Editor's Note

This policy brief is a part of CSEP’s edited report Connectivity and Cooperation in the Bay of Bengal Region

Abstract

DOWNLOADS

Despite numerous examples to illustrate that dominating the maritime sector is a significant contributor to regional economic growth, the Bay of Bengal region, with its strong geographical advantages, did not explore its full potential in the maritime sector. This region lies strategically halfway along the East-West trade lane, and connects India, a major economy, to the rest of the world. However, the maritime logistics facilities, including seaports, in this region focus on intra-region competition rather than exploring a win-win solution through regional cooperation to develop synergetic power to outperform competitors outside the region. Besides the major ports located in Sri Lanka, India, and Bangladesh, ports in Singapore and Malaysia too, play a vital role in serving the Bay of Bengal region, creating overlapping market coverage. Owing to geographical characteristics, hub and spoke networks dominate in the Bay of Bengal region, allowing major ports such as Colombo and Singapore to be promoted as transshipment hubs. Despite the deviation distance and infrastructure limitations, Indian ports attract some transshipment cargo from Indian feeder ports. However, high network connectivity, together with a strong cargo base, is essential to sustain a transshipment hub in a competitive market. The intense competition among ports in this region discourages the concentration of maritime networks and transshipment cargo at a single port, thereby decreasing competitiveness of the region.

While focusing on the transshipment hubs in the Bay of Bengal region, this policy brief addresses the connectivity and cooperation deficit in the maritime sector, and the associated untapped potential that hinders regional development. Best-case scenarios for regional development are presented and analysed. Policy recommendations are provided as actionable steps for realising goals, while also addressing issues concerning stakeholders, and resource constraints.

Introduction

As the most economical mode of transportation for international freight distribution, maritime shipping contributes significantly to economic growth, especially in regions that have geographical advantages. The Bay of Bengal region is strategically located halfway along the East-West trade lane. Despite this, the countries in the region have not been able to leverage the full potential of their location. One of the reasons for this is the infrastructural limitation at the hub and feeder ports in the region.

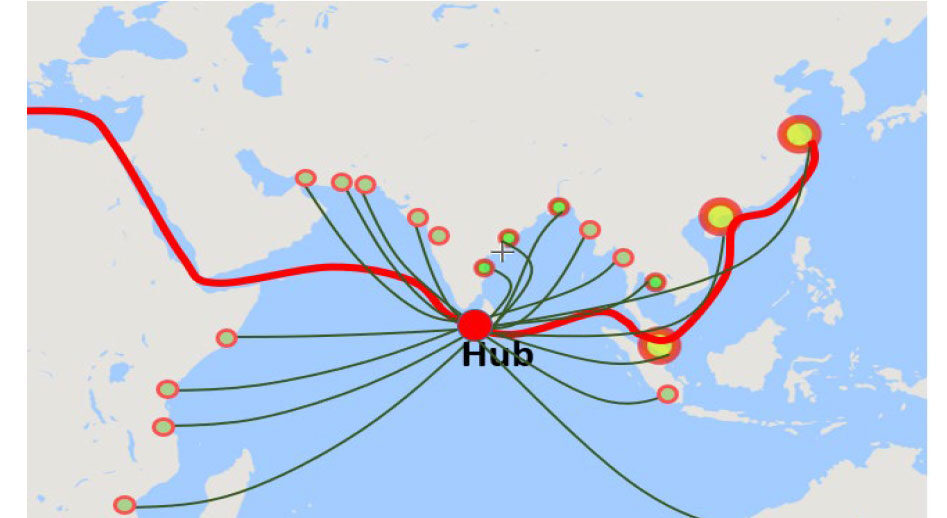

The hub and spoke configuration of maritime networks optimises transport cost by linking the large mainline vessels and small feeder vessels between the origin and destination ports. This model helps to overcome the infrastructure constraints associated with some ports in the region. In the Bay of Bengal region, for instance, the hub and spoke networks are centred on the Port of Colombo, as illustrated in Figure 1, which helps in overcoming the infrastructure limitations at Indian feeder ports, such a draft, terminal handling capacity etc. Other than Hub and Spoke networks, the relay networks improve voyage cost by integrating multiple mainline services. A transshipment hub port is vital in both networks to facilitate an economic space for cargo handling activities.

