MacroInsights: Crowding-Out? Shrinking Savings, High Public Borrowing Impact Interest Rates

Reading Time: 3 minutesMacroInsights, a Centre for Social and Economic Progress (CSEP) series, dissects key economic developments and policy issues of macroeconomic significance. It offers timely, evidence-based analysis to inform public debate and policymaking.

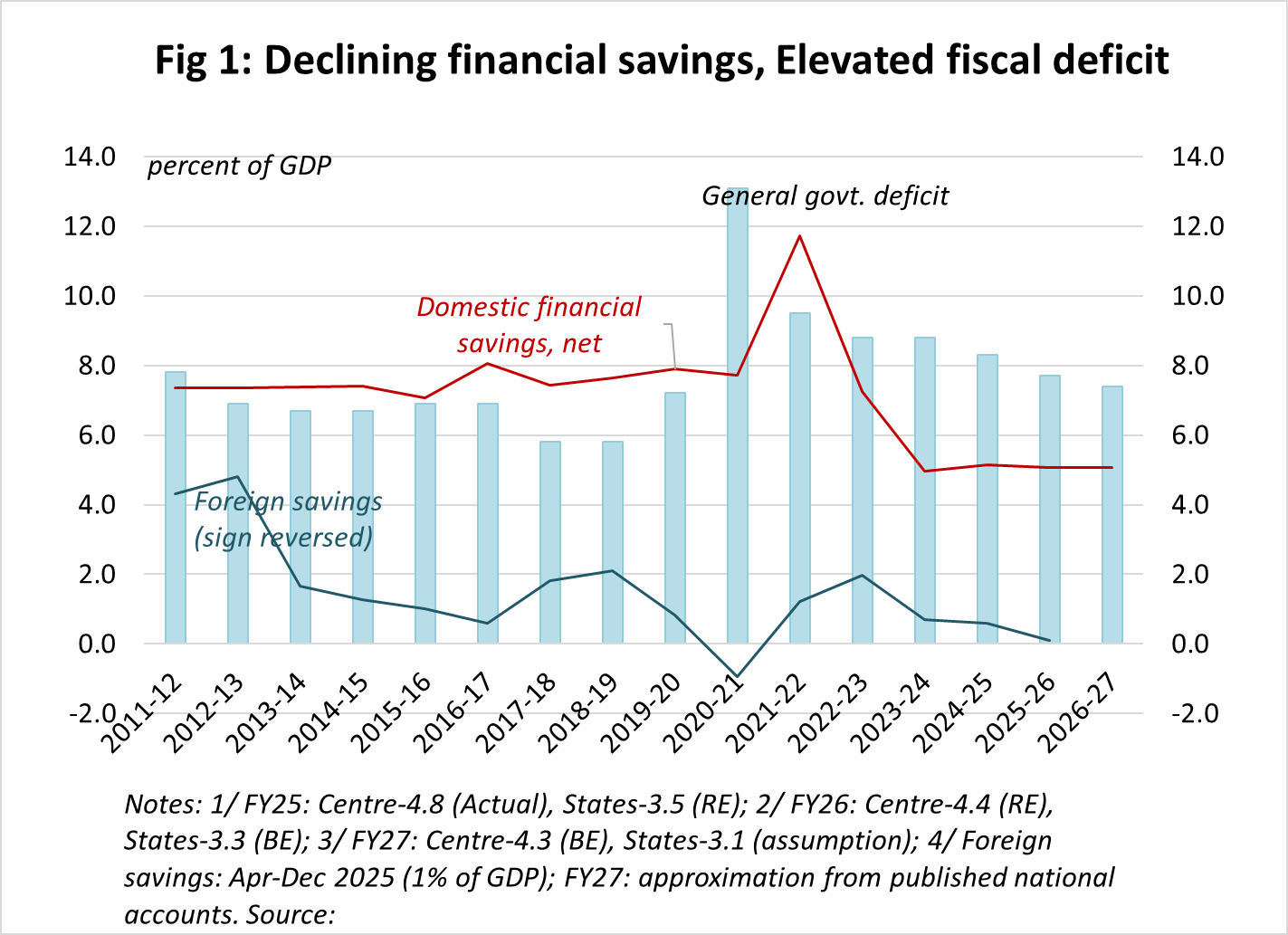

- India’s financial savings have drastically shrunk to 6.5% of GDP in recent years— domestic and external savings averaged 5.4% and 1.1%, respectively, between FY23–FY25 (Chart 1). Financing economic activities—public and private—was not a problem until recently, as private investment demand was muted. This provided considerable space for government borrowings without pressuring real rates (Chart 2). Combined centre–state deficits averaged 8.6% in FY23–FY25.

