EV Competitiveness Beyond Incentives

Reading Time: 5 minutes

DOWNLOADS

Executive Summary

This paper examines the reliance of electric vehicles (EVs) on the existing incentives, particularly tax concessions, to become financially attractive in India. In practical terms, the study attempts to understand how long the purchase of EVs in different segments may require preferential tax treatment to remain cost-competitive compared to conventional vehicles. Electric passenger cars and electric two-wheeled vehicles are taken as a case in point.

Higher upfront costs of EVs vis-à-vis internal combustion engine (ICE) variants remain a significant barrier to EV adoption. To bridge this gap with ICE vehicles, governments at the Central and State levels have provided fiscal incentives—primarily purchase subsidies and tax incentives. The latter includes lower tax rates for EV sales under the national Goods and Services Tax (GST) and the State-level Motor Vehicle (MV) tax regimes. Furthermore, a majority of States that are large vehicle sales markets offer MV tax waivers for the purchase of electric passenger cars and electric two-wheeled vehicles.

Together, these national and state tax measures have significantly lowered an EV’s on-road price, narrowing the gap with its ICE counterpart. While purchase subsidies (such as those available under the PM Electric Drive Revolution in Innovative Vehicle Enhancement [PM E-DRIVE] scheme) are time-bound, tax concessions have been more stable and open-ended, forming the backbone of India’s EV affordability strategy. However, the GST rate on conventional vehicles has recently undergone a major change that can potentially alter the relative vehicle cost economics.

Goods and Services Tax Rate Rationalisation and its Impact on Electric Vehicles

Under the GST regime, conventional ICE vehicles were historically taxed at 28% GST + 1% to 22% Compensation Cess. Following GST 2.0 rationalisation (effective from September 22, 2025), the tax structure now features the following:

- An 18% GST on a majority of ICE vehicles;

- Abolition of Compensation Cess;

- Continuation of 5% GST rate for EVs.

Although GST 2.0 maintains the 5% rate on EVs, lowering ICE vehicle taxes from 28% to 18% reduces EVs’ relative price advantage:

- The on-road price gap between EVs and comparable ICE vehicles has widened by ₹1.1 lakh to ₹1.5 lakh for passenger cars.

- Similarly, for two-wheeled vehicles, the price gap has grown by about ₹7,000 post-GST 2.0.

Hence, while EVs retain lower operating costs, their upfront competitiveness has weakened. However, continued dependence on tax incentives may not be fiscally sustainable. Tax revenue constitutes a large share of Centre and State revenue receipts, which determine the government’s ability to deliver vital services to citizens and implement various programmes and schemes. A calibrated tapering down of existing incentives is needed for those who have already played their part in realising the policy objectives—in this case, promoting electric two-wheeled vehicles and electric passenger cars. This could potentially free up much-needed fiscal bandwidth for the government to channel commensurate fiscal support towards decarbonising hard-to-abate transport segments like heavy-duty vehicles, aviation, and shipping.

What Does This Research Address and How?

As EV penetration rises, preferential tax treatment could erode public revenues. Additionally, falling lithium-ion (Li-ion) battery prices are expected to reduce EV production costs further, thus diminishing the possible need for heavy tax support. EV–ICE price parity could be achievable even under the same tax rates in the near future. Therefore, it is important to test the thesis that EVs continue to rely on the existing tax incentives to become cost-competitive vis-à-vis ICE variants.

This study seeks to shed light on how future prices of EVs and the resulting vehicle cost-competitiveness may play out, potentially impacting the dependence of EV uptake on tax incentives in India. The analysis employs a total cost of ownership (TCO) framework and focuses on passenger cars and two-wheeled vehicles. Passenger cars, in turn, have been segmented into private and commercial in consideration of the current vehicle registration norms. The TCO of a vehicle includes its cost of acquisition and operational costs, such as fuel and maintenance costs over its lifetime, which reveals the total cost incurred throughout the vehicle’s lifespan.

Whether there is dependence of EV adoption on a tax incentive is premised on the hypothesis that the EV’s per km TCO does not reach parity with the baseline ICE vehicle within the first five years of vehicle ownership. Baseline ICE vehicle is the one that has the largest share in a particular vehicle segment (i.e., private passenger car, commercial passenger car, or two-wheeled vehicle). If TCO parity is reached by the fifth year of ownership following possible tax hike(s), it is assumed that the EV is no longer dependent on the concerned tax incentive(s). The fifth year of ownership is chosen as the decisive year since vehicle ownership by an original buyer in India averages four to five years, and EV buyers are unlikely to wait longer to realise the cost advantage of EVs over conventional vehicles.

Key Findings of the Study

Based on the EV cost-competitiveness analysis, the research indicates the following scope to rationalise EV tax incentives.