Figure 1. Hub and spoke networks centred on the Port of Colombo

Source: Developed by the author

Considering their contribution to regional economic growth, the key players such as port authorities, terminal operators, logistics service providers, among others in the Bay of Bengal region should embrace new strategies to enhance the entire port-based value chain. However, due to intense market competition and conflicting objectives, the interactions among these players have become complicated. For example, in India and Sri Lanka, different parties operate the ports, and they focus on maximising port-level profit rather than developing a common framework for the economic well-being of the countries and the region (Kavirathna, Hanaoka & Kawasaki, 2022). Although the cost-driven approaches of shipping lines such as strategic alliances, vessel size enlargement, limiting ports of call, and hub hopping encourage port operators to balance their competitive interactions, they still focus on enforcing competitive power over each other.

The Hub and Feeder Ports in the Bay of Bengal Region

In the Bay of Bengal region, the Port of Colombo is a significant transshipment hub serving the South Asian and a part of the African feeder markets, with transshipment cargo comprising over 75% of the share in port throughput. Colombo serves the Indian sub-continent feeder market because many major shipping services do not call directly at Indian ports due to the latter’s infrastructure limitations in accommodating larger vessels, and the greater deviation from the trunk sea route required to access these ports. However, India has made a significant effort in the last decade to develop port infrastructure, enabling Indian ports to accommodate larger vessels. Due to these developments and the growth in captive cargo volume, mainline services have commenced direct calling at Indian major ports, degrading the transshipment volume at Colombo. As stated by Kawasaki, Tagawa, and Kavirathna (2022), the Colombo and Nhava Sheva ports receive 30 and 16 vessel calls respectively from East Asian services per week, and both ports receive 10 vessel calls from European services per week in 2018. Therefore, Nhava Sheva has only 2.1% transshipment rate at Colombo. However, the V. O. Chidambaranar Port (also known as Tuticorin port) in Tamil Nadu, India, does not receive vessel calls from European and East Asian direct services, and hence has a 73.5% transshipment rate at Colombo. The authors have highlighted that even relatively smaller Indian ports in the Bay of Bengal such as Tuticorin, Krishnapatnam, and Visakhapatnam would obtain direct routes to Europe and East Asia if high Indian cargo demand and port expansions support potential de-hubbing.

