The Hidden Cost of Cesses and Surcharges for Indian States

Reading Time: 4 minutesEven as the states’ share has risen, the pool of taxes being shared has been shrinking

Over the years, India’s Finance Commissions have steadily increased the share of Union taxes that goes to states. On the surface, this looks like an encouraging shift towards greater fiscal decentralisation. However, there is more to it than meets the eye. Even as the states’ share has risen, the pool of taxes being shared has been shrinking, and this has quietly reshaped how much states actually receive.

On average, around 87% of total Union Gross Tax Revenue (GTR) was part of the divisible pool in the early 2010s. Today, the average is closer to 78%, a drop of nearly 9 percentage points

A Smaller Pool Behind a Bigger Share

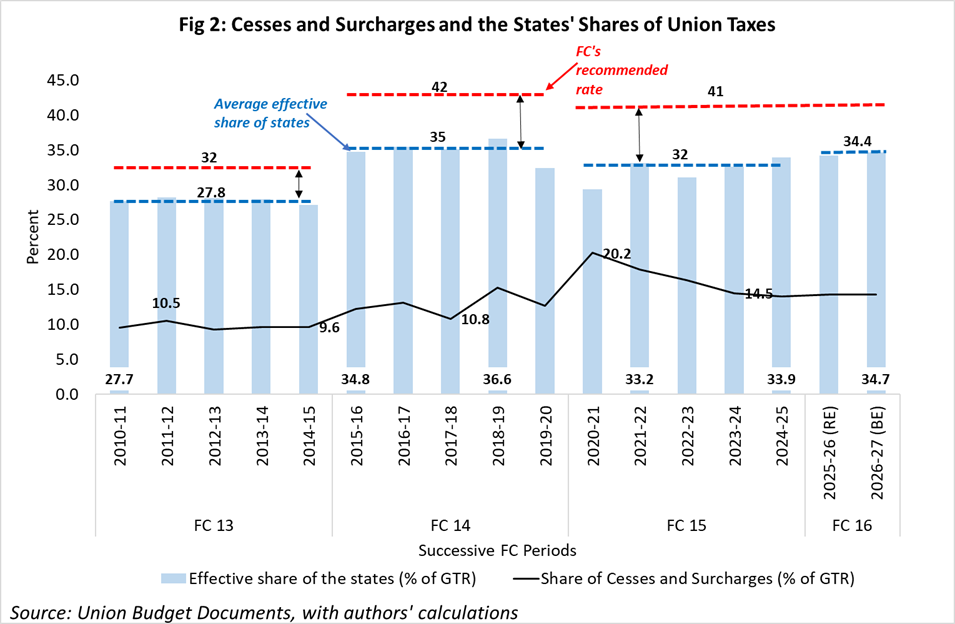

The Finance Commission decides what percentage of central taxes should be transferred to states. This share rose from 32% under the Thirteenth Finance Commission (FC13, 2010–15) to 42% under the Fourteenth Commission (FC14), and currently stands at 41%.

Although this suggests a significant increase in resources devolving to the states, it must be noted that this applies only to the “divisible pool”[1]—the portion of total Union tax collections that is “shareable” with states. However, this pool itself has been shrinking. On average, around 87% of total Union Gross Tax Revenue (GTR) was part of the divisible pool in the early 2010s. Today, the average is closer to 78%, a drop of nearly 9 percentage points (Figure 1). In other words, states now receive a higher share of tax resources, but from a smaller base.

Why Is the Divisible Pool Shrinking?

The key reason lies in the growing use of cesses and surcharges, which are special levies that, under the constitutional framework (Articles 270 and 271), are not shared with the states. They are deducted from GTR before the divisible pool is calculated, along with other deductions, such as the cost of collection and taxes accruing to union territories.

While surcharges are typically applied to income and corporate taxes, a cess is earmarked for a specific purpose like education, infrastructure, health, or disaster relief.

Because these levies are excluded from the divisible pool, any increase in them directly reduces the amount of revenue available for sharing with states. These deductions are often unavoidable as they are legally mandated to finance specific national priorities.

Their share in total tax revenue rose from about 9.5% in 2010-11 to a peak of over 20% in 2020-21, and currently remains elevated at around 14-16%.

A Decade of Rising Cesses and Surcharges

Over the past decade, cesses and surcharges have become increasingly important in the centre’s tax strategy. The centre has relied more on these instruments to raise revenue to offset the higher share of taxes that must be transferred to states. Their share in total tax revenue rose from about 9.5% in 2010–11 (Figure 2) to a peak of over 20% in 2020–21, and currently remains elevated at around 14–16%. This trend predates the pandemic but intensified during it, when the government relied more on such levies, especially fuel-linked cesses, to raise revenues.

Relative to GDP, these revenues also increased from ~1.2–1.3% before COVID to ~1.8–2.0% thereafter. This suggests that their use has remained persistent even as the tax system has evolved, particularly since the rollout of the Goods and Services Tax (GST) in 2017. The GST enveloped many older, smaller levies into broader groups (e.g., merger of Krishi Kalyan, Clean Environment, and Swachh Bharat cess). Thus, today, the system relies mostly on a few high-value cesses like the Road and Infrastructure Cess on fuel, the National Calamity Contingent Duty, and the Agriculture Infrastructure and Development Cess on items like gold and alcohol. One notable exception is the GST Compensation Cess, which was uniquely designed to compensate states for revenue shortfalls during the transition to the new tax regime.

Because a growing portion of revenue is raised through cesses and surcharges, which are excluded from sharing, the effective share is lower than the recommended share.

What This Means for States

To understand the real impact, it is useful to distinguish between two concepts: the recommended share by the Finance Commission (e.g., 41%) and the effective shares, which are what states actually receive as a share of total tax revenue (GTR). The two are not the same. Because a growing portion of revenue is raised through cesses and surcharges, which are excluded from sharing, the effective share is lower than the recommended share. Across successive Finance Commission periods, this gap has widened from about 4 percentage points (FC13) to around 7 percentage points (FC14 period) and about 8–9 percentage points in the recently concluded period of the Fifteenth Finance Commission (Figure 2).

Thus, although the official devolution rate increased, the actual share reaching states has not kept pace.

Why This Matters for the Economy

First, many cesses, especially on fuels and essential goods, operate as implicit taxes that are passed on to consumers through higher prices. It therefore impacts the consumers or households. Such levies can also be regressive, as lower-income households end up paying disproportionately larger shares of their incomes, because all consumers face similar prices.

The Comptroller and Auditor General (CAG) flagged that INR 3.69 lakh crore of cess collections had not been transferred to the designated reserve funds as of March 2024.

Second, from a public finance perspective, higher effective tax burdens can distort economic behaviour by negatively impacting consumption, investment, and compliance. Over time, persistent reliance on such levies can raise the overall tax burden and potentially dampen economic activity.

Third, there are concerns regarding transparency. Cesses are assigned for specific purposes, but the link between collection and actual spending is not straightforward or apparent. For instance, the Comptroller and Auditor General (CAG) flagged that INR 3.69 lakh crore of cess collections had not been transferred to the designated reserve funds as of March 2024[2]. The same audit pointed out that several reserve funds with balances exceeding INR 800 crore had remained inactive for long periods, suggesting they may have outlived their original purpose and require review. Such findings raise questions about accountability, transferability, and actual use of funds collected.

The debate is not just about how much revenue is raised by the government, but how it is raised. A growing reliance on cesses and surcharges can reduce the resources available for devolution to the states, shift tax burden in ways that may be regressive, especially when consumption-based, and undermine overall fiscal transparency.

Kritima Bhapta

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.