Examining the Carbon Border Adjustment Mechanism: Issues and Challenges

Reading Time: 7 minutesIn 2021, the European Union (EU) proposed the Carbon Border Adjustment Mechanism (CBAM) as a part of its “Fit for 55” package which aims to achieve a 55% decrease in overall greenhouse gas emissions by 2030. The EU-CBAM is a tool designed to establish fair prices for the carbon emitted during the production of carbon-intensive goods that are imported into the EU (European Commission, 2023a). The proposed mechanism applies to a limited number of goods which include iron and steel, aluminium, fertiliser, cement, electricity, and hydrogen. It commenced its transition phase in October 2023 and is set to move into its permanent phase starting January 1, 2026.

The EU-CBAM is a tool designed to establish fair prices for the carbon emitted during the production of carbon-intensive goods that are imported into the EU.

The primary objective of CBAM is to mitigate the risk of carbon leakage[1] and level the competitive field for European industries actively engaged in decarbonising their economy. These industries have been bearing the costs associated with domestic emissions, and CBAM seeks to ensure proper accounting and pricing of the carbon content in imported goods. However, it is criticised as a trade-restrictive policy, particularly by developing countries because of the complexity of verifying the emissions embedded in imports which affects the competitiveness of energy-intensive trade-exposed (EITE) sectors.

While the EU-CBAM is proposed as an effort to address carbon emissions, it is important to scrutinise its effect across various dimensions and assess how it may shape the future of trade and economic development. This discussion will delve into the multifaceted issues of CBAM, examining its design and development in light of equity challenges, its compliance with international trade laws, and the broader implications for global trade and economies.

- World Trade Organization Compliance

The CBAM’s compatibility with World Trade Organization (WTO) principles, including Most-Favoured-Nation Treatment (MFN)[2] (General Agreement on Tariffs and Trade [GATT] Article I) and National Treatment[3] (GATT Article III) is a crucial aspect. While the EU claims that CBAM is compliant with these international trade regulations (European Commission, 2023b), the issue remains intricate and is expected to encounter challenges under international trade legislation. An example of this complexity lies in CBAM’s recognition of market-based carbon prices paid in exporting countries but not for equivalent carbon abatement costs imposed through regulatory measures. Additionally, the calculation of embedded emissions under CBAM relies on non-product-related processes and production methods (NPR PPMs) of goods manufactured outside the EU, conflicting with the principles of non-discrimination in GATT and its general exceptions. However, in the long run, as CBAM replaces the phased-out free allowances under the EU Emission Trading System (ETS), it could be viewed as compatible with WTO rules, as both domestic producers and importers would bear the full carbon cost of their products, which the EU has also stressed.

- Equity and Development

The imposition of CBAM by the EU also raises concerns about potential violations of the Common but Differentiated Responsibilities (CBDR)[4] principle under the UN Framework Convention on Climate Change (UNFCCC). CBAM aims to equalise carbon pricing regardless of its origin, imposing equivalent carbon policies globally. This inadvertently puts pressure on exporting nations, particularly developing and Least Developed Countries (LDCs) to adopt carbon policies equivalent to developed countries, pushing for equal rather than differentiated responsibilities. This shift introduces disparities in costs for exporters and intensifies trade imbalances for LDCs, creating a scenario commonly referred to as a “race to the bottom”. This will result in significant welfare losses for LDCs. Studies show that developing economies, particularly countries from Africa and Persian Gulf Arab states could face considerable tariffs due to the high carbon emissions intensities linked to their products. In addition, the economies that are highly dependent on fuel exports, such as Cameroon, Egypt, and Nigeria, would be among the hardest hit by CBAM (Perdana and Vielle, 2022 and Zimmer and Holzhausen, 2020).

The revenues generated from the imposition of CBAM will contribute to the EU’s budget, effectively serving as a revenue-generating mechanism for the EU.