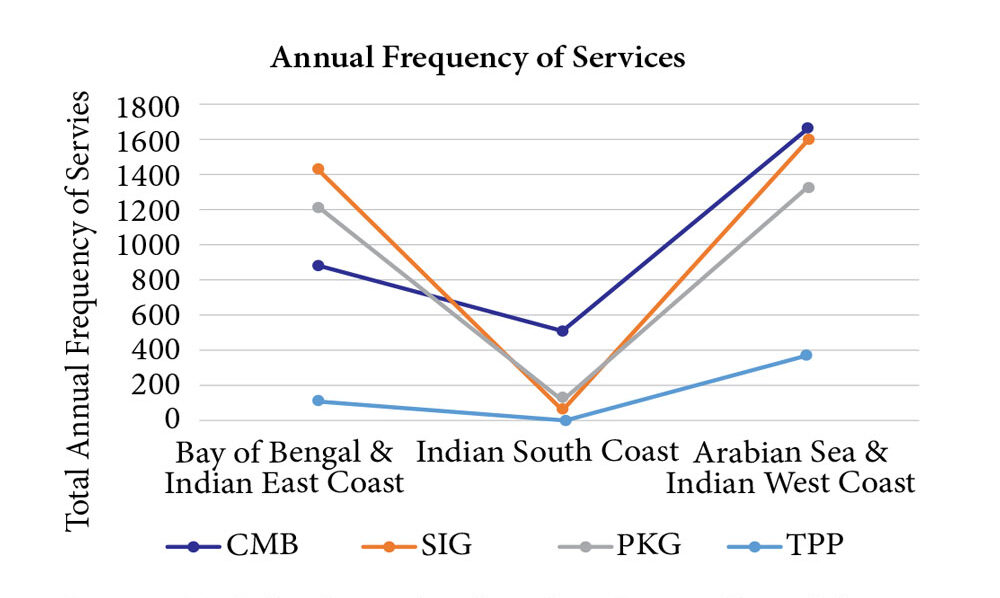

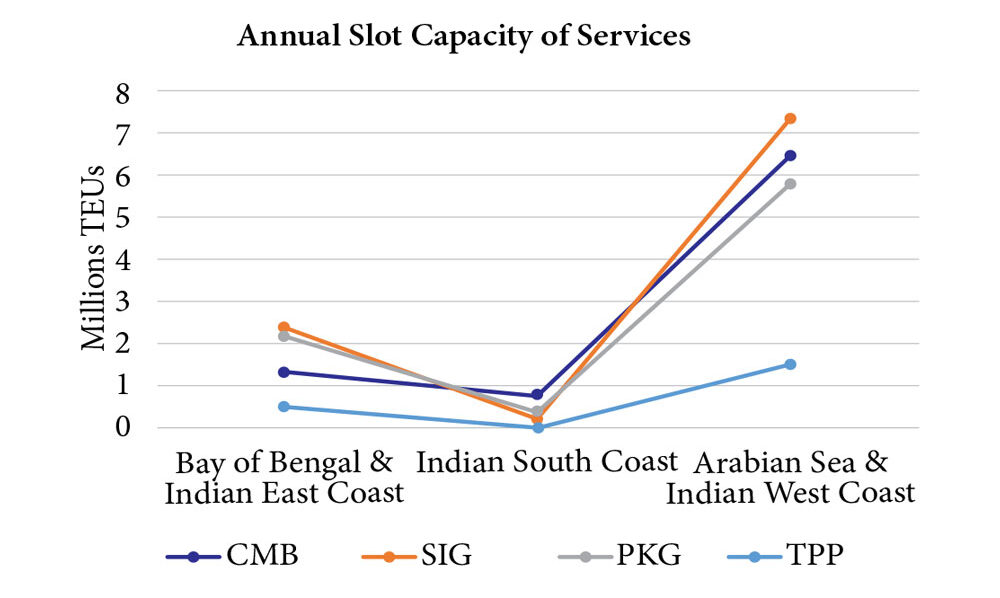

Although the competition between Colombo and Indian major ports is highlighted, a hub port competition can extend beyond regional boundaries. With multiple hub ports possibly serving the same feeder market, the Bay of Bengal region experiences cross-regional hub port competition. Therefore, ports in Singapore and Malaysia also play a vital role in serving the Bay of Bengal region, creating overlapping market coverage for South Asian and Southeast Asian hub ports. Hence, Colombo and Indian major ports experience competition from neighbouring hub ports such as Singapore, Kelang, and Tanjung Pelepas. An analysis of shipping services between the Indian feeder ports and these cross-regional hub ports indicates that except for Tuticorin and Cochin ports in South India, most other feeder ports have a high service frequency with Southeast Asian hub ports (Kavirathna et al., 2018a). Figure 2 shows the total annual frequencies and slot capacities of services connecting Indian East, South, and West-coast feeder markets and four competitive hub ports, indicating strong competition among hub ports in serving these feeder markets. According to the Lloyd’s List Intelligence (2020) port ranking, Colombo is ranked below the Southeast Asian hub ports, and Indian ports have even lower rankings. Although Colombo or Indian major ports do not have a significant role in relay networks, other neighbouring hub ports such as Singapore, Tanjung Pelepas, etc. would also take relay transshipments due to their high network connectivity. Despite these challenges from cross-regional hub ports, the South Asian ports compete rather than explore a win-win solution through regional cooperation to develop a synergetic power to out-perform competitors from other regions.

Figure 2. Annual frequency and slot capacity of services connecting hub ports and feeder markets.

Source: Made by the author based on Data collected from MDS Transmodal Inc.

Note: Colombo, Singapore, Kelang, Tanjung and Pelepas are abbreviated as CMB, SIG, PKG, TPP respectively.

