A High-Growth, Low-Emission Pathway for India: Results From REMIND

Reading Time: 8 minutesEditor's Note

This work was carried out in collaboration with the Potsdam Institute for Climate Impact Research (PIK), Germany. This is an author preprint.

DOWNLOADS

Executive Summary

India stands at a critical juncture in its development journey. With a population of 1.45 billion and aspirations to achieve high per-capita income by 2047, the country must simultaneously deliver on its commitment to reach net-zero CO₂ emissions by 2070. This study demonstrates that these objectives are not only compatible but mutually reinforcing, provided definitive action begins immediately.

The Challenge

India’s CO₂ emissions have more than doubled in the past two decades to 3 billion tonnes, making it the world’s third-largest emitter. Yet per-capita emissions remain well below the global average at 2 tonnes annually. The country’s energy system remains heavily dependent on coal, which accounts for over 70% of electricity generation, making the power sector the single largest source of emissions.

To achieve near-high-income levels, India must sustain gross domestic product (GDP) growth exceeding 6% annually through 2050, which correlates with increased energy consumption and, traditionally, higher emissions. The fundamental question is whether India can decouple economic growth from emissions while maintaining energy security and ensuring a just transition for affected communities.

Our Approach

This study employs a customised version of the REgional Model of Investments and Development (REMIND) integrated assessment model (IAM), developed by the Potsdam Institute for Climate Impact Research (PIK), Germany, to create a high-growth, low-carbon scenario for India. Unlike conventional scenarios that assume moderate growth (projecting per-capita income around US$7,230 by 2050), REMIND–India is calibrated to high GDP growth averaging 6.2% per annum (p.a.) over 2025–2050. This enables per-capita incomes to increase fourfold from current levels to approximately US$11,400 by mid-century, approaching high-income levels.

The model incorporates political economy constraints governing coal phase-out through explicit bounds on retirement rates, recognising the social and economic importance of existing energy infrastructure.

We compare two scenarios: a current policies scenario (Curr_pol) reflecting India’s emissions trajectory under the current level of effort and a net-zero 2070 scenario (NZ2070) that achieves zero CO₂ emissions by 2070 and is compatible with limiting global warming to 1.9°C. The analysis reveals several critical insights.