More importantly, the revenues generated from the imposition of CBAM will contribute to the EU’s budget, effectively serving as a revenue-generating mechanism for the EU. Although the legislation regarding EU CBAM has outlined intentions to utilise the collected revenue for decarbonising manufacturing industries in less-developed countries, the EU Member States did not endorse this proposal and instead proposed that only a part of revenue should be redistributed to low-income EU trading partners. This raises concerns about how the revenue will be utilised, rather than supporting developing countries in achieving their carbon reduction objectives; the revenue generated from exporting nations to the EU will reinforce the EU’s ambitious carbon reduction commitments.

- Limited Climate Mitigation

The EU has proposed CBAM as an important climate measure because it is an extension of the EU ETS to imported goods, therefore, reducing carbon leakage and encouraging emissions reductions by countries with less efficient climate policies. Ex-ante studies show that carbon border adjustment policies can reduce carbon leakage and global CO2 emissions (European Parliament, 2020). However, the particular sectors covered by the EU CBAM consist of only a small proportion of global emissions. While addressing emissions from these product categories is a necessary step toward achieving net-zero goals, it alone is insufficient for a world committed to reaching carbon neutrality.

Furthermore, the potential of CBAM to contribute to global emission reduction only becomes significant when it garners support from domestic producers facing higher production costs due to carbon taxes and unfair competition from imports originating in regions without carbon taxes. Nevertheless, its impact remains limited, as countries subject to these tariffs can reroute their trade to alternative markets, and imports remain unaffected due to CBAM tariffs applying to only five specific groups of imported goods and specific to one region. Hence, it becomes evident that while CBAM holds promise as a tool to address carbon leakage and enhance competitive advantage, its potential to substantially reduce global emission trajectories is rather limited.

- Trade and Other Economic Implications

Given that CBAM takes the form of an import tax, it is expected that it will have a negative effect on trade with considerable variations across countries. This is because carbon tariffs will be imposed on imports of carbon-intensive goods, which could curtail trading partners’ exports, affecting the welfare and employment of both the developed and developing countries.