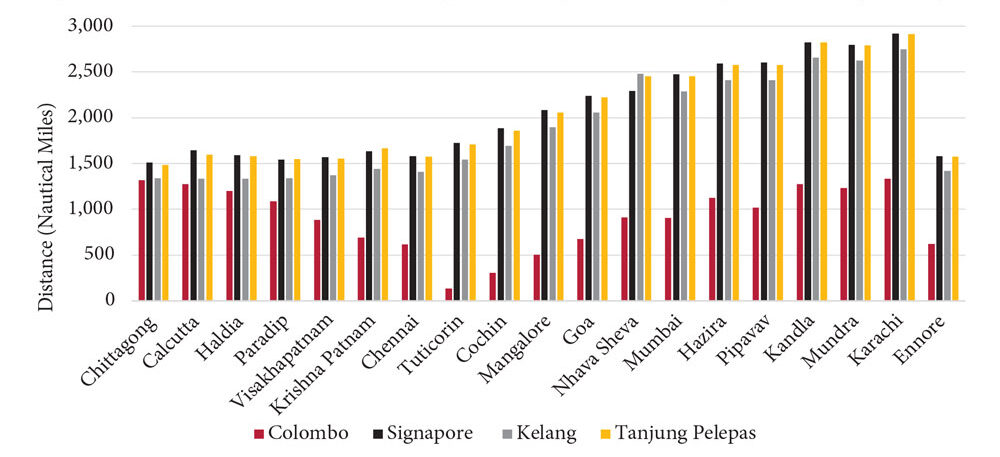

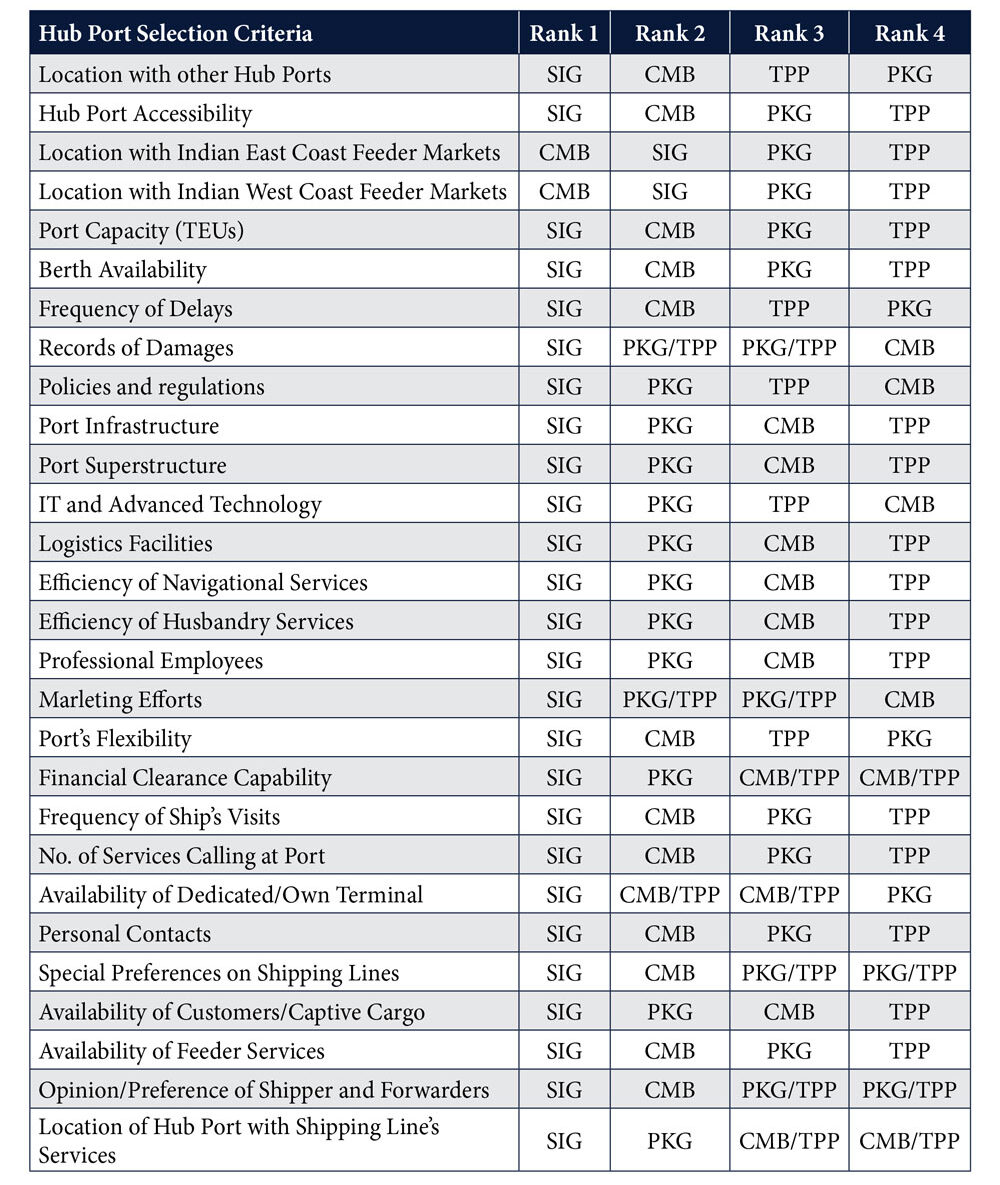

To exploit the advantages of the Bay of Bengal region, its maritime logistics facilities must be utilised most effectively. Shipping lines prefer a minimum voyage cost when optimising a hub and spoke network. Thus, the maximum usage of hub ports in this region would enable shipping lines to reduce feeder costs because these regional hub ports are located closer to the feeder market, as illustrated in Figure 3, where Colombo has significantly shorter distances with all feeder ports than the Southeast Asian hub ports. However, high network connectivity and a strong cargo base are essential for a transshipment hub to attract shipping lines. The intense competition among regional ports discourages the concentration of maritime networks at a single port, thereby decreasing the region’s competitiveness. Thus, the proximity of Colombo or Indian major ports to the South Asian feeder market with a potential of saving voyage costs does not guarantee high transshipment volumes. This is because shipping lines would consider multiple factors beyond the transport cost when selecting a transshipment hub, as illustrated in Table 1 which shows the higher performance of Singapore in numerous hub port selection criteria. As a result, import and export cargo of South Asia would be transported via maritime networks with high voyage costs, degrading their competitiveness in the world commodity market. Moreover, reducing vessel calls at regional ports diminishes the additional income generated from bunkering and other ancillary services. Hence, the cooperation deficits in this region have roots in the untapped potential that hinder regional development. The vulnerability of the transshipment market creates adverse impacts for the entire region.

Figure 3. Feeder link distance between competitive hub ports and feeder ports in the Bay of Bengal

Source: Voyage Planner, Marine Traffic (www.marinetraffic.com)

Table 1. Performance of competitive hub ports concerning hub port selection criteria

Source: Kavirathna et al. (2018)

Note: Colombo, Singapore, Kelang, Tanjung and Pelepas are abbreviated as CMB, SIG, PKG, TPP respectively.

Maintaining Buoyancy Between Competition and Cooperation

