Ali at the Harvard Commencement in 1975. It signified the paradox of self-confidence and deference to the community. The decade leading to 2030 will need Indian leaders to recite such poetry.

The economic prize of 2030 may not seem that attractive at first glance. According to the World Economic League Tables (2021), India’s GDP in 2030 will be $6.2 trillion, translating to $4185 on a per capita basis. However, on a PPP basis, this would be at least 3x more, comparable to Indonesia, South Africa or Peru today. As a society we should endeavour to beat this base case. Getting there will require Cathedral Thinking.

Cathedral Thinking refers to long-term, visionary work that could take generations to complete. Much like building a massive cathedral, those who lay the first stones won’t be there to savour the finished product. Yet each worker is driven to make a meaningful contribution to something that will be enjoyed by future generations, who they’ll never meet. That is the long-range vision leaders need if India has to reach its true potential.

For those who think that a nation’s economic fate is determined by geography or culture, Daron Acemoglu and Jim Robinson (2012) have bad news. In their remarkable book, “Why Nations Fail”, they go through two thousand years of political and economic history, and conclude that it’s man-made institutions, not resources or endowments or the contingencies of history, that are the prime determinants of whether a country is rich or poor. India’s institutions need to be reset for the new era of global competition.

India of 2030 will look very different from an institutional setting and that will perhaps be the core driver of all the surface changes that we will encounter.

A few things stand out. India’s institutions are typically forced to cater to a range of conflicting demands. Regulators often play catch up with market realities. Many government policies have a crisis as a frame of reference. And lastly, in India’s defining moments, individual heroism trumps institutional initiatives. India of 2030 will look very different from an institutional setting and that will perhaps be the core driver of all the surface changes that we will encounter.

Success – amongst people, businesses, countries – is not a result of more good luck, less bad luck, bigger spikes of luck, or better timing of luck. Instead, they make more of their luck than others. The current decade is a time to maximise our return on luck!

256 Network & Praxis Global Alliance. (2021). Turning Ideas to Gold. Retrieved from url:https://www.praxisga.com/reports-and-publications/financial-investors-group/report-turning-ideas-to-gold

Acemoglu, D. & Robinson, J.A. (2012). Why Nations Fail: The Origins of Power, Prosperity and Poverty. New York: Crown Publishers, Random House.

Collins, J. & Porras, J.I. (1994). Built to Last: Successful Habits of Visionary Companies. United States: Harper Business. ISBN 0-060-56610-8

Dreze, J. & Sen, A. (2013). An Uncertain Glory: India and its Contradictions. New Jersey: Princeton University Press.

Durant, W. & Durant, A. (1968). The Lessons of History. Simon & Schuster.

Feldstein, S. (2021). Can Democracy Survive the “Splinternet?”. American Purpose. Retrieved from url: https://www.americanpurpose.com/articles/can-democracy-survive-the-splinternet/

India Ageing Report (2017). Caring for Our Elders: Early Responses, available at https://india.unfpa.org/sites/default/files/pub-pdf/India%20Ageing%20Report%20-%202017%20%28Final%20Version%29.pdf

Lowy Institute Asia Power Index. (2020). Lowy Institute. Retrieved from: https://power.lowyinstitute.org/

Pitch Madison Advertising Report 2019. Retrieved from url: https://www.exchange4media.com/PMAR19-Final.pdf

Press Trust of India. (September 2, 2021). ‘India added three ‘unicorns’ per month in 2021: Hurun report’. Business Standard.

Reliance Industries Limited Integrated Annual Report 2019-2020. https://www.ril.com/getattachment/299caec5-2e8a-43b7-8f70-d633a150d07e/AnnualReport_2019-20.aspx

Reserve Bank of India Bulletin. August 2021. Volume LXXV Number 8. Retrieved from url: https://rbidocs.rbi.org.in/rdocs/Bulletin/PDFs/0BULLETINAUG2021767F2556D32A4061B0AC0EE3C54C1208.PDF

Telecom Regulatory Authority of India. (2020). The Indian Telecom Services Performance Indicators, July-September 2020. New Delhi. Retrieved from url: https://www.trai.gov.in/sites/default/files/QPIR_21012021_0.pdf

United Nations Development Programme. (2019). The 2019 Global Multidimensional Poverty Index (MPI). United Nations Development Programme and Oxford Poverty and Human Development Initiative. Retrieved from url: http://hdr.undp.org/en/2019-MPI

United Nations Population Fund 2017. ‘Caring for Our Elders: Early Responses’ – India Ageing Report – 2017. New Delhi, India: UNFPA. Retrieved from url: https://india.unfpa.org/sites/default/files/pub-pdf/India%20Ageing%20Report%20-%202017%20%28Final%20Version%29.pdf

Virmani, A., 2004. India’s economic growth: From socialist rate of growth to Bharatiya rate of growth, (No. 122). ICRIER Working Paper.

WORLD ECONOMIC LEAGUE TABLE (2021). Available at https://cebr.com/wp-content/uploads/2020/12/WELT-2021-final-23.12.pdf

Zac Dycthwald. (2021). China’s New Innovation Advantage. Harvard Business Review. Retrieved from url: https://hbr.org/2021/05/chinas-new-innovation-advantage

FOOTNOTES

[1] See https://www.financialexpress.com/archive/redefining-the-hindu-rate-of-growth/104268/

[2] https://www.thehindubusinessline.com/economy/at-92-salary-growth-in-india-is-highest-in-asia/article30462524.ece

[3] See data from Insurance Regulatory and Development Authority of India

[4] See Pitch Madison Advertising Report 2019 available here https://www.exchange4media.com/PMAR19-Final.pdf

[5] Reliance Industries Limited Annual Report 2019-20, page 4

[6] See 100 Unicorns: India’s changing corporate strategy, India Market Strategy, Credit Suisse, March 10, 2021. Quoted in RBI Bulletin, August 2021.

[7] https://www.business-standard.com/article/companies/india-added-three-unicorns-per-month-in-2021-hurun-report-121090200848_1.html

[8] https://www1.nseindia.com/content/indices/ind_nifty50.pdf

[9] Handbook of Statistics on Indian States, RBI

[10] https://gdc.unicef.org/resource/report-india-lifted-271-million-people-out-poverty-decade

[11] India’s investment rate as a percentage of GDP has fluctuated between 20% and 35%. With increase in NPAs this has been pulled down. However, the government has been prompt in taking strong actions by the Asset Quality Review followed by the introduction of Insolvency and Bankruptcy Code. These should bring back the NPAs to reasonable levels and kickstart the credit cycle.

[12] https://www.brookings.edu/blog/future-development/2019/01/22/joyless-growth-in-china-india-and-the-united-states/

[13] https://ourworldindata.org/grapher/age-dependency-ratio-projected-to-2100

[14] https://www.rbi.org.in/scripts/PublicationsView.aspx?id=18810

[15] https://www.rbi.org.in/scripts/PublicationsView.aspx?id=18810

[16] https://hbr.org/2021/05/chinas-new-innovation-advantage

[17] https://www.news18.com/news/explainers/explained-cji-ramana-says-4-5-crore-cases-pending-heres-what-has-been-fuelling-backlog-3977411.html

[18] https://indianexpress.com/article/explained/the-oil-bonds-upa-launched-why-how-much-and-what-nda-argues-7458773/

[19] https://scroll.in/article/894559/fact-check-have-upa-era-oil-bonds-prevented-modi-government-from-reducing-oil-prices

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.