Non-fuel Mineral Auctions: How Fair is the Game, and For Whom?

Reading Time: 14 minutesDOWNLOADS

Abstract

The Mines and Minerals (Development and Regulation) Act, 1957 was amended in 2015 and introduced as an auctions system to address three major concerns—transparency, fairness, and objectivity—raised by the Supreme Court regarding the mineral asset allocation process. Four changes became evident following the Act coming into force, and these have impacted competitive efficiency in the mining sector. (1) Of 114 non-fuel mineral auctions held so far, many received excessively high bids (particularly for iron-ore mines); bids higher than even the estimated value of reserves. (2) Mining company profiles changed from merchant miners (selling minerals on the market), to captive miners (owning downstream plants that consume the minerals). This could lead to less-than-efficient usage of the minerals acquired through auctions, with induced general equilibrium externalities. (3) High auction bids, combined with high royalty rates and some other statutory payments, have not encouraged new mining activity in any significant way. Short-term financial gains for State governments, and possible long-term revenue losses and strangulation of new investments, may result. (4) Many auctioned blocks are of previously operational mines (brownfield mines), where the leases had lapsed as of March 2020 as per conditions laid down in the amended Act. This paper also touches upon the subsequent amendment to the Act in 2021, and concludes with suggestions for rationalising the auctions mechanism to ensure competitive efficiency in the mining sector.

The Mines and Minerals (Development and Regulation) Amendment Act, 2015, (henceforth MMDR Act, 2015) ended the first-come, first-serve system of mining allocations and has brought in an auctions regime. This was intended to bring in ‘greater transparency’ and ‘[remove] discretion’ (Ministry of Mines, Government of India, 2019) in the allotment of natural resources. The Government of India noted that State governments would receive an ‘increased share [of revenues] from the mining sector’ with the new system (ibid.).

The analysis in this paper provides an overview of bids made in the auctions of iron ore, limestone, iron ore & manganese, bauxite, manganese, graphite, gold, chromite, copper, and diamond, with a focus on iron ore and limestone.

According to the Ministry of Mines, 114 non-fuel mines have been successfully auctioned to date. Technically qualified bidders (i.e., companies fulfilling certain criteria) participated in an ascending forward online electronic auction and bid on the percentage of the value of minerals which would be despatched over the lifespan of the mining operation.[1] There are two stages in the auction process, where the highest bid in the first stage is taken as the floor price of the second stage. The ascending forward system allows bidders to outbid others in each stage. The respective State government then granted each auction’s highest bidder a mining lease or a composite license (i.e., a prospecting license-cum-mining lease), subject to their having satisfied various conditions.

The analysis in this paper provides an overview of bids made in the auctions of iron ore, limestone, iron ore & manganese, bauxite, manganese, graphite, gold, chromite, copper, and diamond, with a focus on iron ore and limestone.

Of the 114 auctions held so far, detailed information on the first 97 auctions (held up to March 2020) is available on Transparency, Auction Monitoring and Resource Augmentation (TAMRA),[2] the auction monitoring website of the Ministry of Mines’.[3] Details on the remaining 17 auctions have not yet been made available.[4] Since detailed information is only available for 97 auctions, some of the figures and tables in this paper consider only this data.