Key Findings

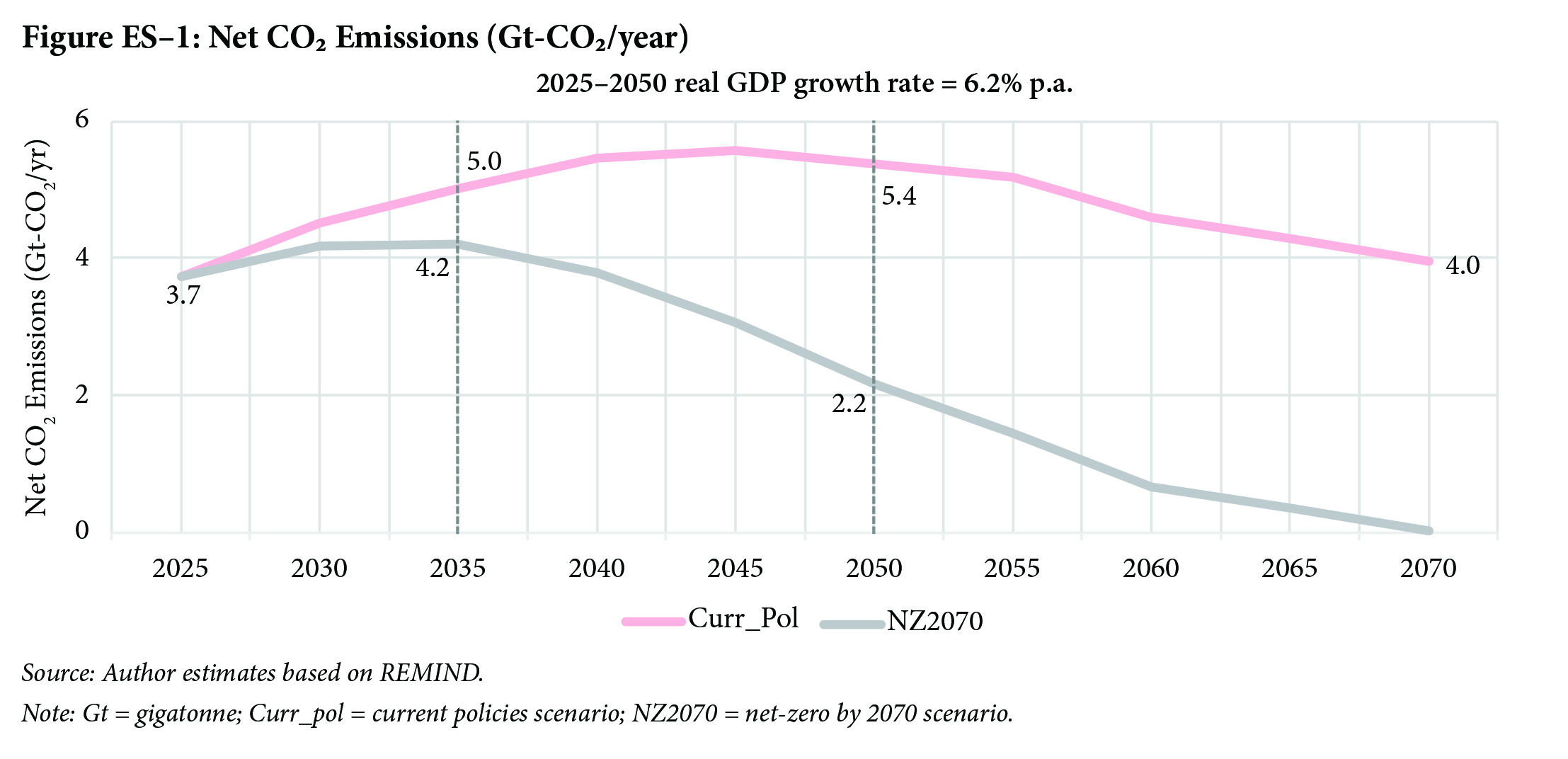

- Emissions Trajectory: Under the net-zero scenario, India’s emissions peak at 4.2 gigatonne (Gt)-CO₂ around 2035, before declining steadily to 2.2 Gt by 2050 and reaching net-zero by 2070. This contrasts sharply with the Curr_pol scenario, where emissions would continue to rise to 5.6 Gt by 2045 and decline only to 4 Gt by 2070 (Figure ES–1).The near-term increase in emissions in the net-zero pathway reflects continued fossil fuel use to meet growing energy demand during economic expansion, albeit at lower levels than under current policies. Crucially, this period lays essential groundwork—renewable capacity expansion, grid modernisation, and end-use transformation—that enables rapid decarbonisation post-2035.

