India E-Commerce Report 2026: Innovation in the Merchandise Space

Reading Time: 5 minutesDOWNLOADS

Executive Summary

Scale and Trajectory

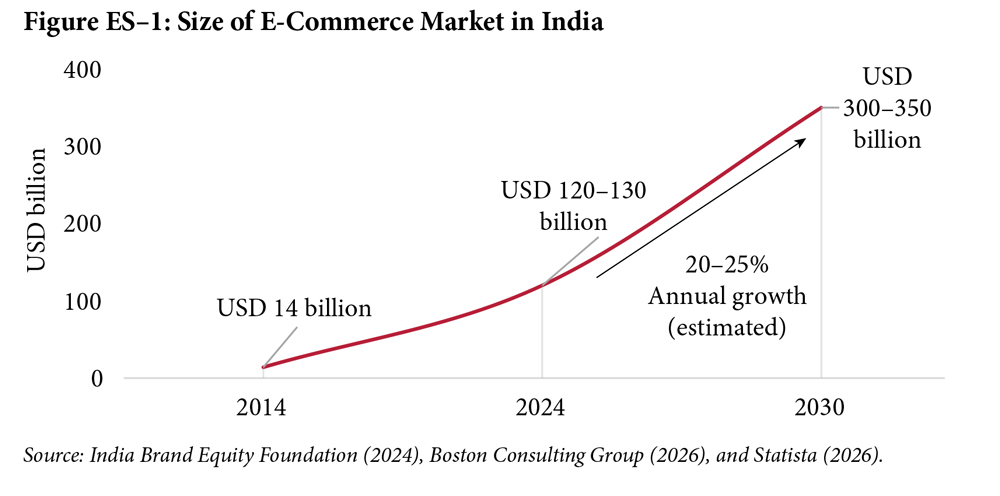

Over the past decade, India’s e-commerce market has expanded rapidly, from USD 14 billion in 2014 to about USD 120–130 billion by 2024, with most estimates pointing to sustained double-digit annual growth of 20–25% (Figure ES–1). Depending on definitions and coverage, projections suggest the market could reach anywhere between USD 300 and USD 350 billion by 2030. Even allowing for measurement challenges, the direction is unambiguous. E-commerce is no longer a peripheral activity but is becoming an increasingly central component of India’s economy. The analysis in this report focuses exclusively on the e-commerce of merchandise goods, excluding services such as travel, ticketing, and digital subscriptions.

At a time when the broader economy is undergoing structural changes, e-commerce has emerged as one of its most adaptive and innovative components. Growth in internet access, digital payments, and shifts in consumption behaviour have together created the foundation for digital commerce to scale. It is emerging as a core economic infrastructure that links buyers and sellers across geographies and lowers search and access costs. This transformation is visible not only in scale but in the widening scope of digital commerce across use cases, from consumer-facing retail to business-to-business (B2B) procurement, and across geographies from large urban centres to smaller towns. The variation reflects the complexity of the Indian market, where consumer preferences, firm capabilities, and regional conditions differ widely. Treating this ecosystem through a single regulatory lens risks distorting its evolution. Thus, policy must recognise this shift and provide stable, long-term signals that support sustained investment and innovation.