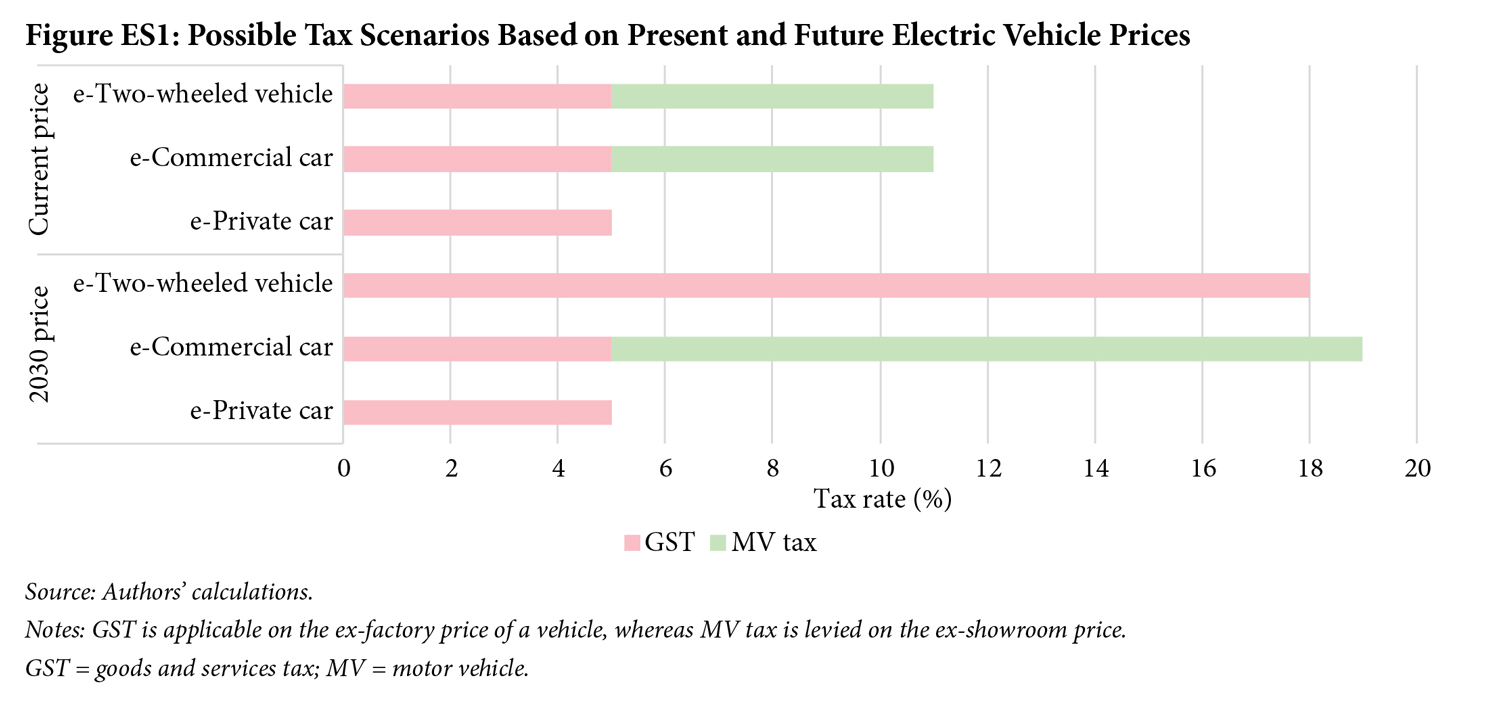

- Privately owned electric passenger cars continue to depend on the existing tax incentives till at least 2030. This includes a preferential GST rate of 5% on EV sales and an exemption on MV tax. Maintaining the status quo is necessary until the costs of electric cars decrease further.

- Our analysis suggests that electric commercial passenger cars are cost-competitive in the current price scenario, even after the removal of the MV tax waiver; however, retaining the 5% GST rate is necessary. States can levy MV tax on this electric car segment up to the rate of 6%. From 2030 onwards, the MV tax rate can be further raised up to 14%, with GST maintained at 5% without compromising the electric commercial car’s cost competitiveness. These tax hikes would enable the States to reduce their tax revenue losses.

- Considering current prices, electric two-wheeled vehicles can remain cost-competitive even when the MV tax is levied up to 6% with the continuance of the current 5% GST rate. In this case, only States would be able to recover their tax revenue losses.

- Electric two-wheeled vehicles may not have to depend on preferential GST treatment beyond 2030. There can be room to raise the GST rate to 18%, provided they continue to benefit from the MV tax exemption and current demand incentives.

Figure ES1 summarises the possible tax scenarios based on the EV cost-competitiveness analysis.

One may view this outcome with some degree of scepticism. The study’s results are indicative and conditional. Among the array of factors, the assumed value for average daily vehicle kilometres (VKM) for a certain vehicle segment has a substantial bearing on the results. Although effort has been made to arrive at a reasonable average value, real-world usage varies widely and lacks robust data. The analysis is also contingent on the possible decline in Li-ion battery price. Despite this caveat, the given assessment has the merit of providing visibility of the possible scope for the government to rationalise the existing tax incentives for EV buyers.

Q&A with authors

What is the core message of your paper?

The guiding principle is to strike a balance between promoting adoption of EVs by keeping them cost-competitive with ICE counterparts and reducing revenue losses to the government from EV tax incentives.

Although the recent GST reforms (entailing decrease in ICE vehicle taxes from 28% to 18% with continued 5% tax rate on EVs) have widened the on-road price gap between electric and conventional vehicles, using a total cost of ownership (TCO) framework, the study finds that privately owned electric cars will likely remain reliant on tax incentives until at least 2030. In contrast, electric commercial cars and two-wheelers are already approaching competitiveness, allowing for gradual withdrawal or rationalisation of certain tax concessions for these EVs. This will potentially help free up some fiscal bandwidth of the government to redirect its resources towards decarbonising harder-to-abate sectors such as heavy road transport, aviation, and shipping.

What presents the biggest challenge?

The analysis is contingent on the consideration that consumers base their purchase decisions on the lifetime costs of vehicles rather than the upfront vehicle cost. Creating awareness among consumers regarding the costs and benefits of EVs and how to assess the resulting financial merit is important. This is a time-taking proposition.

What presents the biggest opportunity?

Electric commercial cars and two-wheelers are already approaching competitiveness, allowing for gradual tapering of certain tax concessions for these EVs. This will potentially help free up some fiscal bandwidth of the government to redirect its resources towards decarbonising harder-to-abate sectors such as heavy road transport, aviation, and shipping.

Shyamasis Das

Tarandeep Kaur

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.