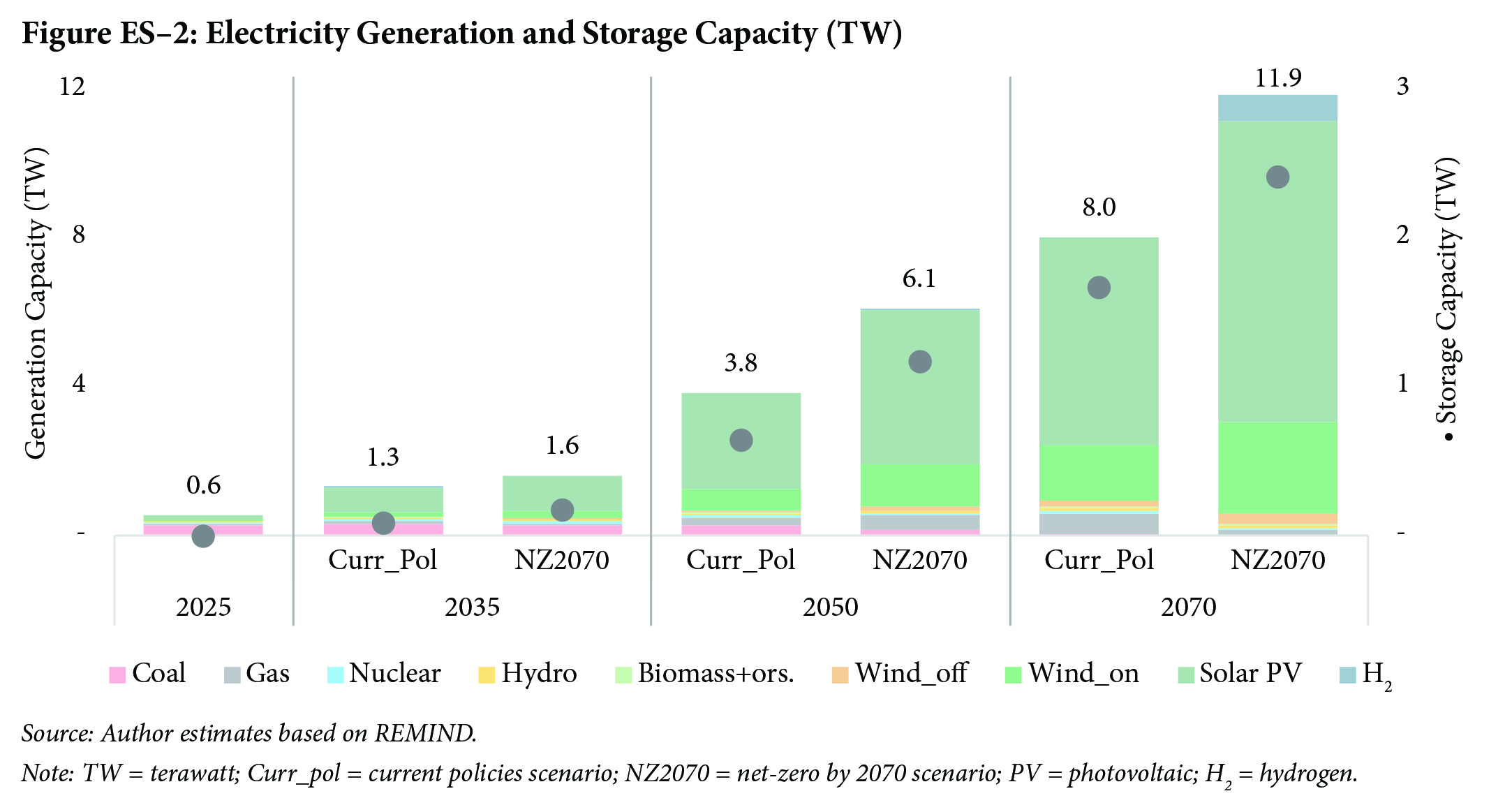

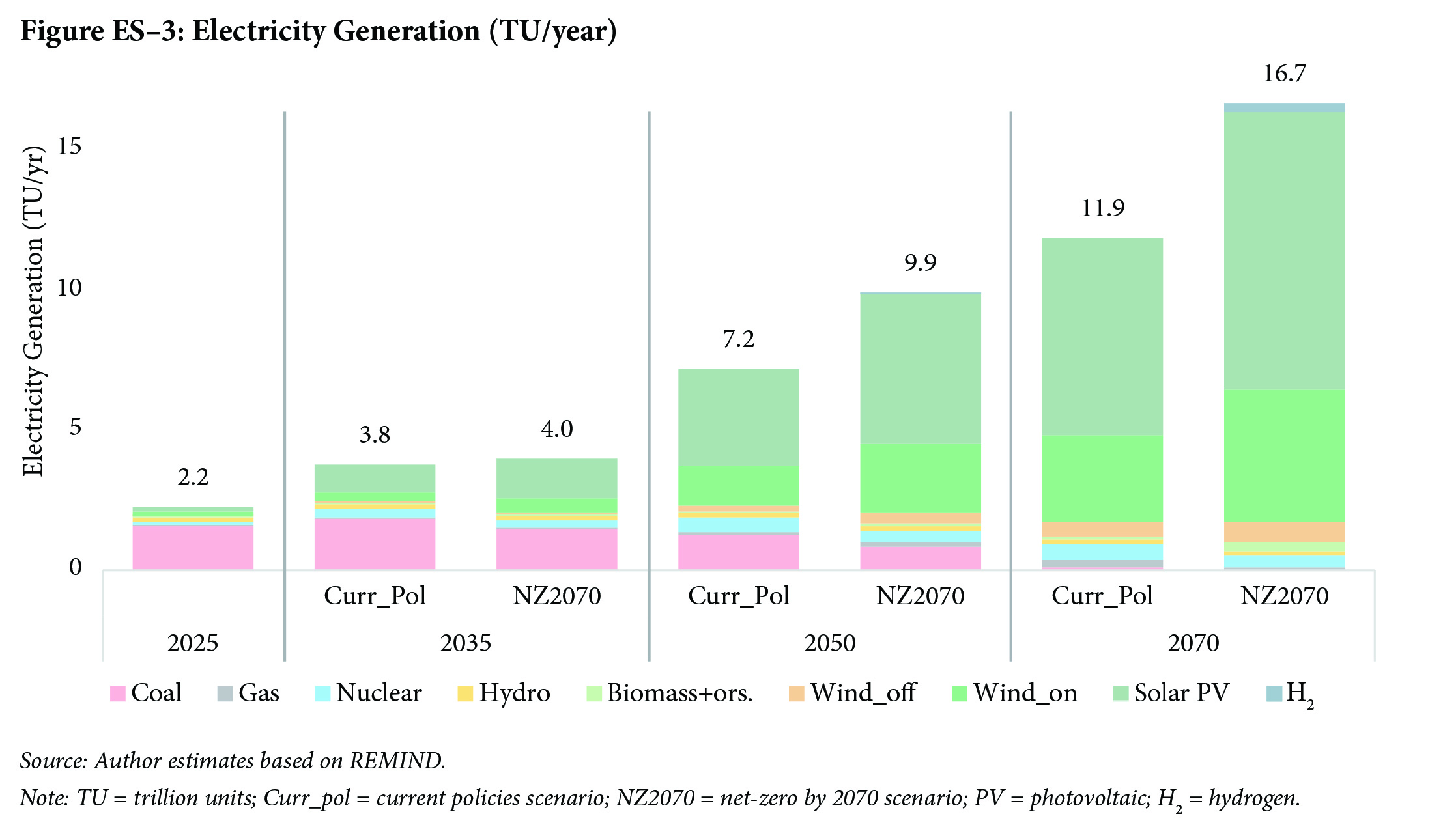

- Power Sector Transformation: The electricity sector undergoes extensive transformation. Total generation capacity must expand from 0.6 terawatts (TW) currently to 1.6 TW by 2035 and 6.1 TW by 2050, driven overwhelmingly by solar and wind deployment (Figure ES–2). Non-hydro renewables would generate 52% of total electricity by 2035, rising to 84% by 2050 and 96% by 2070 (Figure ES–3).Coal generation capacity is estimated to peak around 2030 at 293 GW before declining gradually to 230 GW by 2040, 158 GW by 2050, and phasing out entirely before 2070 (Figure ES–2). This measured approach avoids premature asset stranding while preventing new coal lock-in and minimising political–economic disruption from coal phase-out.