Strategically, an ideal way to address the cooperation deficits in the Bay of Bengal region would be to have an appropriate balance between the extreme ends of competition and cooperation among market players. Such a balanced approach derives strategic implications for players in the same market to create win-win outcomes rather than fostering traditional win-loss outcomes. If this strategy is applied to the ports in the Bay of Bengal region, they would cooperate with each other to create a bigger business opportunity for the entire region while also competing to absorb a large portion of this expanded business opportunity. Since this policy encourages simultaneous competition and cooperation among regional ports, it is essential to identify the areas where they should cooperate or compete with each other. For example, if the regional ports have an extreme price competition, and each port tries to attract more shipping lines by lowering the port charges than their competitors, this unhealthy competition will eventually result in a discounted average port charge for the entire region, and shipping lines would benefit from a high bargaining power. However, port operators and investors will not benefit from a discounted port charge, and the attractiveness of the entire region would be adversely affected. Also, extreme competition encourages port operators to focus on individual profits leaving fewer avenues for sharing resources and competencies to reduce negative externalities. Conversely, if ports have an extreme level of cooperation, the market would have a monopolistic high price, which would eventually reduce its attractiveness for the shipping lines. Moreover, extreme cooperation discourages port operators from innovation, specialisation, and enhancing operational efficiencies. Thus, an appropriate balance between competition and cooperation will enable win-win outcomes for the entire region.

Value creation and value capture are the fundamental concepts for drawing up policy objectives. Value creation addresses the common benefit of cooperation among ports in the region such that all ports would benefit from it. For example, value creation efforts can be devoted to enhancing the region’s competitiveness by drawing up regional tariff and rebate policies, developing the regional export sector, and creating joint marketing campaigns for shipping lines. With that, the Bay of Bengal maritime market can be expanded with more business opportunities enhancing regional economic growth. On the other hand, value capture is the individual effort made by each port to enhance its competitiveness. Therefore, while maintaining regional cooperation for value creation of the entire region, each port makes an effort at value-capturing to perceive more individual benefits from expanded business opportunities in the region. The next section emphasizes on several policy objectives to address the cooperation deficits among ports in order to exploit the untapped potential in this region, considering the short, medium, and long-term perspectives.