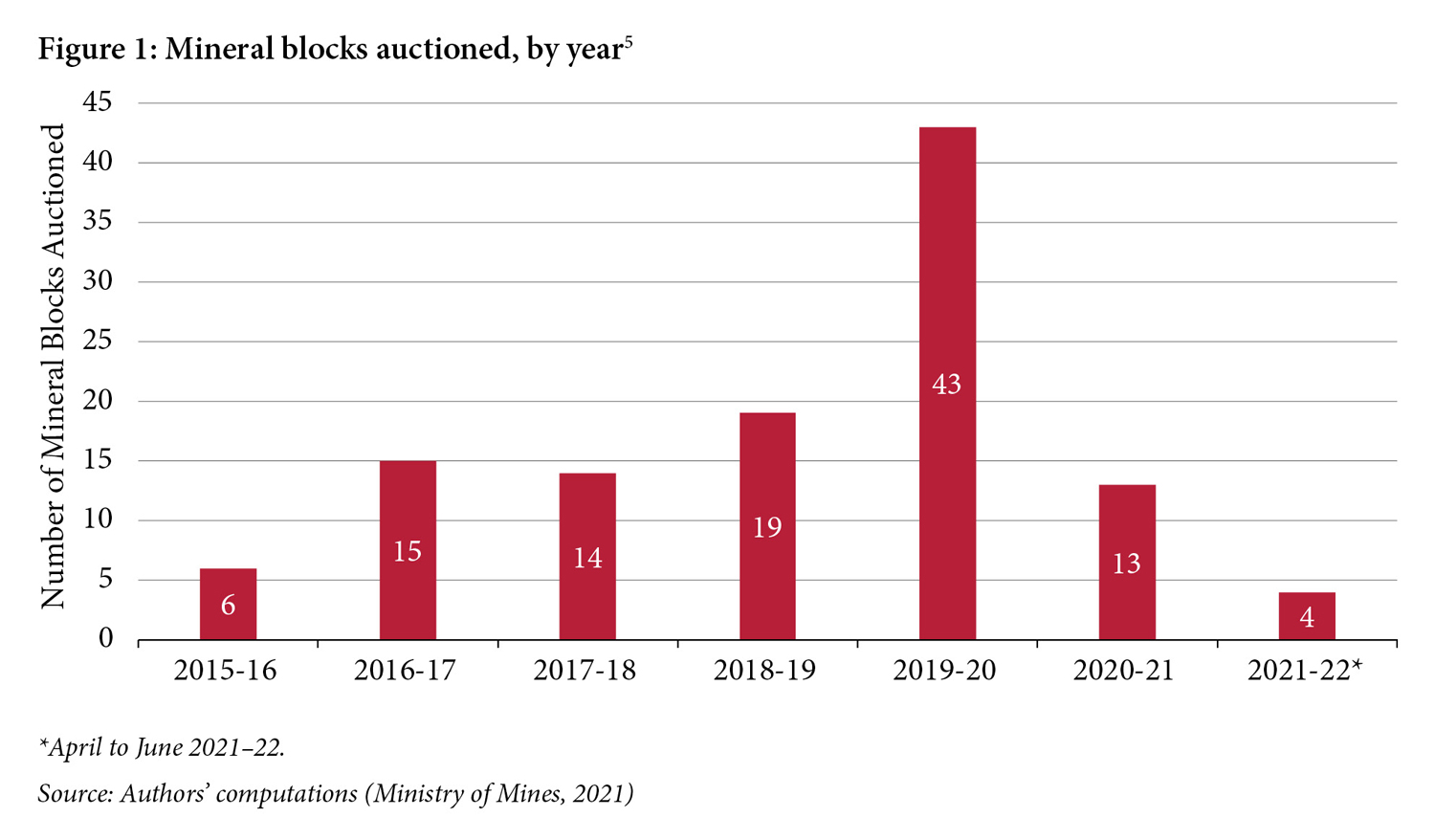

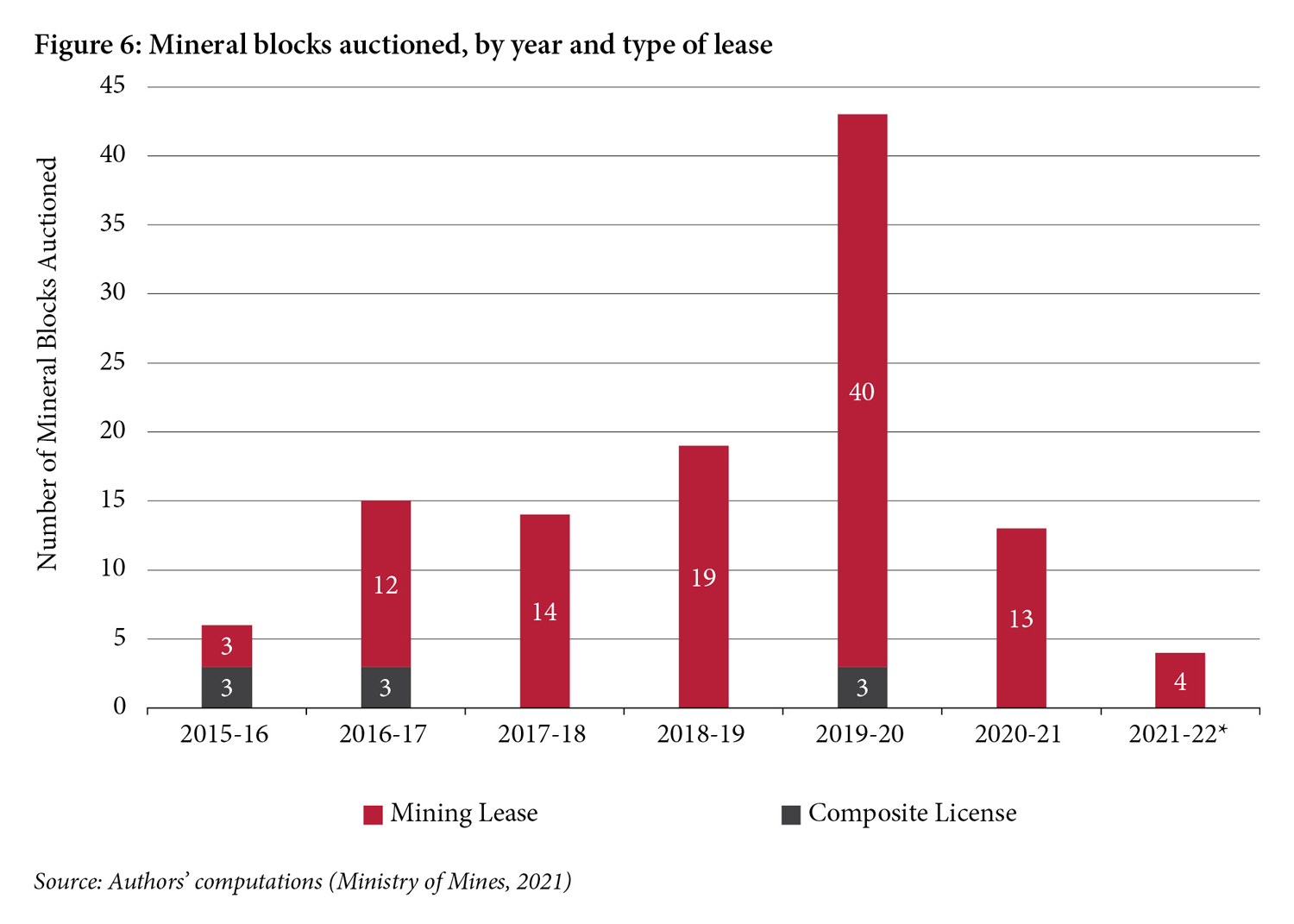

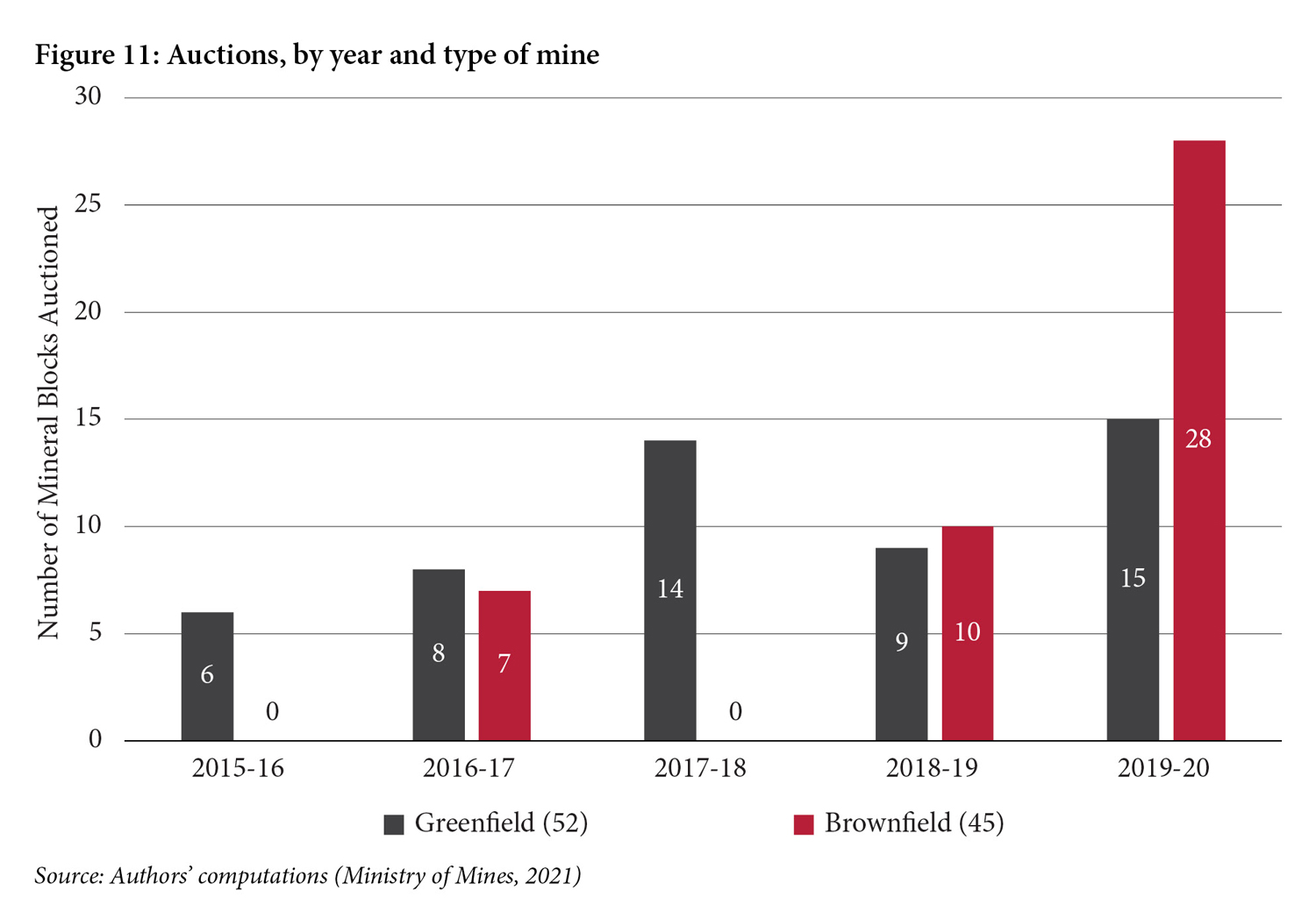

Figure 1 shows the number of auctions each year following the amendment of the Act in 2015. The first year saw just six auctions but this number more than doubled over the next two years, to 15 and 14 respectively. The years 2018–19 and 2019–20 saw a surge in auctions (mainly of brownfield mines, i.e., already mined blocks, unlike ‘greenfield’ mines that have never been mined). This surge was triggered by a provision in the amended Act, which stated that leases of certain merchant mines would lapse on March 31, 2020 for specific reasons as mentioned in MMDR Act, 2015.

Meanwhile, in an attempt to ensure mineral security and continuation of mining, the government has passed the Mines and Minerals (Development and Regulation) Amendment Act, 2021 [MMDR Act, 2021], which allows for valid clearances to be passed on to the new leaseholder to ensure ‘continuity in mining operations even with change of lessee’ and to ‘avoid repetitive and redundant process of obtaining clearances’ for the same mine.

The amendments in MMDR 2021 have also resolved various pending cases under Sections 10A(2)(b) and 10A(2)(c)—to do with the rights of those who were granted leases before the MMDR Act, 2015—by stating that a ‘large number of mineral blocks’ would be put up for auction.

Figures 1 and 2 show the increasing number of auctions in 2018–19 and 2019–20, with 43 taking place in 2019–20; more than a third of all auctions since the start of the regime.

Of the 43 mines auctioned in 2019–20, 17 were iron-ore mines, and six were iron ore and manganese mines. With many iron-ore mines closing and the mining leases of several non-captive mines coming to an end in March 2020, there have been speculations that India might become a net importer of iron ore again. This had last happened in 2015 (Dry Cargo International, 2019). However, speedy auctions of mines will help increase the indigenous mining of iron ore rather than relying on imports.

Speedy auctions of mines will help increase the indigenous mining of iron ore rather than relying on imports.

The year 2020–21 saw the fewest auctions (barring the first year, 2015-16), which may be in part due to the Covid-19 pandemic. There have already been four auctions in the ongoing financial year 2021–22, with many more blocks expected to be auctioned. (HT Correspondent, 2021).