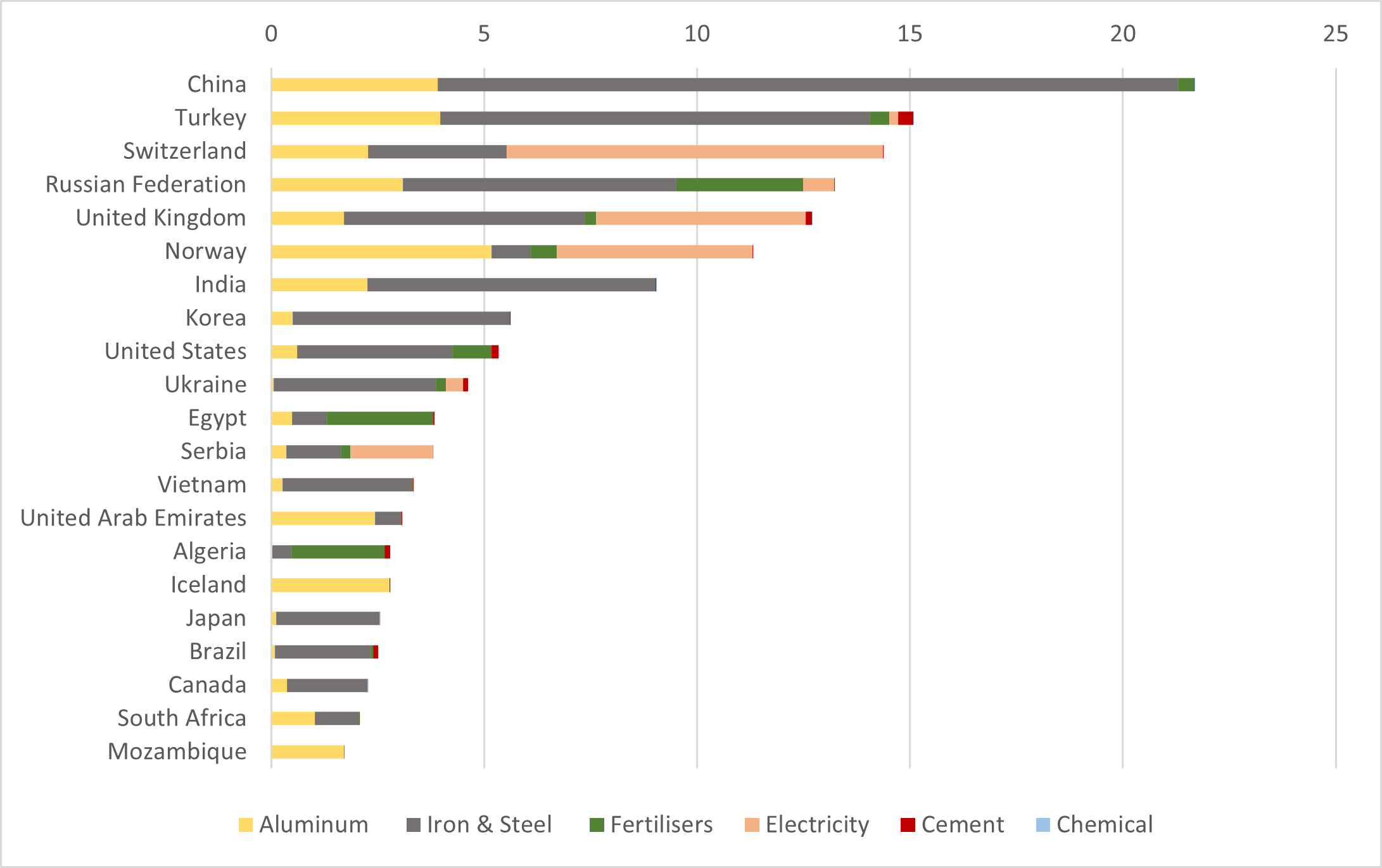

Considering import volumes, India, Brazil, and South Africa stand out as the developing countries most vulnerable to CBAM, while Mozambique emerges as the most vulnerable least developed country.

Figure 1 shows the list of countries with the highest levels of imports to the EU for CBAM-affected sectors in 2022. From this view, China, Turkey, Switzerland, the Russian Federation and the United Kingdom are the top five countries most exposed to the mechanism. However, the effective impact of CBAM will depend on the level of carbon emissions embedded in trade and the carbon prices already paid in the countries of origin, if any. Considering import volumes, India, Brazil, and South Africa stand out as the developing countries most vulnerable to CBAM, while Mozambique emerges as the most vulnerable least developed country (LDC).

Figure 1: Imports of the European Union for CBAM sectors in 2022 (USD Billion)

Source: Authors’ computation using World Integrated Trade Solution, World Bank (2023)

While there is a divergence of opinions in the literature regarding the impact on India’s trade, numerous studies acknowledge that India is among the developing nations most vulnerable to the effects of CBAM. India’s major exports to the EU, such as Iron and steel (28.26%), aluminium (27.18%) and Cement (6.67%) will face significant threats due to carbon levies. Estimates according to Xiaobei et al. (2022), indicate a significant decline in India’s exports of iron and steel by up to 58.5%, alongside potential decreases of around 10 to 12% in exports of non-ferrous metals and chemicals. Whereas Majumder et al. (2023) present contrasting findings, suggesting marginal declines ranging from 0.004% to 0.62% in sectors such as fertilisers, cement, aluminium, iron, and steel. Additionally, the fact that India does not have an explicit domestic carbon tax also raises concerns regarding the potential loss of tax revenue to the EU.

Way Ahead

In essence, the EU’s CBAM is proposed as a forward-looking innovative instrument aimed at reducing carbon leakage and securing a level playing field, but it has the potential to reshape the way countries conduct international trade. It will not only influence international efforts to combat climate change and foster equitable and sustainable economic development but will also change the future pattern of trade. Despite its transformative potential, the development and associated issues discussed above underscore the importance of adopting a balanced and comprehensive worldwide strategy to ensure its efficacy while minimising legal complexities.