In the short-term, regional ports should cooperate on addressing existing market challenges such as shipping line alliances and hub-hopping, among others. As for value capturing, each port should make an effective port marketing effort which is currently lacking in this region. As discussed by Notteboom, Pallis, and Rodrigue (2022), a survey carried out in Europe revealed that 81% of port authorities lead their port marketing activities, and a survey of 70 cruise ports in the Mediterranean Sea indicates that 71.4% of port authorities lead their port marketing activities. Accordingly, their port marketing strategies deal with a network of stakeholders, including three main categories: business-related stakeholders (e.g., shipping lines, terminal operators, logistics companies), societal groups and local communities, and institutional stakeholders focusing on policy and legislative interventions. Moreover, port operators can cooperate to share underutilised port infrastructure and reduce port congestion. Port performance should also be enhanced considering qualitative aspects because shipping lines consider numerous factors for hub port selection. While attracting transshipment cargo, ports should cooperate on generating additional revenue from ancillary services and common user facilities.

The captive cargo volume can be increased in the medium term by developing regional imports and exports. Moreover, regional ports should consider optimising maritime networks to secure the most economical network configuration for international trade. Hence, the competitiveness of import and export cargo in the world commodity market should be enhanced by lowering transport costs. Since hub port competition is affected by shipping lines, port authorities, terminal operators, and other logistics service providers, an effective integration among them should be one of the medium-term objectives.

In the long term, it is essential to have an effective functional allotment for regional ports and clarify the transshipment hub status. The regional port operators should get together to discuss the directions for port development with a long-term master plan. Port customers should get the best possible deals with service providers without jeopardising their possibilities of enhancing the infrastructure and services. Port efficiency can be enhanced by encouraging private-sector involvement in port operations.

Although policy interventions address the regional cooperation deficit, significant challenges and constraints would influence achieving those objectives. Developing countries in the region have to overcome resource constraints of the maritime sector with the help of all stakeholders, including port administrators and operators, governmental bodies, international organisations, and shipping and logistics companies. The following section recommends measures to achieve these policy objectives.

Policy Options

An effective balance between competition and cooperation will not emerge voluntarily. Therefore, it is essential to enforce rules and/or incentives in the short term. Regional port cooperation should share resources and expertise to improve trade volume, assuring a sufficient cargo volume for shipping lines to enable their vessels to call at regional hub ports. Since global terminal operators have competitive advantages with economies of scale, expertise, and increased market power from a worldwide terminal network, inviting them to operate regional ports would enhance the market power of the entire region. Although several shipping services currently call at South Asian and neighbouring regional hub ports such as Colombo and Singapore simultaneously, calling at two adjacent regional ports by the same service will be limited in the future because shipping lines try to reduce their voyage costs. Therefore, vertical integration with shipping lines by offering dedicated terminals, on-arrival berths, and free dwell time for transshipment containers will encourage them to call at South Asian hub ports continuously. Moreover, governments may encourage shipping lines to invest in port infrastructure, giving them a sense of ownership in port facilities; thus, they would take initiatives to enhance port throughput. For example, offering concession agreements such as Build–Operate–Transfer (BOT) to shipping lines and rebates on port tariffs would enable shipping lines to invest in port facilities, especially if the port has geographical advantages. Also, port authorities should focus on developing supporting logistics infrastructure in the hinterland, such as high-capacity logistic corridors, multi-modal hubs, empty container depots, container freight stations, etc., while enabling advanced operations such as multi-country consolidations. A majority of the regional ports, especially in Sri Lanka and India, have severe issues with hinterland connectivity due to congested transport corridors and gaps in logistics infrastructure, which eventually decrease port competitiveness. Since a few shipping alliances dominate this region, vertical integration between alliances and port operators should be encouraged. Apart from developing infrastructure, it is essential to create professionals in maritime logistics to carry out efficient shipping agency functions and customs procedures, etc., to attract global shipping companies.

The possibility of hub port relocation is significant for transshipment markets. For instance, Maersk Sealand relocated its transshipment hub from Singapore to Tanjung Pelepas in 2000. Thus, ports should consider appropriate incentives to encourage shipping lines to relocate their transshipments from external hub ports to the Bay of Bengal region. Moreover, its connected markets should be expanded beyond the Indian sub-continent, especially targeting minor ports in East Africa and the Arabian Sea. Since an effective integration among market players is one of the medium-term objectives, Kavirathna et al. (2020a) highlighted the possible cooperation among terminals in Colombo to reduce port congestion and waiting time. Accordingly, despite their different ownership, Colombo Port’s terminals agree to handle excess vessels of competitive terminals when they have idle berth facilities, which guarantees the optimum utilisation of port infrastructure and high customer service with a potential for reducing over 1,600 hours of cumulative vessel waiting time per month at Colombo. The private sector can be involved in port operations by offering concession terminals. However, the profit-oriented objectives of private operators would have both positive and negative consequences; thus, effective enforcement is required from public port administrators.