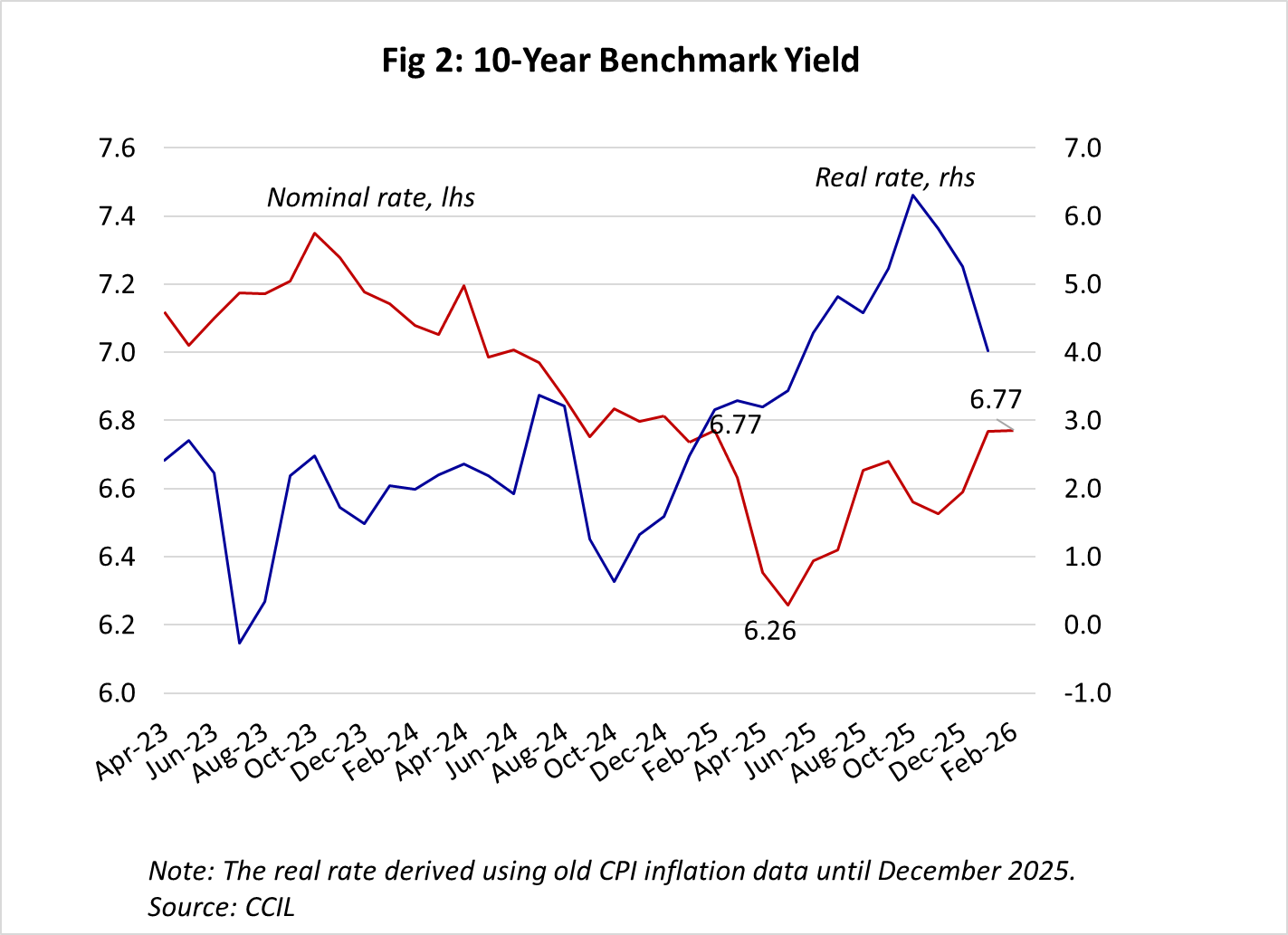

- However, interest rates have been hardening since June 2025, when the 10-year government bond yield reversed direction, defying a 50-bps policy rate cut to steadily climb to 6.77% in February 2026, similar to that a year ago before the start of the monetary easing cycle. State government securities’ yields (10-year) have risen ~80-bps as well, with the average spread over sovereign almost doubling relative to Feb–July 2025.

- The trend is the reverse of the sharp fall in headline CPI inflation since January 2025 (old series) to below 2% lower bound last July, alongside a 125-bps easing by the central bank. The benchmark yield rate should have fallen below 6.0%. In fact, CPI-adjusted real interest rates in FY24–FY25 (Chart 2) were relatively lower!

- The interest rate pressures reflect increased government and private demand for funds.

- Lower tax revenues (raised income tax exemption caps in February 2025 and GST rate reduction in September 2025), larger-than-expected market borrowings by state governments in the second half (FY26), and the FY27 budget in February – Rs 17.2 trillion of market borrowings and slow consolidation – which exceeded market expectations. General government deficit in FY26 is ~7.7 %, and only slightly lower in FY27.

- Post-GST cuts, private credit demand strengthened from ~10–11% in September to 14–15% in the following months through February 2026.

- The question is whether public borrowing is pushing up interest rates. Corporate bond yields (AAA) have risen. Critically, banks’ investment appetite for government bonds has decreased because private credit picked up.

- Financial savings significantly below the general government deficit is an evident constraint. Consider the macroeconomic framework, last assessed by the FRBM Review Committee Report (2017). The then estimated financial saving was 10% of GDP—7.6% domestic and 2.3% external savings. It suggested equal division between the government and the private sector (5.0% each) to avoid potential crowding out. Accordingly, the recommended total fiscal deficit was 5.0% of GDP (2.5% each for the union and state governments).

- However, there is a big question mark now about the sustainable current account deficit—even 1% of GDP or less is proving difficult to finance, given the successive squeezes on the capital/financial account, leading to reserve drawdowns (balance of payments deficit) and unrelenting exchange depreciation pressures.

- The resurfacing of fiscal dominance could possibly force a monetary policy reset by pushing up r*, the real equilibrium interest rate. There would be very few financial resources left for the private sector in the current framework, risking a higher cost of capital (e.g., vis-à-vis China) and a drag upon private investment.

- A pertinent policy question is whether the 16th Finance Commission’s recommendation to target a general government fiscal deficit at 6.5% of GDP by 2030–31 (3.5% and 3.0% for the union and state governments, respectively, after adjusting for special assistance to states for capital investments) is not synchronised with the emerging constraints.

Renu Kohli

Senior Fellow

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.