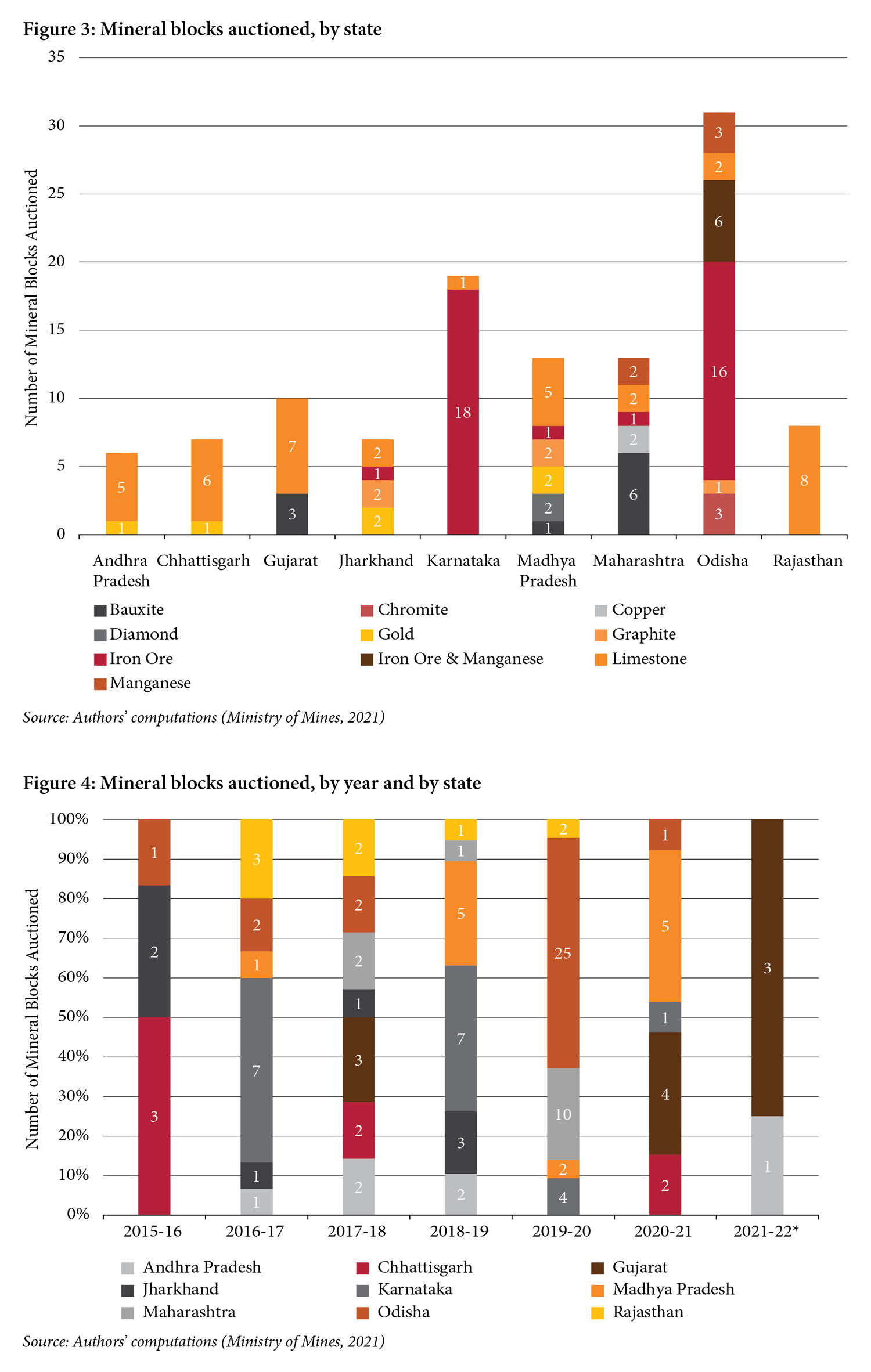

A total of 19 auctions have been held in Karnataka, 18 of which were previously operational iron-ore mines. Odisha saw a surge in auctions in 2019–20, with 25 blocks auctioned, of the total 31 in the state. The remaining seven states had fewer than 15 auctions each, primarily for limestone blocks (Figures 3 and 4).

