MacroInsights: Rupee Pressures—Then and Now: Why This Isn’t 2013 but a Structural BoP Problem

Reading Time: 3 minutesMacroInsights, a Centre for Social and Economic Progress (CSEP) series, dissects key economic developments and policy issues of macroeconomic significance. It offers timely, evidence-based analysis to inform public debate and policymaking.

Three months into the West Asian war, the rupee remains under pressure despite aggressive RBI intervention, tighter restrictions on derivatives activity, and higher duties on precious metals. A broader set of measures was introduced to bridge the external financing gap, mostly replicating the 2013 playbook. But the current episode is different: it reflects a balance-of-payments (BoP) problem rooted in long-standing structural weaknesses, not just a war-driven shock or a repeat of 2013.

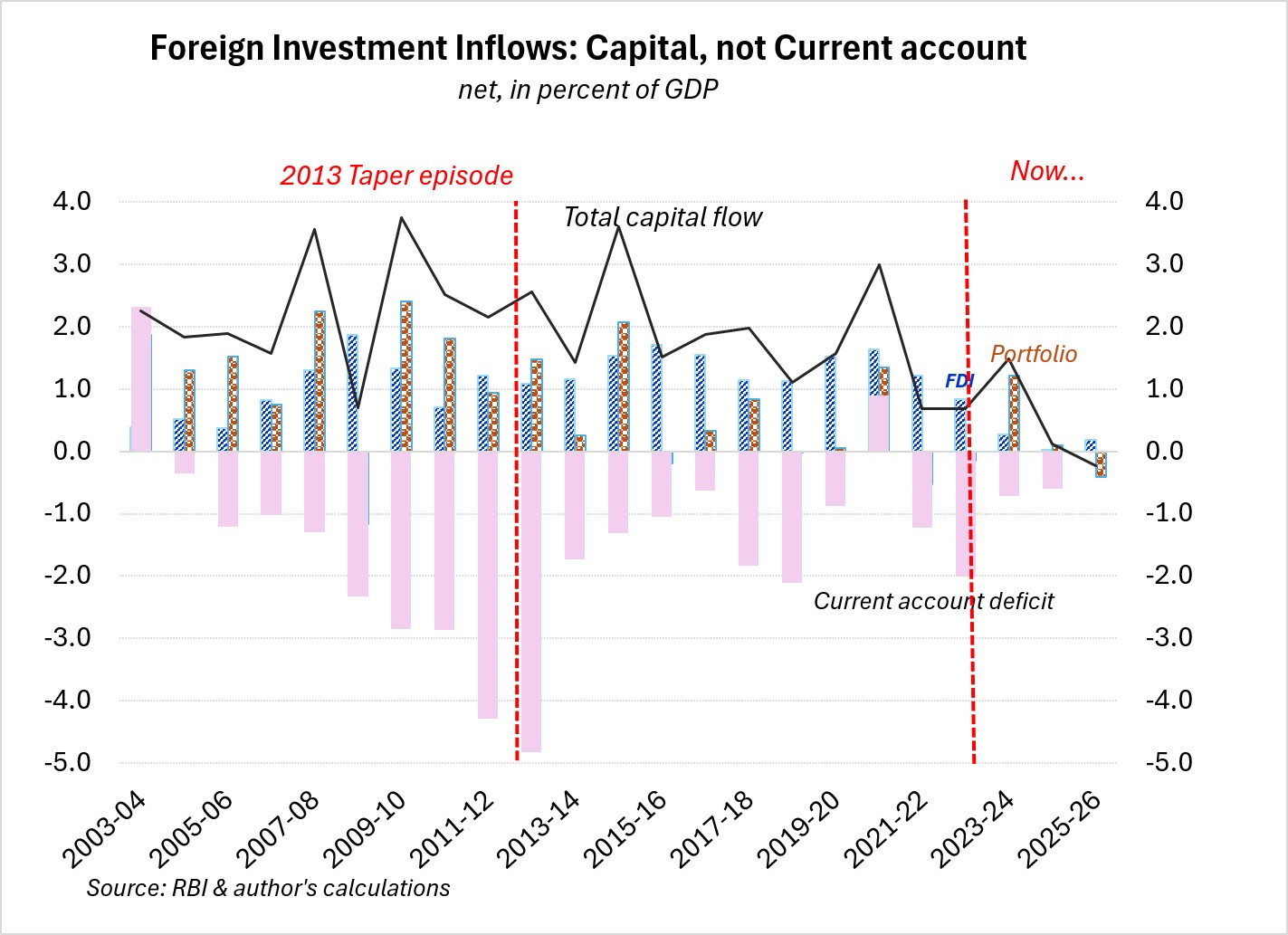

Unlike 2013, this crisis reflects a chronic foreign capital deficit, not a current account shock. The 2013 taper episode was driven by current account dynamics (Chart 1). This time, in three of the four years leading up to 2025–26—well before the West Asia shock— India’s BoP was in deficit, drawing down reserves. Foreign capital, especially direct investment, has been draining out, making even moderate current account deficits difficult to finance.