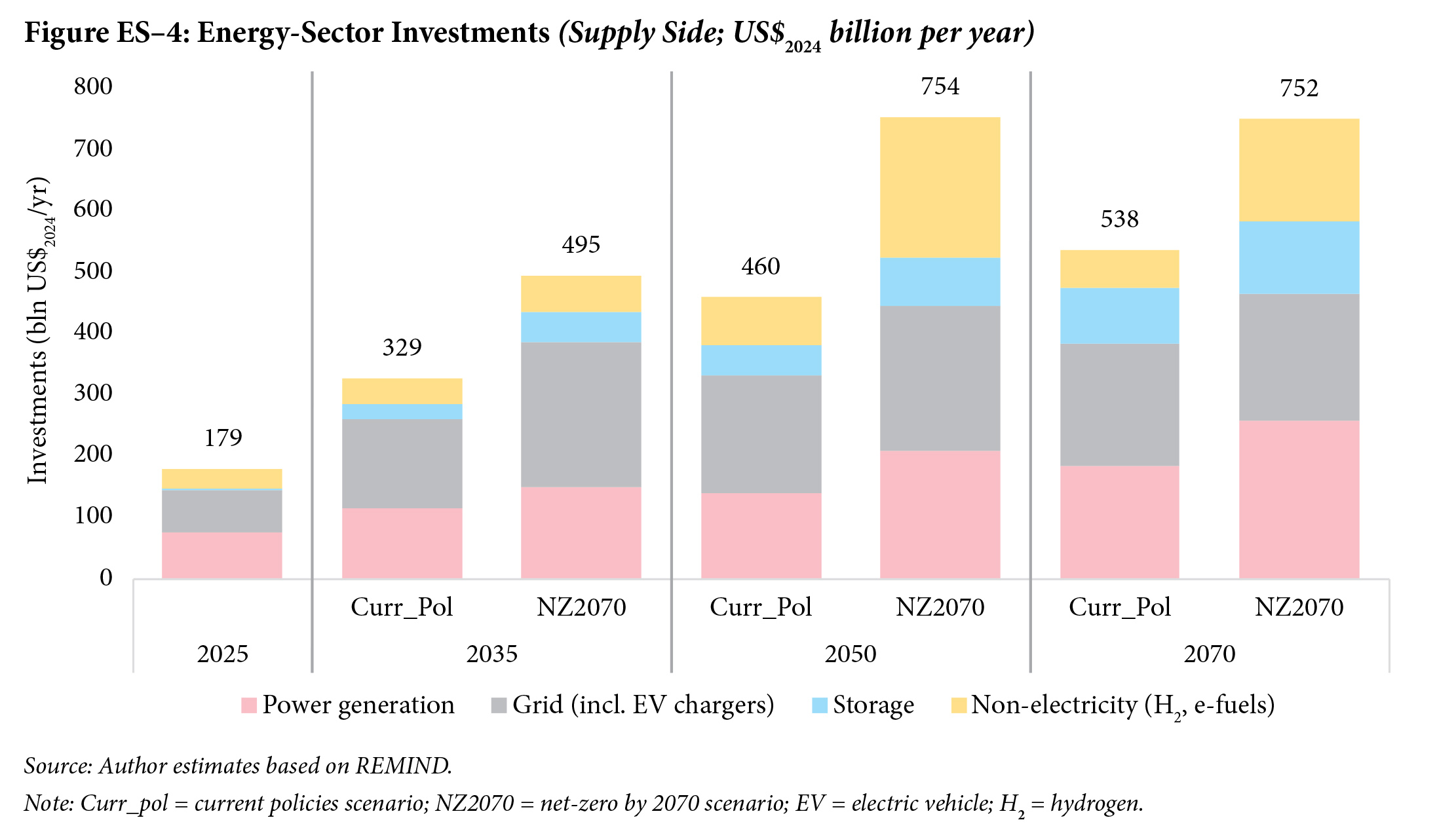

- Energy Storage and Grid Infrastructure: Massive renewable deployment necessitates parallel expansion of storage and transmission infrastructure. Storage capacity must reach 172 GW by 2035—double the level projected under current policies—to balance supply from variable renewable sources (Figure ES–2). By 2050, storage capacity must reach 1.1 TW, complemented by green hydrogen (gH₂)-based generation to provide long-duration seasonal storage.Grid investments must more than triple to approximately US$236 billion annually by 2035, representing half of all energy-sector investments during this period—60% higher than under current policies. This expansion is critical as renewable generation will occur predominantly in Renewable Energy (RE)-rich regions in the northwest and the south, distant from many major demand centres. Without commensurate transmission capacity, clean energy would be curtailed and fossil fuel reliance would continue.