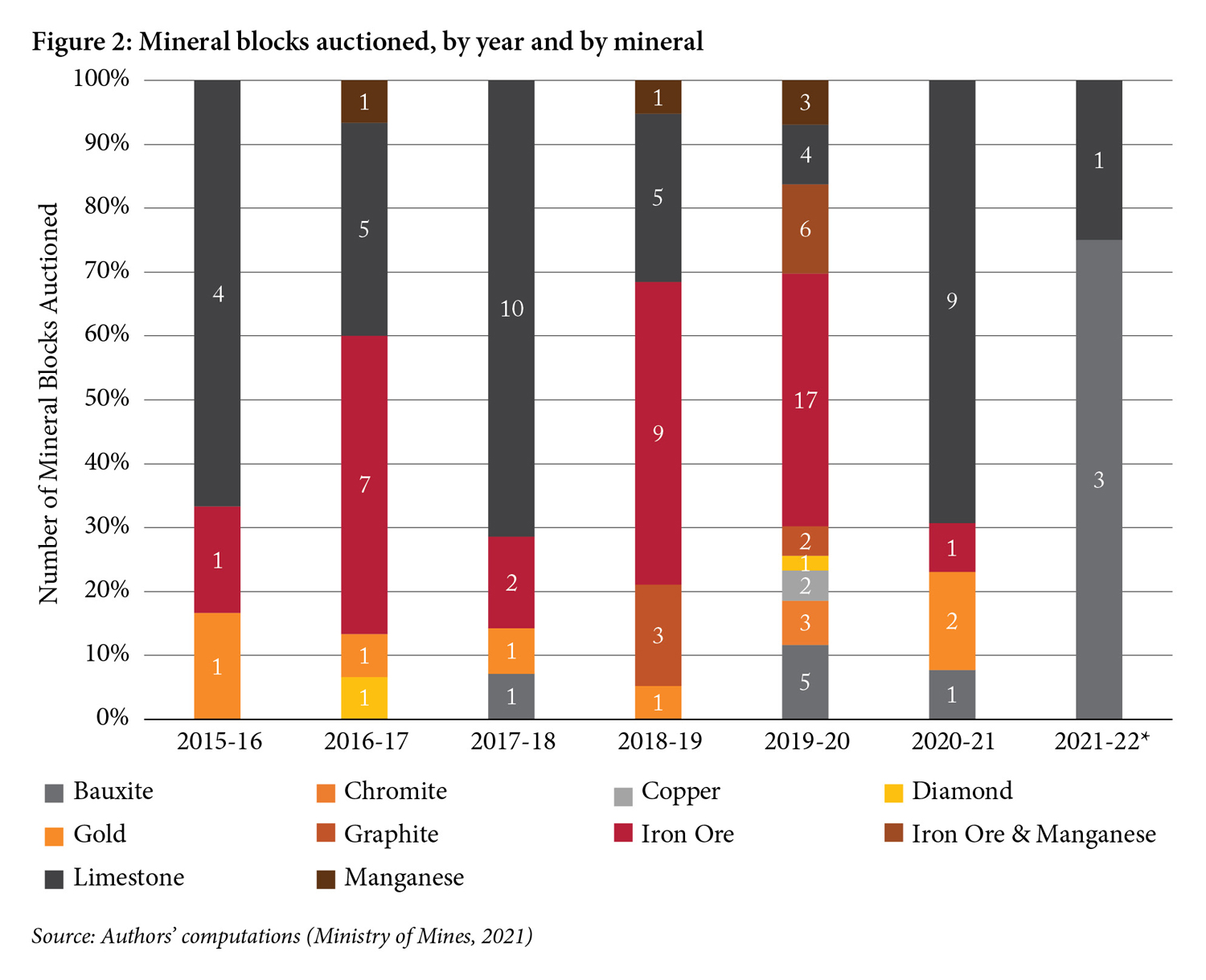

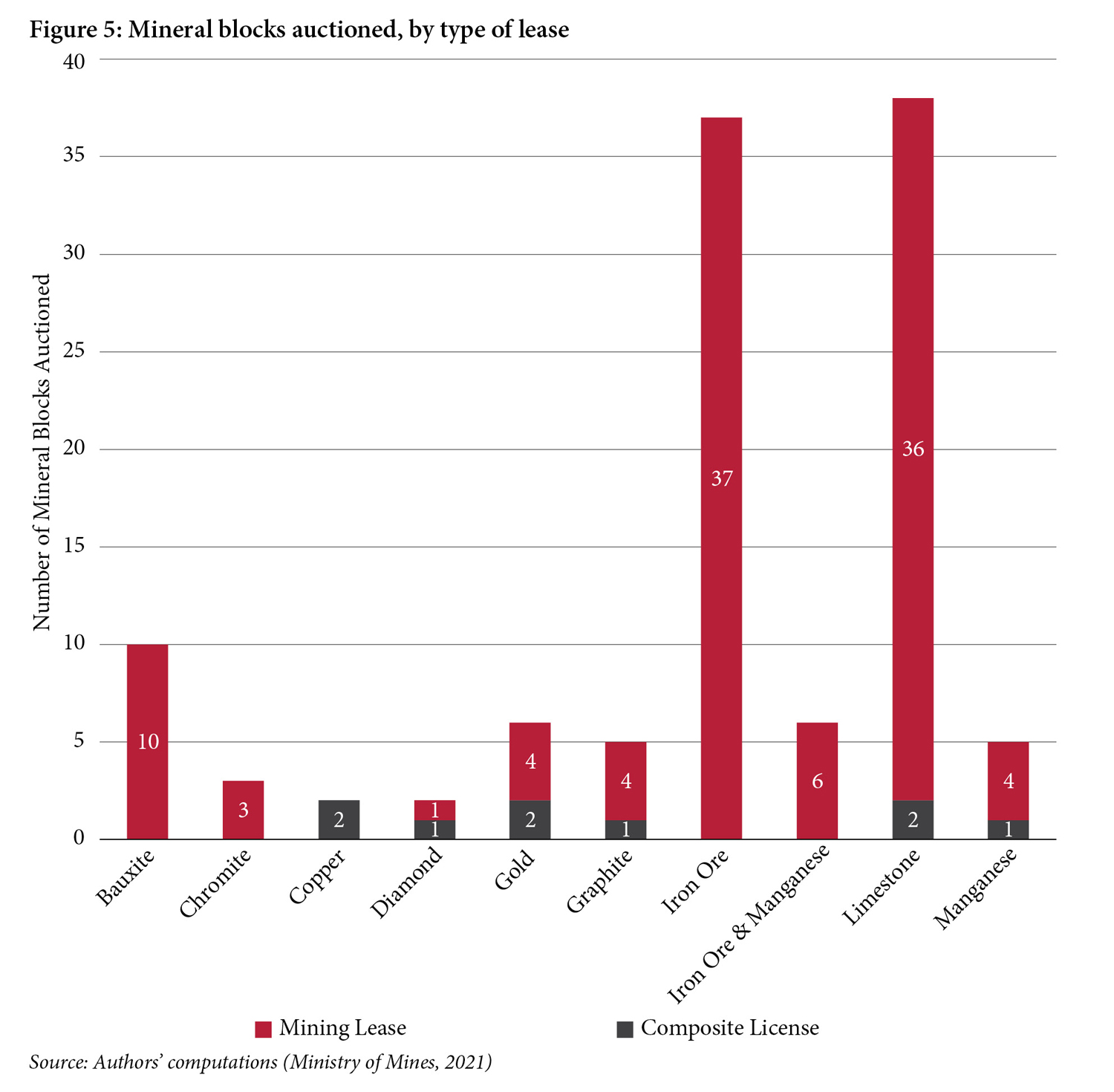

The majority of blocks auctioned were iron ore (and some iron ore and manganese) and limestone blocks, which in total make up 81 of the 114 total auctions (Figure 5). In comparison, there were far fewer auctions of blocks with deep-seated minerals.

There are two types of leases that may be auctioned under MMDR Act, 2015: mining leases (MLs) and composite licenses (CLs) (prospecting license-cum-mining lease). The Minerals (Evidence of Mineral Contents) Rules, 2015 Section 7 provides details on the exploration requirements to determine whether a CL or ML would be granted for a particular mineral area.

Holders of CLs are given the right to undertake prospecting operations, followed by mining. These licenses are granted in areas with limited exploration and weaker evidence to show mineral content (MMDR Act, 2015, Section 11).

The majority of auctions were for MLs (Figures 5 and 6), given that many blocks were previously operational mines (and hence there was sufficient evidence for mineral content). As a result, 105 MLs were granted (in comparison to just nine CLs—one each for diamond, graphite, and manganese; two each for gold, copper and limestone). Composite licenses are generally granted for non-bulk commodities, such as diamonds and graphite, where more exploration is needed before mining operations can commence. More must be done to incentivise the exploration and mining of these non-bulk commodities.