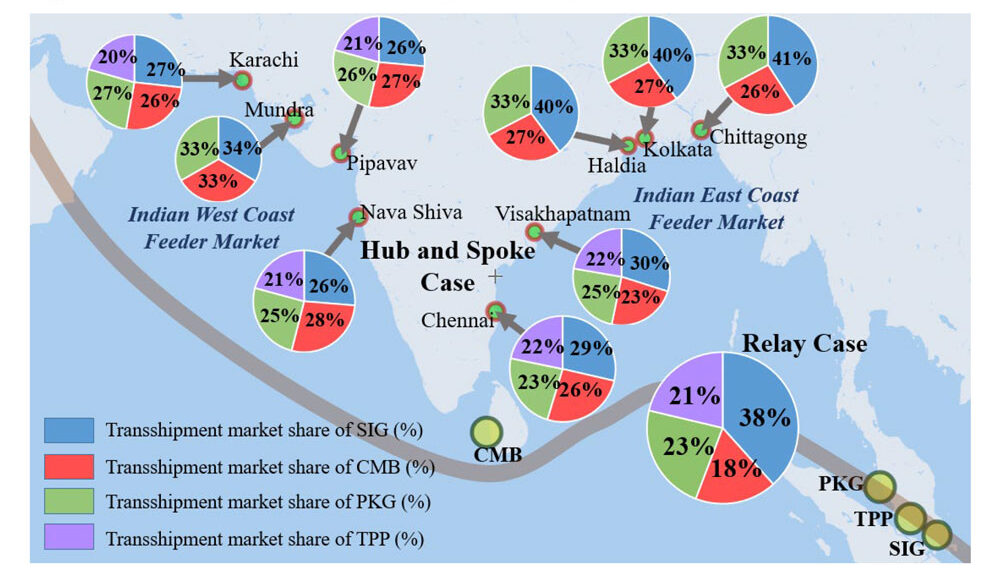

Kavirathna et al. (2018) have highlighted berth availability as the most critical factor for hub port selection. Moreover, feeder connectivity and high cargo volume are significant for hub and spoke networks. Therefore, this region should attract more feeder operators offering dedicated feeder berths and tariff rebates in the short term. However, improving cargo volume is essential in the long term to maintain a strong feeder network because feeder lines consider volume stability when allocating their vessel space to multiple mainlines. Moreover, geographical features play a significant role in westbound and eastbound voyages. When considering export cargo originating from India’s East coast and destined for the Far Eastern countries, using Southeast Asian hub ports would be an advantage. However, if these exports were destined for European countries, their transshipment at Colombo would be economical. However, these advantages are hard to absorb because the port selection is affected by many other factors. As illustrated in Figure 4, Kavirathna, Kawasaki and Hanaoka (2018) estimated that most Indian East coast feeder ports would offer higher transshipment volumes to Singapore than Colombo due to the high efficiency and network connectivity in Singapore, although Colombo is located closer to these feeder ports. Colombo and major Indian ports have less competitiveness in relay transshipments because of their poor network connectivity. Thus, ports should cooperate on developing a highly connected hub port within this region to optimise their maritime networks. Moreover, having a highly connected hub port would reduce waiting time for shippers and consignees, enhancing regional competitiveness.

Figure 4. Estimated market shares for competitive hub ports

Source: Kavirathna, Kawasaki and Hanaoka (2018)

Note: Colombo, Singapore, Kelang, Tanjung and Pelepas are abbreviated as CMB, SIG, PKG, TPP respectively.