Market Structure and Concentration

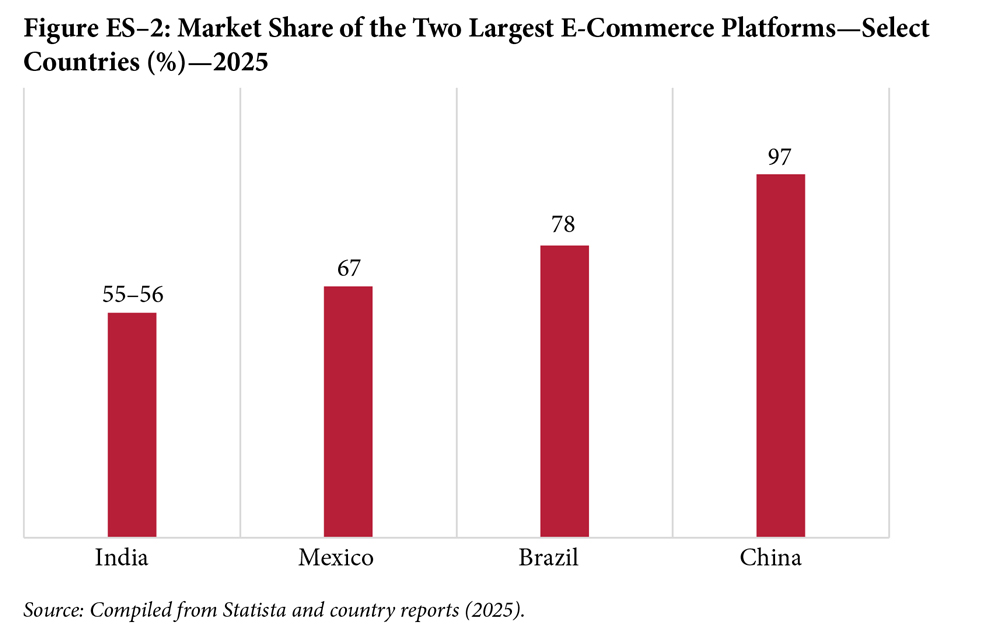

Concerns about market concentration in India’s e-commerce sector are understandable. Amazon and Flipkart (including affiliates such as Myntra and Shopsy) together hold about 55–65% of the market share, making them the clear leaders. Data on web traffic also show that these platforms account for about 87% of monthly visitors. Similar patterns of concentration appear in other large emerging markets: in China, Taobao and Tmall together represent about 97% of listed traffic; in Brazil, Mercado Livre and Amazon capture roughly 78%; and in Mexico, Amazon and Mercado Libre account for around 67% (Figure ES–2). Therefore, some degree of concentration appears to be a fundamental outcome of platform economics. Scale economies, network effects, and logistics efficiencies tend to favour larger players. Thus, globally, e-commerce markets tend to evolve toward oligopolistic and even duopolistic structures.

These concerns should, however, be viewed within context. High concentration does not necessarily imply the presence of entry barriers, and entry barriers are not necessarily insurmountable. The continued emergence of smaller and niche players across segments suggests that the market remains open to entry: New entrants are able to grow by differentiating their business models or targeting specific consumer groups. This ongoing churn is an important feature of the sector’s dynamism. In a geographically dispersed country like India, scale is often necessary to reduce unit cost of transactions and make delivery networks viable.

The Profitability Puzzle

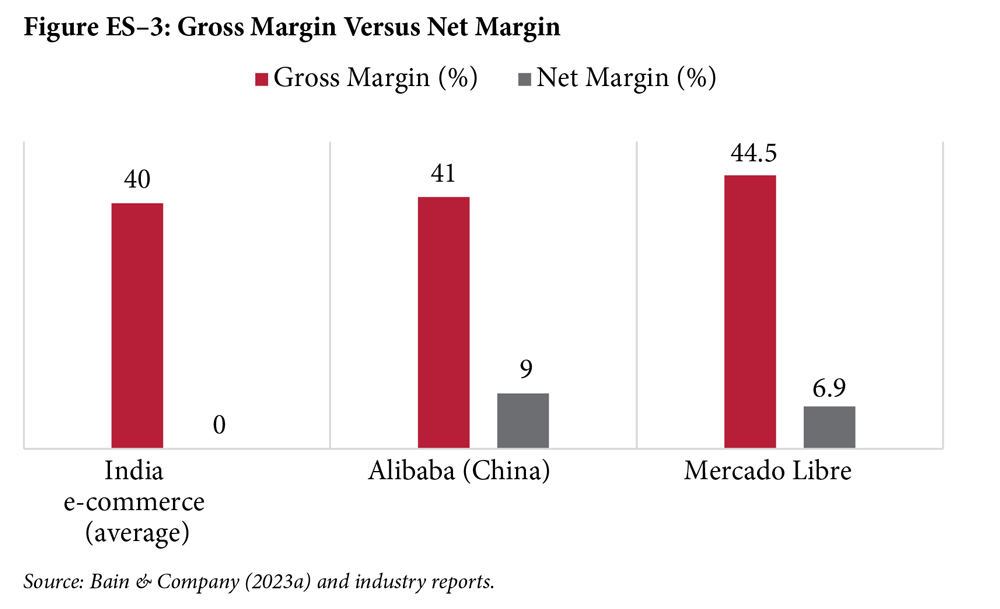

The more pressing constraints lie elsewhere. Despite gross margins of around 40–43% at the platform level, the sector remains largely unprofitable at the net margin level in India. In contrast, China’s Alibaba reports gross margins of 40–41% alongside net margins of about 9% every year. Similarly, Mercado Libre in Brazil and Mexico recorded a gross margin of 44.5% and a net margin of 6.9% in 2025, even while continuing to invest in logistics, free shipping, and fintech.