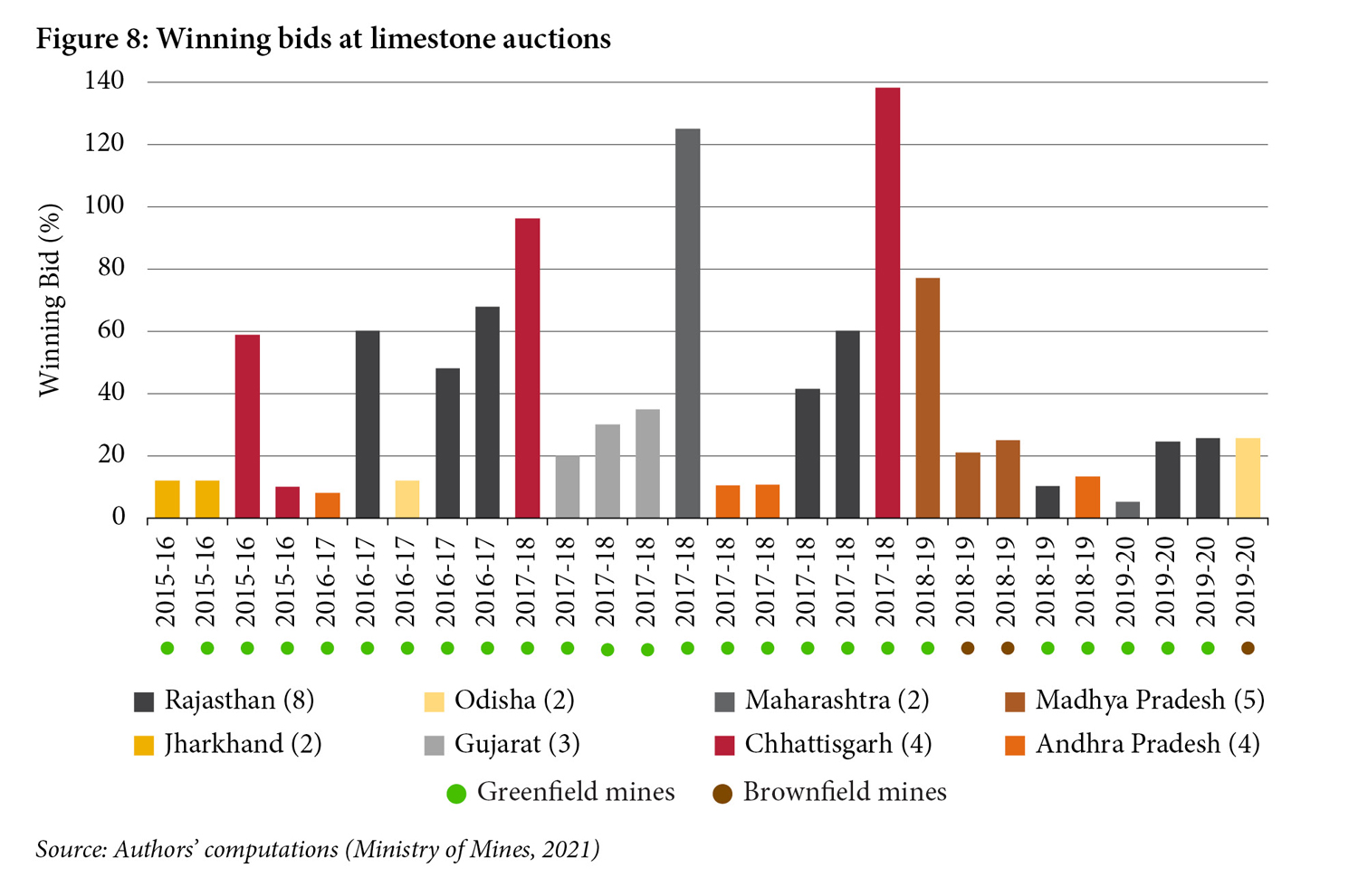

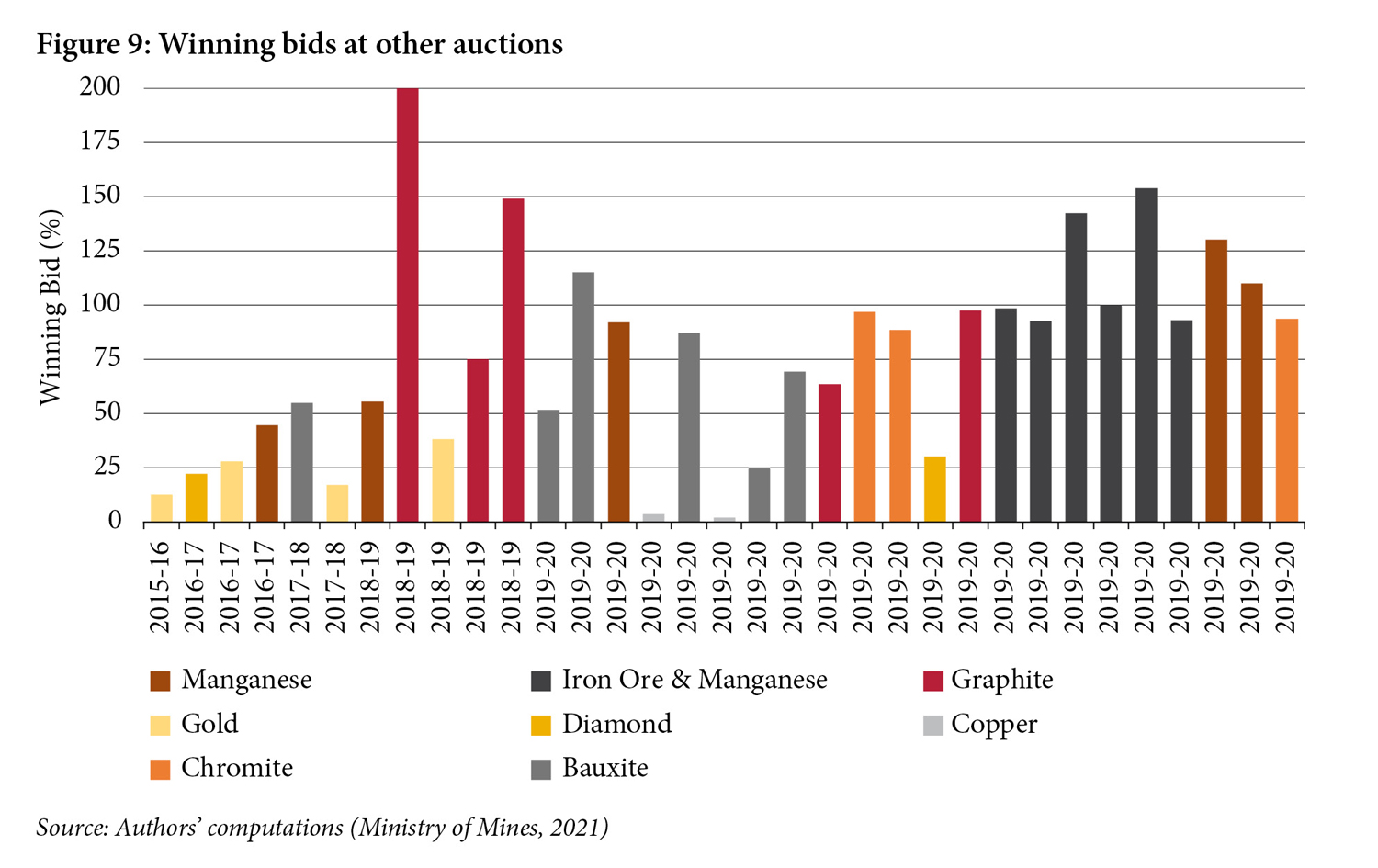

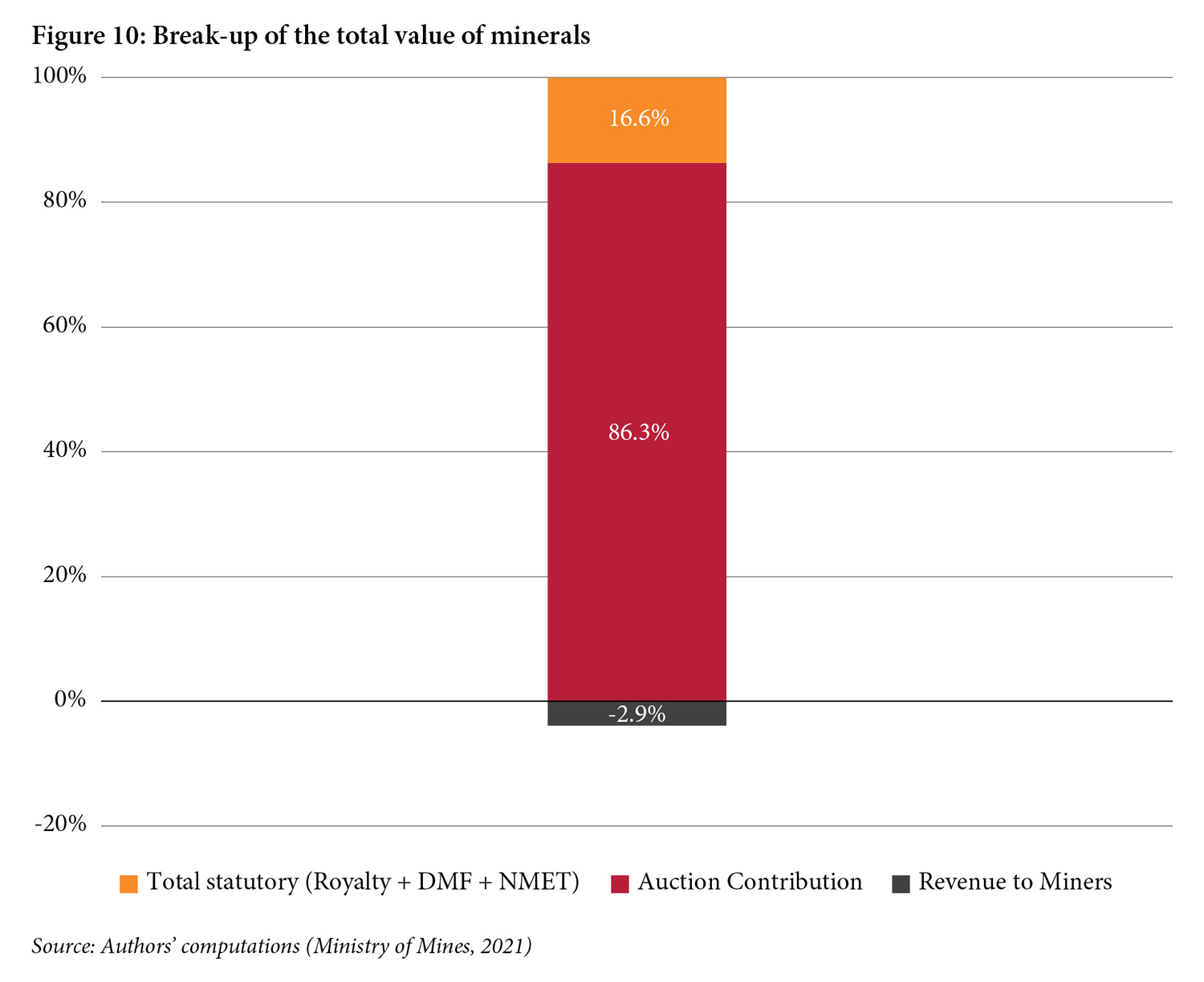

Figures 7 to 9 show the winning bids for iron ore, limestone, and other blocks. As detailed information has not yet been made available, these figures show only the 97 auctions until March 2020. Some of these auctions were won with bids exceeding 100 percent, where mining companies agreed to pay the government more than the value of the minerals despatched, on top of statutory payments and other taxes. Statutory payments consist of royalties, District Mineral Foundation (DMF) contributions (10 percent of royalties for leases granted in or after 2015, and 30 percent of royalties for older leases), and National Mineral Exploration Trust (NMET) contributions (2 percent of royalties).

The winning bidder must pay the State government the bid percentage of the value of the minerals mined each month.[6], [7] The value of the minerals is computed using the Average Sale Price (ASP),[8] which is published by the Indian Bureau of Mines for each mineral by state and mineral grade, considering the mineral sales done by non-captive miners. These computations are done ex-post.

Computation of auction payment:

Monthly auction payment

= quantity of mineral despatched

× Average Sale Price of mineral (by state and grade)

× percentage quoted in auctions

Captive miners may sustain such a business model by absorbing losses from mining activities in their downstream businesses. In contrast, merchant miners will have to find ways to remain competitive. High bids in auctions result in inefficiencies in the economy. Captive miners may choose to only mine as per their requirements which might distort open market prices to their competitive advantage. Additionally, high bidders, hit by the ‘winners’ curse’, may not even start mining operations. Further, mining companies may attempt to cut corners in environmental protection or community welfare, given the high premiums they have committed to the government in auctions.

High bids in auctions result in inefficiencies in the economy. Captive miners may choose to only mine as per their requirements which might distort open market prices to their competitive advantage. Additionally, high bidders, hit by the ‘winners’ curse’, may not even start mining operations.