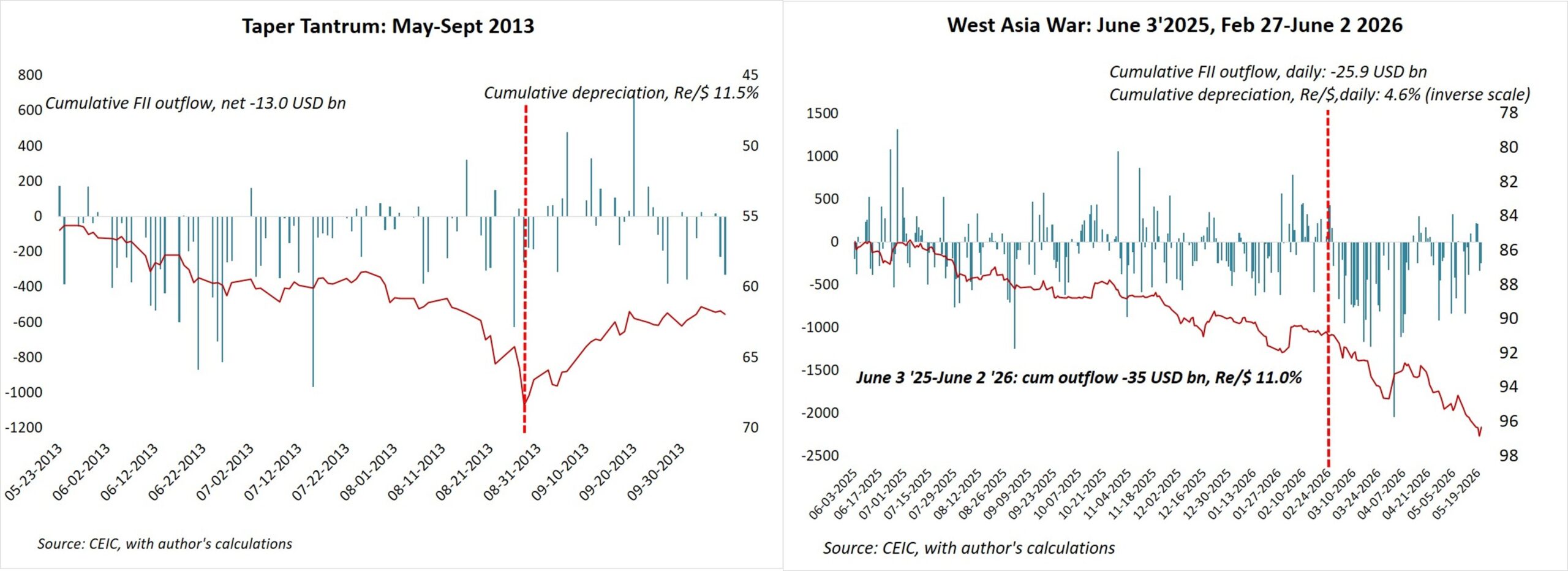

After the outbreak of the West Asia war on February 27, portfolio outflows accelerated to roughly double the level seen during the four taper-tantrum months of 2013, yet with only half the currency depreciation (Chart 2), cushioned by massive RBI spot and forward interventions. Even so, between FY22–FY26, the rupee fell from Rs 74.5 to Rs 88 per dollar.

Oil-driven current account widening compounds an already strained BoP. To check speculative pressures, the RBI restricted derivatives in April. Next, gold and silver duties were raised in May. In 2013, such curbs compressed the current account sharply—from 6.7% of GDP in Oct–Dec 2012 to 1.2% by Jul–Sept 2013. The oil backdrop was far less forgiving—average crude oil import prices persisted above US$100/bbl for three years then (2011–12 to 2013–14) versus three months now—underlining today’s greater vulnerability.

The rupee’s downslide persists despite larger reserves’ firepower—US$663 billion in February 2026 vs US$287 billion in May 2013—but the forward book is more encumbered. It stood at US$104 billion in March 2026, including US$30 billion from three-year buy/sell swaps, compared to US$32.6 billion in 2013, when a forward liability of that size could be offset by mobilising US$34.3 billion in NRI deposits. Today, a chronic BoP deficit and a three-times-larger forward overhang mean any additional external borrowing is costlier, compounding medium-term FX liabilities and worsening the outlook.

The June 5 measures from the government and RBI aim to attract foreign capital and plug the BoP gap, but at greater cost and risk. These extend tax incentives for sovereign debt with a widened scope, permit NRI-OCI investments into Indian equities, provide concessional forex swaps from RBI for public-sector entities’ overseas borrowings, and absorb hedging costs for banks raising FCNR(B) deposits until September 2026. The cost is higher now, with a domestic policy rate of 5.25%, a US Fed funds rate of 3.5–3.75%, and an expected depreciation of ~6%. The RBI’s exchange-rate risk assumption on its balance sheet to attract hard currency for rupee stabilisation weighs against the unwinding of the stretched maturities in 2029–31.

The West Asia shock has exposed a structural difficulty in attracting and retaining foreign capital, limiting 2013’s relevance for the current crisis. A common expectation is FCNR deposit mobilisation in the $50–70 bn range, enough to meet FY27 external financing needs. Sovereign debt incentives could result in passive debt inflows from future inclusion in global bond indices. The first may indeed buy some time, while the latter remains to materialise—portfolio debt inflows responded briefly to previous reforms, falling thereafter. Overall, these are temporary stabilisers amidst more enduring fundamental pressures. They are not a substitute for structural adjustment.

Renu Kohli

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.