This cross-country comparison underscores some deeper concerns that can be classified into (i) operational and (ii) regulatory.

At the operational level, average revenue per user (ARPU) in India remains low at roughly USD 107 compared to USD 1,330 in China, USD 514 in Mexico, and USD 350 in Brazil. Average order values (AOVs) are also lower at INR 500–700 (USD 5–7) in Tier-2 and Tier-3 cities versus INR 900 (USD 9) and above in Tier-1 cities. These patterns are reinforced by an almost 50% reliance on cash-on-delivery (COD). Cost structures further compress margins. Industry evidence suggests that logistics and fulfilment, including warehousing, represent the largest cost burden, with last-mile delivery constituting roughly 60% of total logistics cost per parcel. Additionally, return rates range between 25 and 40% in India, relative to 16.9–24.5% globally. Reverse logistics, restocking, and product devaluation add significantly to cost pressures, particularly in fashion and electronics.

These challenges are structural. They arise from the nature of the industry, India’s geographic dispersion, heterogeneous demand patterns, and relatively low purchasing power. They help explain why profitability remains elusive despite scale, and why the challenge is less about market concentration and more about cost economics.

Gaps in the Policy Conversation

At the same time, important gaps in the policy and regulatory conversation remain. First, the most critical gap lies in measurement. Without consistent definitions and robust, standardised data, it is difficult to accurately assess market shares, competitive dynamics, or even the true size of the sector. In fact, while large volumes of data are generated within the ecosystem, the availability of consistent, aggregated, and usable data for public analysis remains limited. This naturally impacts the quality of policy formulation and regulation.

Second, a clear gap persists between regulations on paper and their actual implementation. Under India’s foreign direct investment (FDI) policy, 100% FDI is permitted under the automatic route in the marketplace model, where platforms act purely as facilitators between buyers and sellers without owning or controlling inventory. In contrast, the inventory-led model, where the platform owns the goods and sells directly to consumers, is prohibited for foreign investment. In practice, however, this distinction is often blurred. Platforms have circumvented rules through indirect control over inventory and pricing, and these instances reveal that operational realities often override formal boundaries, raising serious doubts about effective enforcement. Thus, blanket restrictions on FDI, limits on platform ownership, or caps on scale are blunt structural tools. They risk harming the sector’s profitability, reducing competition, discouraging fresh investment, and slowing innovation and growth. Instead, specific anti-competitive behaviour, such as predatory pricing, exclusive seller deals, self-preferencing, and abuse of dominance, should be directly scrutinised and penalised where proven.

Third, despite their central role, issues concerning gig workers, who form the backbone of e-commerce logistics and last-mile delivery, have received disproportionately limited attention in policy discussions. As the sector expands rapidly, critical questions around earnings instability, unpredictable working conditions, and inadequate social security protections remain largely unresolved. The growth of e-commerce risks exacerbating precarious employment, widening inequalities, and undermining the very workforce that sustains its efficiency and scale. In this context, despite the much-publicised ban on “10-minute delivery” advertisements, quick commerce continues to expand rapidly with little change on the ground. Consequently, worker safety remains a serious and unresolved concern.

The Way Forward

In this context, the role of policy is best seen as enabling rather than prescriptive. India has already made significant progress in building the foundations of digital commerce through investments in public digital infrastructure, payments systems, and connectivity. The next phase will depend on maintaining a policy environment that is predictable, supportive of innovation, and responsive to emerging challenges. Excessive intervention risks stifling innovation, while insufficient oversight may raise legitimate concerns around fairness and consumer protection.

E-commerce in India is still evolving. Its strength lies not just in its size but in its ability to adapt, experiment, and expand into new segments of the economy. Preserving this dynamism, while ensuring fair and open markets, will be key to sustaining its contribution to growth and opportunity in the years ahead.

Overall e-commerce in India is a highly dynamic and innovative sector, confronting multiple structural challenges but endowed with strong inherent advantages. International experience, particularly from China, suggests that facilitative and balanced policy frameworks can enhance the sector’s contribution to growth and livelihood creation. Evidence from other developing countries also indicates that domestic and international players can coexist, underscoring the need for a level playing field that encourages firm-level innovation rather than creating artificial barriers.

Laveesh Bhandari

Janak Raj

Aashi Gupta

Indramani Tiwari

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.