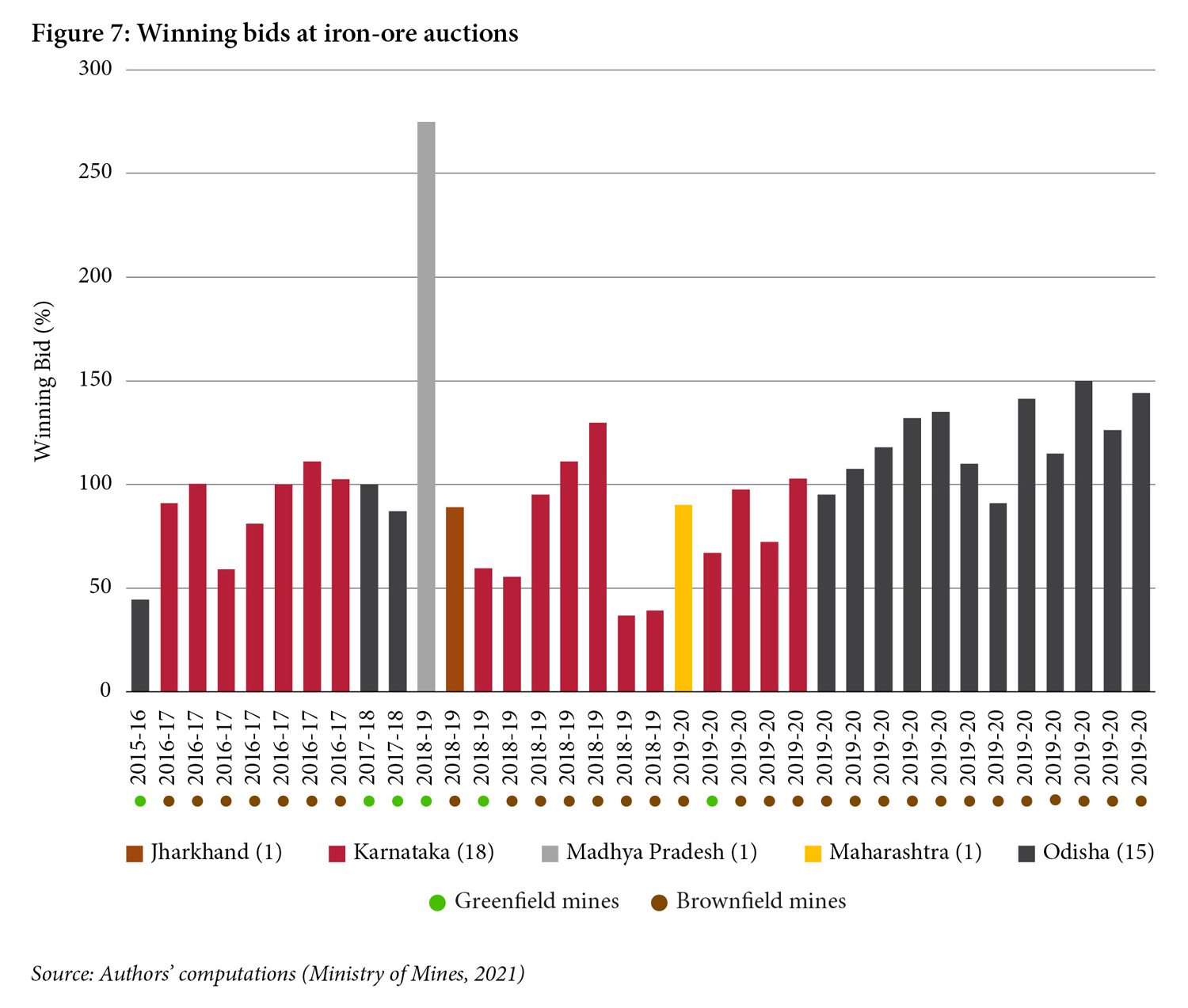

Many iron-ore mines have been auctioned at high premiums. For example, Figure 7 shows the Pratap Pura iron-ore mine in Madhya Pradesh, which was auctioned for 275 percent of the value of minerals in May 2018—the highest bid ever. Of the most recent iron-ore auctions in Odisha, all but two mines had a winning bid of over 100 percent, with the remaining two going for over 90 percent. The bids for the new iron ore and manganese mines were similarly high, with all six receiving winning bids of over 90 percent (Figure 9).

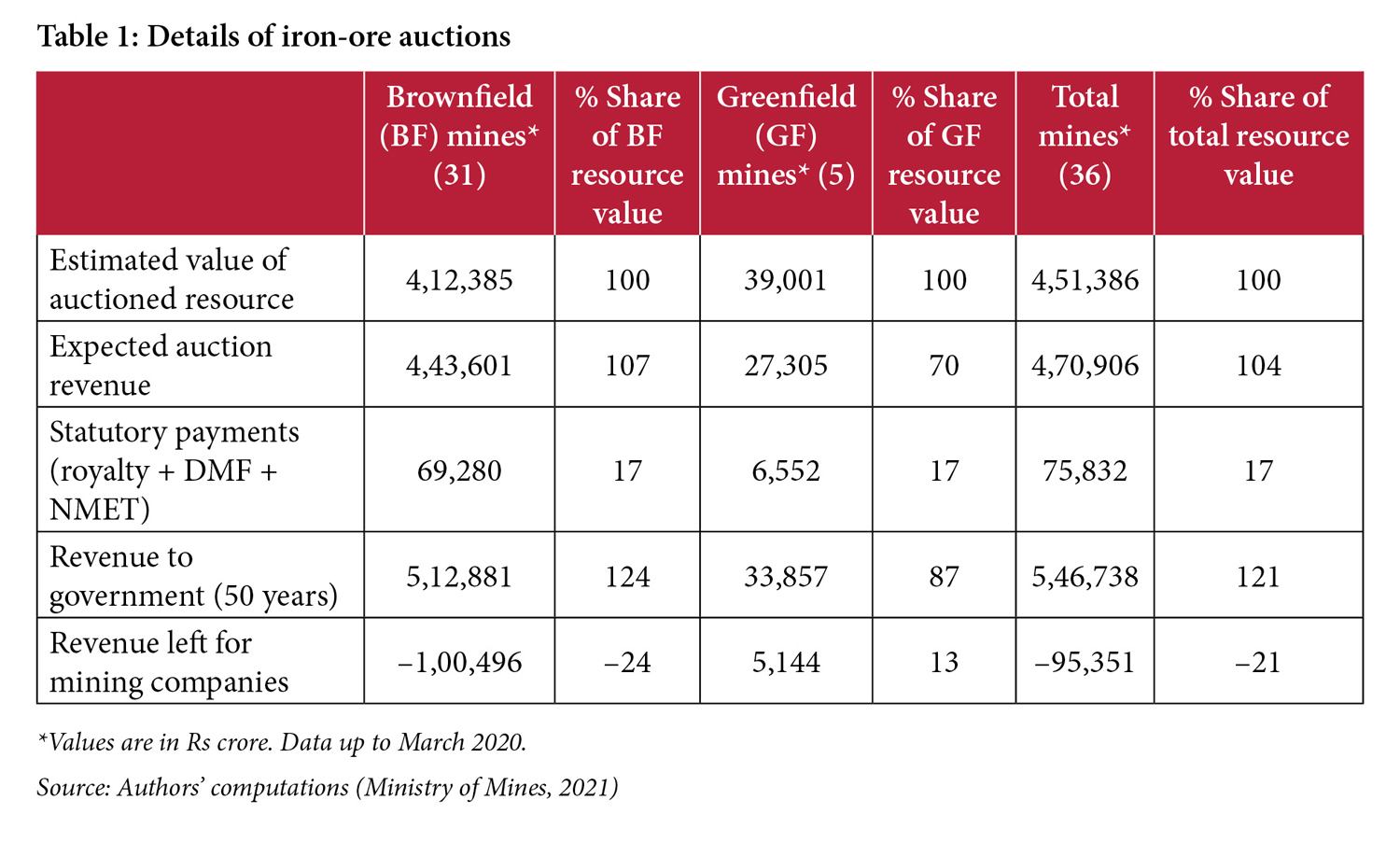

The auctions of iron ore blocks can be split into two components: brownfield mines and greenfield mines. Of the 36 iron ore mines auctioned, 31 were brownfield, and the remaining five were greenfield. While only a few greenfield mines were auctioned, it is notable that the average winning bid for brownfield mines (107 percent) was higher than the average for greenfield mines (70 percent), as is shown in Table 1. Figures 7 and 8 show the mines auctioned (green circles represent greenfield mines and brown circles represent brownfield mines).