- Electrification and Efficiency: Electricity’s share in final energy (FE) must increase from about 20% currently to 50% by 2050, reflecting significant shifts in transport, industry, and buildings.Electrification, combined with fuel switching to renewables and efficiency improvements, enables energy intensity of GDP to decline from 2.3 GJ/US$ currently to 0.83 GJ/US$ by 2050.

- Industrial Decarbonisation: Steel production is projected to nearly triple to 460 Mt by 2050, with production shifting from conventional blast furnace routes towards direct reduction processes using gas and, ultimately, gH₂ and electric arc furnaces (EAFs) using scrap.Cement production doubles to 670 Mt annually by mid-century, with carbon intensity falling from 0.6 to 0.25 tonnes of CO₂ per tonne of cement through increased use of alternative materials, energy efficiency, fuel switching, and ultimately carbon capture technology.

- Investment Requirements: The transition requires additional annual investment of approximately US$62 billion during 2026–2035, representing about 0.85% of GDP above current policy levels. This rises to approximately US$380 billion annually (1.55% of GDP) during 2036–2050. However, these investments would reduce expenditure on imported fossil fuels, resulting in savings of 1.2% of GDP through 2050.

Critically, about 80% of the total investment needs must be raised from domestic sources through higher savings, redirection of investments from brown to green sectors, innovative financing mechanisms (blended finance, green bonds, etc.), and additional private capital mobilisation. This would push general investment rates from 30–31% currently to 34% of GDP by 2035. The remaining 20% of the total, roughly US$51 billion annually in the near term, requires international climate finance scaled up to approximately six times the recent levels.

Policy Recommendations: The Five Pillars for 2035

Based on these findings, we propose five key pillars for India’s 2035 climate targets:

- Emission Intensity Reduction: Reduce emission intensity of GDP by 65% compared to 2005 levels, ensuring emissions peak around 2035 before declining. This represents a significant enhancement of the current 45% target for 2030.

- Renewable Energy (RE) Expansion: Achieve 80% of cumulative electric power installed capacity from non-fossil-fuel sources, with an objective of 1,200 GW of RE capacity (excluding large hydro) by 2035. This requires average annual capacity additions of 150 GW during 2030–2035, representing a 2.5-fold increase over current 2030 targets.

- Peaking and Phasing-Down Coal Generation: Peak unabated coal use for power generation before 2035, implying no new unabated coal plants commissioned post-2030, with existing plants beginning gradual retirement starting with older, inefficient units. This timeline provides adequate time to coal-producing states (which will see a decline in coal demand from 2040 onwards) for economic restructuring while preventing new coal lock-in.

- Accelerated Electrification: Double the rate of electrification across end-use sectors, prioritising railway traction, passenger vehicles, and light commercial vehicles in the near term, gradually expanding to other transport modes and industrial applications as technology costs decline.

- Expanded Carbon Market: Include the power sector in the forthcoming Carbon Credit Trading Scheme (CCTS) alongside industries already covered, with progressively tightened carbon intensity targets aligned with long-term emission trajectories.

Essential Enabling Policies

Beyond these targets, several enabling policies are critical:

- Energy Price Rationalisation: Current electricity pricing, characterised by extensive cross-subsidies, provides perverse incentives that discourage efficiency and undermine renewable competitiveness. Reforms eliminating wasteful subsidies while protecting vulnerable consumers through direct benefit transfers would improve system efficiency.

- Market Structure Reform: The electricity sector must shift from long-term agreements towards exchange-based trading mechanisms that accommodate renewable intermittency through real-time and day-ahead markets, enabling more efficient balancing of variable generation.

- Carbon Pricing: A carbon price reaching US$100 per tonne by 2035 would provide technology-neutral incentives for emissions reductions, generating revenues for clean energy investments and just transition programmes. As carbon pricing matures, existing mandates such as renewable purchase obligations (RPOs) would become obsolete, with market forces naturally driving the shift towards cleaner energy.