Moreover, structural changes are observed in this region when changing the role of the feeder port to a direct calling port. For example, due to their adequate port infrastructure, Mundra and Nhava Sheva ports receive vessel calls directly from mainline services. Besides, India is trying to develop Vizhinjam port as a transshipment hub in the southern coastal area. Since India has a solid captive cargo base and the potential to serve several South Asian landlocked countries, creating its own transshipment hub would be possible. However, Chittagong port and some Indian minor ports still use Colombo as the central transshipment hub. Considering the least deviation of Colombo from the East-West trunk sea route, concentrating hub and spoke networks at Colombo would be ideal for this region. This is especially important because the feeder costs between Colombo and Indian East, South, and West-coast feeder ports might be lower than the costs of transporting containers via land transport corridors to their own transshipment hub due to the large land size of the Indian subcontinent. Therefore, port operators should develop a commonly agreed policy on ports’ function allotments to avoid over-investment in port development and unhealthy port competition. For example, in Sri Lanka, Hambantota port is being developed as a container port by China Merchant Port Holding, although the potential unhealthy competition between Colombo and Hambantota ports would threaten the transshipment hub status of Colombo (Kavirathna et al., 2020b).

However, attracting relay networks would reduce the vulnerability of Colombo’s transshipment volume even with these minor ports’ development. Besides, cooperation among regional ports on developing multi-modal transport infrastructure and outsourcing logistics would improve this transshipment market. For example, suppose one regional player has more competency in bunkering service, then other ports may outsource bunkering operations to this player, eventually reducing the overall cost with more economy-of-scale advantages. In the short term, cabotage restrictions can be reconsidered to offer more options for shipping lines to transport cargo within this region. Relaxing cabotage restrictions would encourage more global shipping companies to call at these regional ports, especially considering the potential growth in trade volumes from India and Bangladesh. Thus, the Bay of Bengal Initiative for Multi-Sectoral Technical and Economic Cooperation (BIMSTEC) members should agree on a liberal cabotage law while ensuring positive economic impacts for all members with an effective mechanism for sharing rewards. Due to the transshipment market competition, the market power of individual ports can be threatened if they continue to act as isolated entities. Therefore, port operators should synergise their competitive advantages to develop the Bay of Bengal region as the dominant maritime market in the world.

References

Kavirathna, C.A., Kawasaki, T. & Hanaoka, S. (2018). Transshipment hub port competitiveness of the port of Colombo against the major Southeast Asian hub ports. The Asian Journal of Shipping and Logistics, 34(2):71–82. Retrieved from http://doi.org/10.1016/j.ajsl.2018.06.004.

Kavirathna,A., Kawasaki, T., Hanaoka, S. & Matsuda, T. (2018a). Transshipment hub port selection criteria by shipping lines: The case of hub ports around the Bay of Bengal. Journal of Shipping and Trade, 3(4). Retrieved from https://doi.org/10.1186/s41072-018-0030-5.

Kavirathna C.A., Kawasaki, T., Hanaoka, S. & Bandara, Y.M. (2020a). Cooperation with a vessel transfer policy for coopetition among container terminals in a single port. Transport Policy, 89:1–12. Retrieved from http://doi.org/10.1016/j.tranpol.2020.01.010.

Kavirathna C. A., Hanaoka. S., Kawasaki, T. and Shimada, T. (2020b). Port development and competition between the Colombo and Hambantota ports in Sri Lanka. Case Studies on Transport Policy, vol. 9, no. 1, pp. 200–211. Retrieved from http://doi.org/10.1016/j.cstp.2020.12.003.

Kawasaki, T., Tagawa, H., Kavirathna, C.A. (2022). Vessel deployment and De-hubbing in maritime networks: A case study on Colombo Port and its Feeder Market. Journal of Marine Science and Engineering, 10(3), 304. Retrieved from http://doi.org/10.3390/jmse10030304.

Kavirathna C.A., Hanaoka, S. and Kawasaki, T. (2022). Terminal pricing decisions of the port authority and the global terminal operator of the competing ports in Sri Lanka. Journal of South Asian Logistics and Transport, 2(2), pp. 43-77. Retrieved from http://doi.org/10.4038/jsalt.v2i2.49.

Lloyd’s List Intelligence. (2020). One Hundred Ports, The Definitive Ranking of the World’s Largest Container Ports. Retrieved from https://lloydslist.maritimeintelligence.informa.com/one-hundred-container-ports-2020

MDS Transmodal Inc. (2016). MDS containership databank. Retrieved from https://www.mdst.co.uk/data

Notteboom, T., Pallis, A. and Rodrigue, J. (2022). Port Economics, Management and Policy, New York: Routledge. Retrieved from http://doi.org/10.4324/9780429318184.

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.