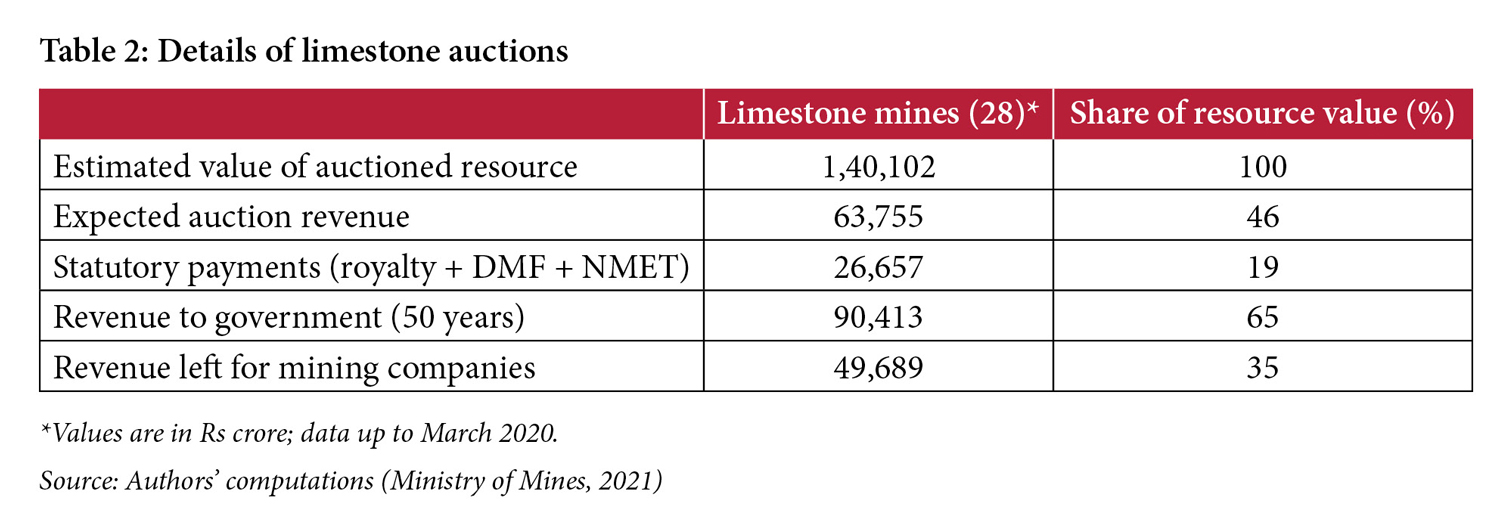

In contrast to the iron ore auctions, Figure 8 shows that greenfield blocks dominated limestone auctions—25 of the 28 mines were greenfield. With these auctions, the average bid for greenfield blocks was 47 percent, higher than the 26 percent average for brownfield blocks. As opposed to iron-ore blocks, the bids for the greenfield limestone mines were higher on average than for brownfield mines, though only a few brownfield mines were auctioned.

Besides iron ore and limestone, six blocks of precious minerals were also auctioned. An interesting case was that of the Bunder diamond mine in Madhya Pradesh. Originally, evidence of the minerals was discovered by the Anglo-Australian mining company Rio Tinto in 2004. However, little progress was made to convert the exploration efforts into a mine, and in 2017, Rio Tinto announced that it would be ‘gifting’ the project back to the Government of Madhya Pradesh (Rio Tinto, 2017). The mine was then auctioned in 2019, and Essel Mining won the ML with a bid of 30.05 percent. Besides iron ore and limestone, peculiarly high bids (ranging from 75 percent to 200.05 percent) were received for the six graphite mines.

The auctions show that winning bids have been excessively high, leaving very little for the companies.

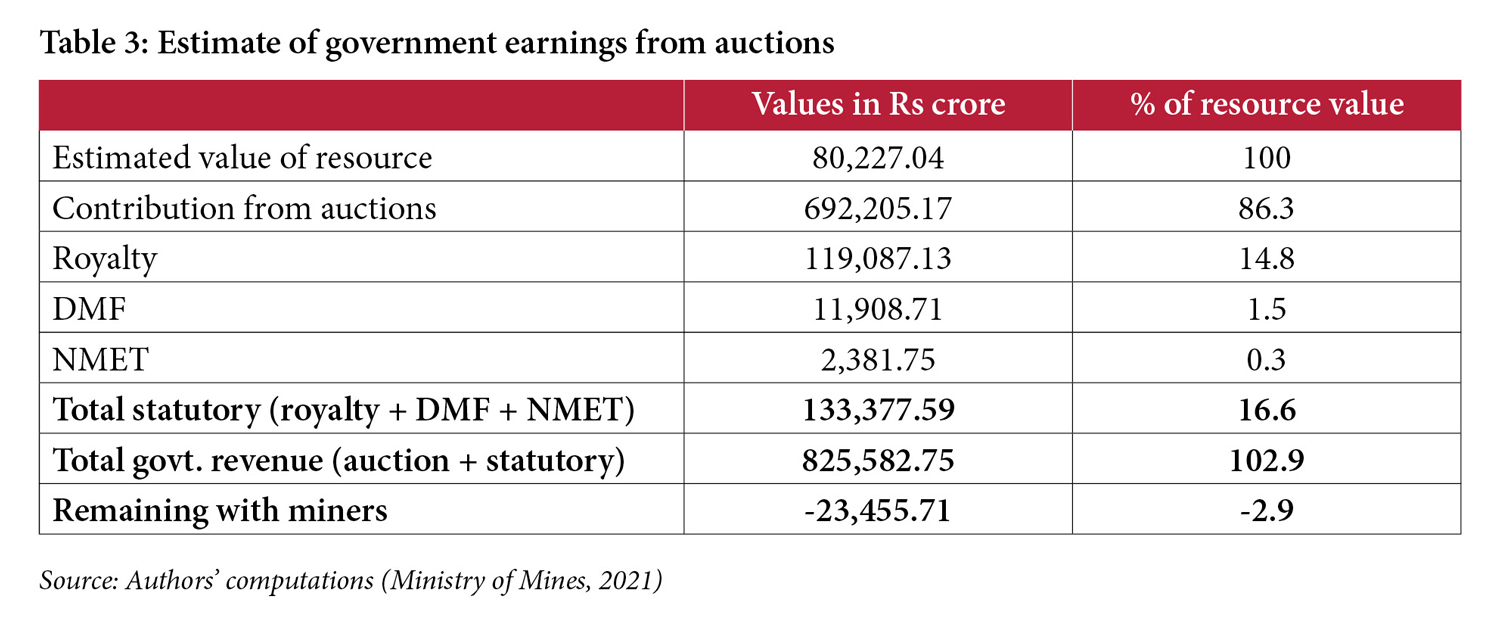

Using the results of the auctions and exploration data on the estimated quantity of mineral resources, the Ministry of Mines makes some implicit assumptions to calculate how much State governments can expect to earn over the lifetime of the mines. The auctions show that winning bids have been excessively high, leaving very little for the companies. Tables 1 and 2 show estimated earnings from iron ore and limestone auctions respectively, while Table 3 reflects the overall earnings of State governments from all auctioned mines. The assumptions made in computing this estimate apply to all tables:

- The estimate of the quantity and grade of resources in a mineral block is not the final quantity that can or will be mined.

- The ministry uses the average sale price (ASP) of the mineral (by state, and by grade) to determine the value of the minerals.

- This ASP will fluctuate over the lifetime of the mine and will likely not reflect the average value used when the ministry made its estimates.

- Of the 97 blocks auctioned, nine were for CLs. However, there is no guarantee that the prospecting efforts shall lead to a viable mining operation, and this will result in lower-than-expected government revenues.

For the 97 mines auctioned, the miners will, on average, pay the respective State governments 102.9 percent of the value of minerals. This is primarily due to the large winning bids for the 42 auctions of iron-ore and iron-ore and manganese blocks. These bids consistently exceeded 50 percent and in 22 auctions exceeded 100 percent.

Over and above the payment of operational expenses, auction commitments, and statutory payments, miners also need to pay corporate taxes, forest and wildlife protection payments, and stamp duties. All these costs may make the business model unsustainable, leading to dampened production, corners being cut (e.g., health and safety, environment, and community welfare) or a forfeit of the lease.

Many of the auctions were of brownfield merchant mines where the leases had lapsed in March 2020 (Figure 11). Section 8A of the MMDR Act, 2015 states that non-fuel mining leases would be valid for 50 years. Additionally, the leases of older merchant mines in operation for longer than this period would be allowed to continue mining operations till March 31, 2020, while the leases of similar captive mines would be extended till March 31, 2030.

A total of 334 mines were impacted by this section of the act in total, of which 48 were working mines, primarily producing iron ore which accounted for 25–35 percent of the country’s total output (Patel, 2019).