- Just Transition Measures: Coal-dependent states (Jharkhand, Odisha, Chhattisgarh, and parts of Madhya Pradesh) require comprehensive policies including retraining programmes, economic diversification strategies, and social protection measures to manage employment and revenue impacts. The geographic redistribution of economic benefits—with renewable-rich and relatively higher-income states (Rajasthan, Gujarat, Karnataka, Tamil Nadu, and Andhra Pradesh) gaining substantially—necessitates careful policy attention to distributional impacts.

The Cost of Delay

The timing of India’s decarbonisation efforts critically determines overall costs. Delayed action would necessitate deployment of expensive negative emission technologies (such as enhanced rock weathering [ERW] and carbon capture and storage [CCS]) post-2070 to compensate for excess emissions, with implicit carbon prices exceeding US$1,200 per tonne by 2080—nearly three times higher than the US$429 per tonne under the recommended pathway. These technologies remain largely unproven at scale and face significant resource constraints.

In contrast, the proposed pathway achieves net-zero through conventional mitigation measures, with investments coinciding with lower abatement costs and avoiding dependence on expensive and unproven technologies. The implicit carbon price rises from US$5.50 per tonne currently to US$100 by 2035 and US$241 by 2050, reflecting the increasing but manageable marginal cost of abatement.

Conclusion

This analysis establishes that India can pursue an ambitious growth trajectory while establishing a credible path to net-zero emissions by 2070. The critical insight is that actions taken over the next decade—the period through 2035—will lay the groundwork for accelerated decarbonisation when clean technologies become more mature and cost-competitive, yielding emission reductions in subsequent years.

The proposed targets represent an integrated strategy where renewable expansion, storage and grid investment, coal phase-out, electrification, and carbon pricing reinforce each other. The estimated investment requirements, while substantial, are manageable and far more efficient than the expensive corrections that delayed action would necessitate. India’s experience in navigating this transition could provide valuable lessons for other developing economies seeking to reconcile growth imperatives with climate responsibilities.

Keywords: India, Energy transition, Net-zero emissions, Climate policy, Renewable energy, Nationally Determined Contributions, Integrated Assessment Model, REMIND model, Viksit Bharat

Q&A with author

What is the core message of your paper?

Economic development and climate action are compatible with each other. Using the REMIND integrated assessment model, we show that India can sustain high economic growth — approaching high-income levels by 2050 — while achieving net-zero CO₂ emissions by 2070, consistent with the Paris Agreement. The key is a managed energy transition that peaks emissions around 2035, massively scales up renewable energy, accelerates electrification across transport and industry, and gradually phases out coal power generation. This would require additional investment of roughly 1.4% of GDP annually in the medium term in the energy supply sector: a manageable sum, especially given the savings from reduced fossil fuel imports and lowered burden of environmental externalities caused by fossil fuel use.

What presents the biggest challenge?

Mobilising investment at the required scale, and doing so equitably. The net-zero pathway requires roughly US$175 billion per year in additional energy investment over 2026–2050, of which at least 20% must come from international sources. This would imply external flows to India increasing multiple times from current levels, underscoring how far existing climate finance mechanisms fall short. Domestically, the transition will also create significant regional winners and losers: coal-producing states would face economic disruption even under a gradual phase-out in the absence of pre-emptive measures, while the benefits of renewable energy deployment will accrue disproportionately to states with high solar and wind energy potential. Without proactive just transition policies and economic diversification, political resistance from affected regions could undermine the entire effort.

What presents the biggest opportunity?

The energy transition is also India’s biggest economic development opportunity. As one of the world’s largest energy markets, India has the potential to build and scale competitive domestic manufacturing base in solar, wind, energy storage, green hydrogen, and electric vehicle industries, thus reducing import dependence on fossil fuels and capturing clean energy value chains at home. Decarbonisation would also deliver major co-benefits: improved energy security, dramatically reduced air pollution, and the creation of new industries and jobs. By creating an optimal policy framework and operationalising it, viz. rationalising energy prices, expanding carbon markets, and investing in grid infrastructure, the clean energy transition can serve as a powerful engine of the Viksit Bharat development vision.

Utkarsh Patel

Chen Chris Gong

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.