Effective implementation of the CCTS will enable Indian enterprises to demonstrate their commitment to low-carbon production processes using green technologies, which can reduce CBAM costs and expand green energy-intensive export opportunities in the EU market.

Meanwhile, the Indian government has already started preparing its own National Credit Market (NCM) through the Carbon Credit Trading Scheme (CCTS). It will serve as an efficient, market-driven incentive for the largest emitters and hard-to-abate industrial sectors to decarbonise. Moreover, effective implementation of the CCTS will enable Indian enterprises to demonstrate their commitment to low-carbon production processes using green technologies, which can reduce CBAM costs and expand green energy-intensive export opportunities in the EU market. In this context, Indian manufacturers must prioritise investments in energy-efficient technologies to minimise carbon emissions and adopt sustainable trade practices.

The author extends gratitude to Janak Raj, Senior Fellow, and Rajat Verma, Associate Fellow, CSEP, for their valuable comments and inputs.

References

European Commission. (2023a). Taxation and Customs Union. Retrieved from CBAM: https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en#:~:text=The%20EU’s%20Carbon%20Border%20Adjustment,production%20in%20non%2DEU%20countries

European Commission. (2023b). Regulation (EU) 2023/956: Establishing a Carbon Border Adjustment Mechanism. Retrieved from https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32023R0956

European Parliament. (2020). Economic assessment of Carbon Leakage and Carbon Border Adjustment. Retrieved from https://www.europarl.europa.eu/RegData/etudes/BRIE/2020/603501/EXPO_BRI(2020)603501_EN.pdf

GATT. (1986). The text of the General Agreement on Tariffs and Trade. Geneva: World Trade Organization. Retrieved from General Agreement on Tariffs and Trade: https://www.wto.org/english/docs_e/legal_e/gatt47_e.pdf

Majumder, P., Mathur, S., & Pohit, S. (2023, August). Smoky Affair. EU’s CBAM is unfair in principle. Retrieved from The Hindu Businessline: https://www.thehindubusinessline.com/opinion/eus-cbam-is-unfair-in-principle/article67154996.ece

Perdana, S., & Vielle , M. (2022). Making the EU Carbon Border Adjustment Mechanism acceptable and climate friendly for least developed countries. Energy Policy 170.

XIAOBEI, H., FAN, Z., & JUN, M. (2022). The Global Impact of a Carbon Border Adjustment Mechanism. The Task Force on Climate, Development and the IMF.

Zimmer, M., & Holzhausen, A. (2020). EU Carbon Border Adjustments & developing country exports: Saving the worst for the last. ALLIANZ RESEARCH. Retrieved from https://www.allianz.com/content/dam/onemarketing/azcom/Allianz_com/economic-research/publications/specials/en/2020/november/2020_11_17_EU_CBAM_and_develping_country_exports.pdf

Bibliography

UNCTAD. (2021). A European Union Carbon Border Adjustment Mechanism: Implications for developing countries. United Nations Conference on Trade and Development.

FOOTNOTES

[1] Carbon leakage refers to the reallocation of industrial production from a region with higher constraints on greenhouse gas emissions to regions with lower constraints, undermining the efficacy of the climate policies in the stricter region.

[2] Most Favoured Nation treatment states that any advantage given to the imported goods of one WTO member must be extended promptly and without conditions to equivalent products originating from all other WTO members, thereby preventing discrimination between countries.

[3] National Treatment states that internal regulations must not favour domestic "like" goods or production over imported products by providing preferential treatment or protection.

[4] The CBDR principle acknowledges individual countries' different capabilities and responsibilities in addressing climate issues.

Find on this page

The Centre for Social and Economic Progress (CSEP) is an independent, public policy think tank with a mandate to conduct research and analysis on critical issues facing India and the world and help shape policies that advance sustainable growth and development.