Given India’s untapped geological potential and the imminent demand for critical minerals for green technology manufacturing, there is an urgent need to enable the exploration and auctioning of greenfield deep-seated mineral assets and ensure their early operations.

Of the 97 auctions until March 2020, 45 were of brownfield blocks, i.e., mines previously in operation. There were 52 auctions of greenfield mines, including those with deep-seated minerals such as copper, diamond, gold, and graphite. However, according to the Federation of Indian Mineral Industries (FIMI), no greenfield mining project has come into operation from the auction process (Iyengar, 2021).

The Central government has attempted to facilitate a seamless transition between the leaseholders through an amendment of the MMDR (this was done with the Mineral Laws (Amendment) Act, 2020, which amended provisions of both MMDR, and the Coal Mines Act), such that the new miner would be able to start operations without acquiring new environmental clearances for two years.

Given India’s untapped geological potential and the imminent demand for critical minerals for green technology manufacturing, there is an urgent need to enable the exploration and auctioning of greenfield deep-seated mineral assets and ensure their early operations.

The Mines and Minerals (Development and Regulation) Act, 1957, was amended in March 2021 through the MMDR Amendment Act, 2021 (March 28). Several changes were made to improve mining and create a level playing field between captive and merchant miners. With this amendment, captive miners may now sell up to 50 percent of the minerals produced after meeting the requirement of their end-use plants and upon payment of additional amounts, compared to 25 percent before. This should help reduce the wastage of minerals and increase their supply in the open market.

Public-sector mining companies are also being brought to the same playing field as private-sector miners. While public-sector companies may be allocated mining lands without going through the auction process, they will be required to make additional payments to make up for the auction payments the state exchequer would have otherwise received if allocated to private-sector companies.

More changes have been made to the clearance transfer system, with auctioned brownfield mines carrying any existing and valid clearances to the new successful bidder. The aim is to ‘avoid the repetitive and redundant process of obtaining clearances again for the same mine’.[9]

Issues relating to the pending cases under Sections 10A(2)(b) and (c) have also been cleared, and many mineral blocks are set to be auctioned. The government has decided to reimburse the expenses incurred by the mining companies, through funds from the NMET. The Non-Exclusive Reconnaissance Permit (NERP) has been done away with; there had been no takers since its introduction in 2015.

The auction system needs a thorough review. Mentioned below are a few observations in this regard.

- The promised high returns are the potential financial reward for the states, if the winning miners can overcome the ‘winner’s curse’ paradigm (Vijay Kumar & Sinha, 2020), and accomplish scheduled tasks. However, even if the miners succeed, the idiosyncratic promised over-payment acts as a tax on merchant miners and the economy.

- The cost overspend would have to be recovered from downstream operations of these miners, creating inefficiencies of resource allocation in mining and downstream activities. In a general equilibrium framework, the economy shall have to bear the cost of a less than efficient allocation of productive resources.

- As per discussions with senior officers of various mining companies and government officials, the reasons for overbidding may be many:

- Most relate to the security of procuring raw materials. The cost of minerals may only be a small proportion of operations cost for downstream plants, but guaranteeing mineral supply would be important to the producers.

- Additionally, some mining companies might have bid high in the hope of favourable policy-changes in the future.

- The aftermath of the auctions appears to be unfavourable with regard to boosting mining production in India:

- Some auctioned leases were surrendered, even before mining operations could begin.

- Some others, who started production, failed to meet their agreed-upon production outputs per their Mine Development and Product Plans (MDPA).

- This will adversely impact the government’s estimates of earnings, and the availability of mineral resources for further processing.

- Furthermore, in the context of the Covid-19 pandemic—while global iron-ore prices are rising due to increasing demand from a recovering China (Mining.com, 2021)—iron-ore production in India has been doubly hampered: first by the pandemic, and secondly by the delay in continuing, or starting, operations of mines successfully auctioned over a year ago.

- It is unlikely that the auction mechanism will be reverted to the first-come, first-serve system used in India earlier, which is still used in other mineral-rich countries. However, it may be worth considering a policy that differentiates the allocation mechanism between bulk and deep-seated minerals. It is not feasible to estimate the quantities of deep-seated minerals in the same vein as bulk minerals, without exploration using ore-specific geological expertise. This is evident from the fact that there have been very few auctions of these minerals and from the limited number of deep-seated mineral discoveries in India.

- Moreover, many of these minerals are critical for manufacturing clean energy technologies, electronics, and national security applications. Therefore, the process of allocation of mineral rights must be sensitive to incentivising exploration—including the right to mine, which is prevalent in many other mining jurisdictions.

- Some thought may be given to honing the existing auctions system to achieve a more efficient mineral allocation regime:

- This includes placing multiple mineral blocks on auction under a pre-announced auctions calendar.

- It may also help to change the auctions from a two-stage to a single-stage system.

- Additionally, the ascending forward bidding process may be changed to a single sealed bid.

These changes would help reduce the scarcity mindset, as miners will know when more mineral blocks will be up for auction, and, therefore, it would not encourage competitive overbidding.

- Finally, there must be a relook at the two mineral taxation systems currently in place—royalties and auctions—as past baggage is being carried forward in a new regime. Paul Milgrom and Robert Wilson, both of Stanford University, won the Nobel Prize in 2020 for their pioneering theoretical work on how auctions work, and for their insights on how to innovate auction formats for selling goods and services that are not amenable to efficient sale in a traditional manner (The Nobel Prize, 2020). It would be worthwhile to imbibe learnings from their work to further improve the auctions system in India.

Dry Cargo International. (2019, December 2). India May Become Net Importer of Iron Ore Again from Next Year. https://www.drycargomag.com/india-may-become-net-importer-of-iron-ore-again-from-next-year

HT Correspondent. (2021, June 5). Chhattisgarh govt to auction 16 iron ore, limestone mines in next 2-3 months. Hindustan Times. https://www.hindustantimes.com/cities/others/chhattisgarh-govt-to-auction-16-iron-ore-limestone-mines-in-next-2-3-months-101622870964819.html

Iyengar, S. P. (2021, January 18). FIMI debunks mine auction process; blames it for raw material shortage. The Hindu BusinessLine. https://www.thehindubusinessline.com/news/fimi-debunks-mine-auction-process-blames-it-for-raw-material-shortage/article33599524.ece

Mining.com. (2021, April 6). Iron ore price back above $170 as China steel hits record. https://www.mining.com/iron-ore-price-above-170-on-robust-chinese-demand/

Ministry of Mines website, https://mines.gov.in/, accessed June 2021

Ministry of Mines, Government of India. (2019). National Mineral Policy 2019.

https://www.mines.ap.gov.in/miningportal/Downloads/NewDocs/National%20Mineral%20Policy.pdf

Patel, K. (2019, December 31). Mining lease expiry in 2020 throws up risks and opportunities. MoneyControl. https://www.moneycontrol.com/news/opinion/mining-lease-expiry-in-2020-throws-up-risks-and-opportunities-4774851.html

Rio Tinto. (2017, February 7). Rio Tinto gifts Bunder diamond project in India to Government of Madhya Pradesh. https://www.riotinto.com/en/news/releases/Bunder-project-gifted-to-government

Sivamani, G. (2020). An analysis of non-fuel mineral blocks auctions in India. Brookings India [now CSEP]. https://www.brookings.edu/research/an-analysis-of-non-fuel-mineral-blocks-auctions-in-india/

The Nobel Prize. (2020, October 12). The Prize in Economic Sciences 2020 [Press release].

https://www.nobelprize.org/prizes/economic-sciences/2020/press-release/

Vijay Kumar, S., & Sinha, R. (2020). Mineral Auctions in India: Winner’s Curse or Owner’s Pride? The Energy and Resources Institute.

FOOTNOTES

[1] The rules of the auction process are prescribed in the Mineral (Auction) Rules, 2015.

[2] TAMRA, https://tamra.gov.in/mom.php

[3] Data has been taken from the Ministry of Mines website, https://www.mines.gov.in/

[4] These 17 auctions took place from March 2020 onward, with 13 auctions taking place in the financial year 2020–21, and the remaining four auctions taking place from April to June 2021.

[5] Years refer to the financial year, starting April 1 and ending March 31 of the following year.

[6] Mineral (Auction) Rules, 2015, Section 8

[7] Minerals (Other than Atomic and Hydro Carbons Energy Minerals) Concession Rules, 2016, Section 51

[8] Minerals (Other than Atomic and Hydro Carbons Energy Minerals) Concession Rules, 2016, Sections 42-46

[9] The Mines and Minerals (Development and Regulation) Amendment Bill, 2021

Rajesh Chadha

Ganesh Sivamani

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.